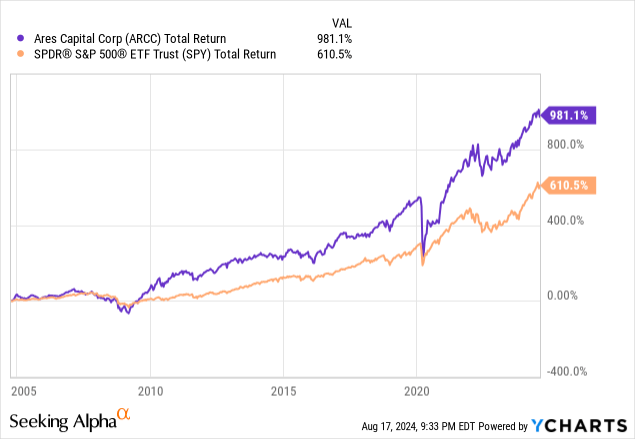

In a turbulent landscape, where interest rates have risen sharply, and recession indicators have started to flash red, Ares Capital (NASDAQ:ARCC) has continued to weather the storm and slightly outperformed the S&P 500 (SPY) over the last 3 years.

However, we do see a lot of headwinds toward Ares Capital as interest rate uncertainty kicks in with the Federal Reserve signaling to cut interest rates in the short term. This is happening against the backdrop of the end of the 40-year bull market in bonds, characterized by steadily declining interest rates that began in the 1980s and ended in 2022, which could signal a transition to higher long-term interest rates. Additionally, we evaluate why Ares Capital may be more sensitive to recession risks than most people think, and why investors should be extremely cautious as the latest macroeconomic data has broadly deteriorated. We also assess the strength of Ares Capital’s dividend and some startling correlations we have found in comparison to “CCC” credit.

Sailing Along

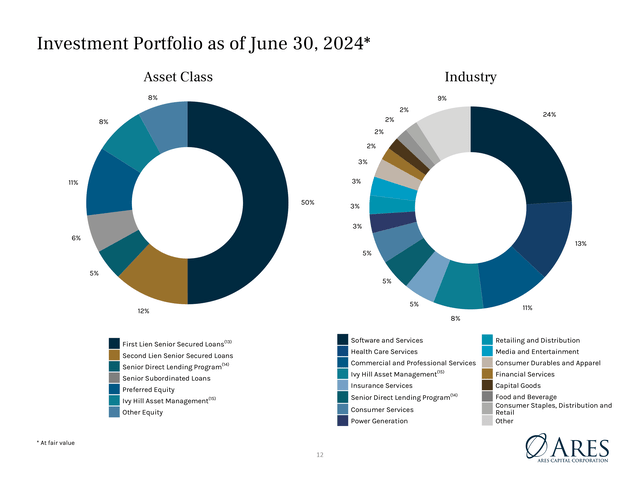

To quickly summarize what Ares Capital business model consists of, it is a Business Development Company (BDC) that invests in small to medium size enterprises, mainly by extending business loans. They do so by raising money from a blend of equity issuance, credit facilities and debt securities. As of last quarter, the fair value of ARCC’s investments stood at $24.97BN, with the liability side consisting of $11.72BN of paid in capital and $13.03BN of principal debt outstanding (mostly long-term debt).

In terms of what those investments consist of, it’s mostly first lien and second lien senior secured notes, which is great since they’re highest up in the capital stack and are supposed to be backed by collateral. The other portion exists of direct lending, subordinated loans, equity etc. They are also very much diversified in terms of the sectors they have lent to. On these $24.97BN worth of investments, they gained $755M in investment income as of last quarter, or $3.02BN at an annualized rate which equates to a yield of approx. 12.09%.

Ares Capital IR

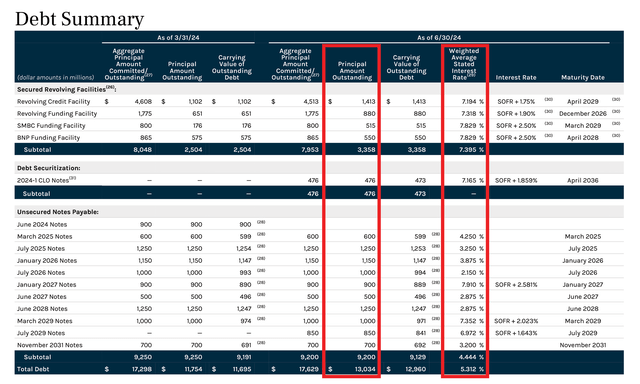

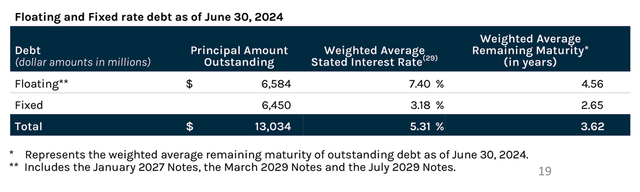

For more clarification on the debt financing side of the balance sheet, out of the $13.03BN of debt, there’s a mix between fixed and floating rate funding. All the $3.36BN worth of credit facilities are floating rate, ranging from Secured Overnight Financing Rate Data (SOFR) +1.75% to SOFR +2.50%, which comes down to an average of 7.39%. The other $9.68BN, which exists out of Unsecured Notes and a CLO, are mostly fixed rate at an average of 4.44%, which is quite low considering it’s not far off the 10-Year United States Treasury yield and most recent debt raised at a floating rate is rather around 7%. The BDC even has some outstanding debt which was raised during Zero Interest-Rate Policy (ZIRP) & Quantitative Easing (QE) at a staggering rate of 2.15%, which we are highly unlikely to ever see again, and is set to reset higher like most of other maturities on ARCC’s book.

We do note that more recent debt issuance has been floating rate debt, at a much higher rate than the fixed debt, raising the weighted average interest rate from 4.88% last quarter to 5.31% right now. This could be due to the high interest which would need to be paid on newly unsecured notes, and perhaps a general belief that the Federal Reserve is likely to cut interest rates soon. On the other hand, Ares Capital is a BDC which isn’t particularly highly levered, only having $13.03BN worth of debt on $24.97BN of investments, with the other half of the financing being made up of paid-in capital. In terms of maturities of the debt, both bank credit and unsecured notes maturities range from 2025 all the way to 2031. In addition, there’s $4,60BN untapped liquidity in revolving credit facilities and $601M in cash and short-term investments.

Ares Capital IR

Dividend Safety

Given most investors own ARCC for the substantial dividend as income, we want to assess how safe this dividend is and whether it’s backed by both safe and sufficient levels of cash flow. In short, to explain on which spread ARCC makes money, they’re gaining 12.09% yield on $24.97BN worth of investments, or $3.02BN in investment income annually based on Q4 figures.

On this $3.02BN, however, $692.11M worth of interest expenses and approx. $728M worth of fees like management fees etc. need to be paid, leaving the common stockholder with $1.60BN before taxes. This means that after income and exercise tax, the company has approx. $1.43BN left to issue as dividends to ARCC, which stands at a $13.07BN market cap. This equates to a hypothetical yield of 10.96%, meaning the 9.26% dividend yield right now is well covered. But what would happen if the interest rate reset higher on all current outstanding debt from 5.31% closer to the 7.40% at which more recent floating rate debt has been issued?

Ares Capital IR

At a 7.40% interest rate on $13.034BN worth of debt, it would require $964.52M to service the debt. Layering on top of that the previously mentioned management fees etc. of $728M, we would be left with $1327.48 of the $3.02BN worth of investment yield generated. Subtracting estimated taxes of $136.41M, we’re left with $1.19BN. That is, however, at a $13.07BN market cap still a 9.10% yield, not far off the current yield being paid out.

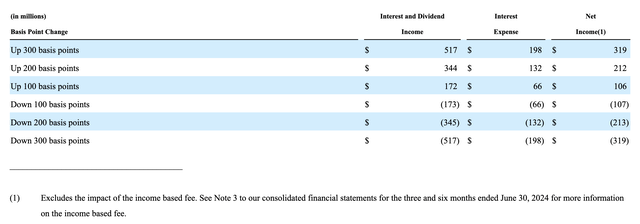

In reality, the income ARCC receives is actually mostly from floating rates and income would be higher as well if rates went up. The previous calculations would only be true if Ares Capital wouldn’t be able to push through costs to borrowers. In the table below are the estimates from Ares Capital on what the annualized impact would be on net income based on interest rate changes. As you can see, higher rates typically favor Ares Capital, but that’s only on the condition that the higher rates don’t deteriorate the business’ fundamentals and with it its ability to pay down debt obligations.

Form 10-Q, SEC

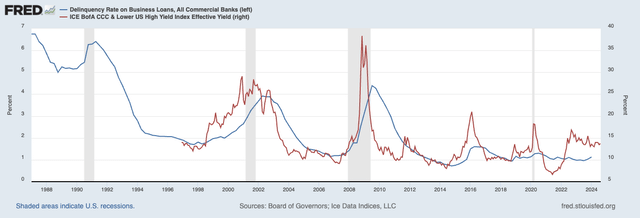

Interest spreads widening sharply would likely lead to a substantial increase in loans having to be put on non-accrual status. Looking at CCC credit, for example, which is currently yielding on average 13.54%, spiked massively during previous recessions. In 2008, for example, yields went to well over 30% for a brief time, in 2001, they rose to 28% at one point and in March 2020, they widened to 18%.

An Uncertain Interest Rate Environment

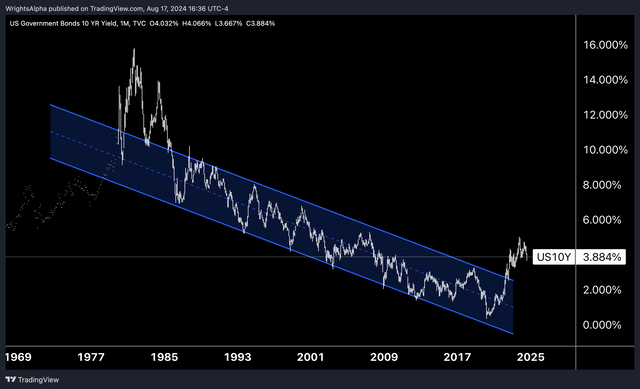

Sometime in early 2022, a major shift took place in the bond market after, for the first time in nearly 40 years, the yield on 10-year government bonds finally broke out of the range within which it had moved during a regime of ever-declining interest rates. We believe that after the “everything bubble” began to burst, this marked the end of the era of “easy money” and that interest rates may be in a long-term trend of higher interest rates.

TradingView, Wright’s Research

In addition to ARCC only having lived through a period of long-term declining interest rates, it has also not faced a meaningful recession over the last 15 years besides a global panic in March 2020 which got solved by pumping trillions of dollars of liquidity into the economy. Either way, when we look at the funding side of Ares Capital, their Unsecured Notes recently got graded “BBB” by Fitch Ratings. In general, “BBB” yields have not seen any meaningful blowout since 2008 and have remained at a very attractive level, making it quite a perfect environment for ARCC to have raised capital.

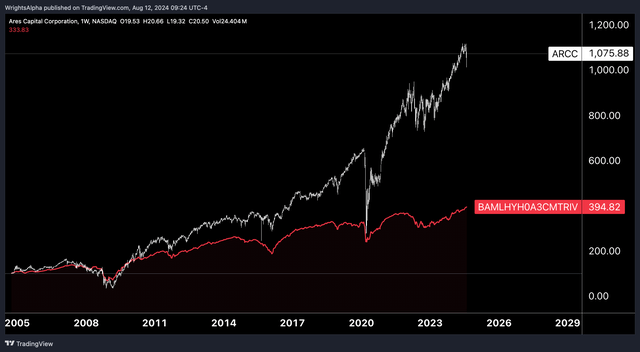

On the lending side of the business, we actually found a staggering correlation between “CCC” credit and ARCC. At this moment, “CCC” credit yields on average 13.54% compared to the previously calculated 12.09% yield ARCC achieves. If we actually overlap the “CCC” bond return index in red and Ares Capital in white, they behave very similarly, experiencing drawdown in exactly the same periods. The key difference being however that Ares Capital has outperformed the index widely over the last 20 years.

TradingView, Wright’s Research

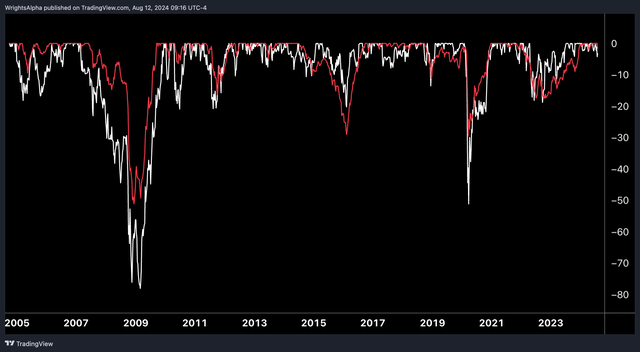

If we put the drawdown of both Ares Capital in white and the “CCC” bond return index, we can also see that they experience eerily similar downturns, with Ares Capital in general seeing a deeper drawdown in serious credit moments like 2008 and 2020. Which is why we would be extremely careful and on our toes about a possible recession or credit event lying around the corner.

TradingView, Wright’s Research

While it is true that in general, higher rates are set to benefit ARCC, in reality this is only the case if it doesn’t lead to more non-accruals. As previously mentioned, borrowers may surely be able to pay 12% or even a bit higher, but surely as we saw in 2008 they’re not able to pay in excess of 30%. Down below, we charted both “CCC” yields and business delinquency rates. And as you can see, they got a pretty staggering overlap as well, with delinquencies rising as credit spreads blow out during a recession. The most worrying part about this may be the fact that over the last 15 years, yields have been pretty much contained in a long period of low unemployment and virtually no business defaults during ZIRP.

Federal Reserve (FRED)

More specifically, recent figures have shown that unemployment is up and the Sahm Rule has been triggered, signaling a very likely upcoming recession. Which is why we would be looking very closely at the spread between the 3-month treasury yield and 10 year treasury yield, since a steepening/de-inversion of this curve, has virtually always signaled a recession.

On the other hand, it does seem like the management is anticipating these tough times ahead, currently having secured far more first-lien loans, switching to risk-off and having at least $5.20BN of liquidity left in revolving credit facilities and cash/short-term investments. The Debt/ Equity ratio of Ares Capital is also standing around 4-year lows, again highlighting the management’s decision to prioritize safety. The management put this quite clear in their Q1 Earnings Call:

And even with that strong company performance, you have capital structures that got set up that may be can’t live through 5% base rates for a long period of time. And that’s why you’re seeing more equity and more structured equity come in to deleverage a lot of these situations with potential for rates to remain higher for longer, which frankly, is kind of our baseline expectation around here. So, we’re managing the portfolio and thinking about risk as if we have higher base rates for longer. (Q1 Earnings Call)

A Note On Portfolio Strength

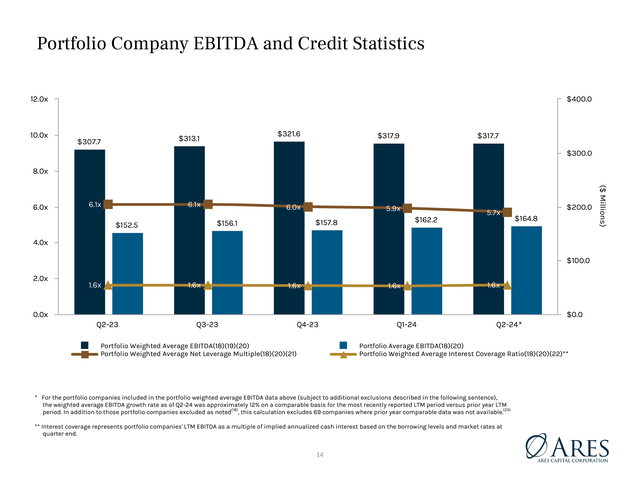

Lastly, we want to touch upon something that we haven’t really seen addressed yet, which are the underlying fundamentals of the portfolio companies as purported by the management team. On the surface, the portfolio companies don’t seem extremely risky, with the LTV ratio of newly originated loans being below 40% in Q2, the net leverage multiple being 5.7x and the interest coverage ratio being 1.6x.

Ares Capital IR

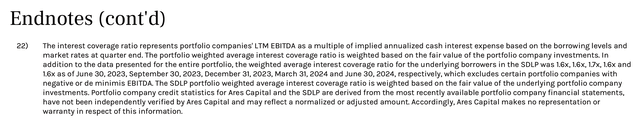

There are big caveats to be added to these metrics. The Net Leverage Multiple for example is broadly defined as: “Ares Capital’s last dollar of invested debt capital (net of cash) as a multiple of EBITDA”. And while this may represent a good measure to some, we believe it doesn’t tell the whole picture of actual profitability since it leaves out Depreciation and Amortization, for example. In ARCC’s calculation, they also excluded certain companies with negative or “de-minimis EBITDA”. In general, we believe there to be a lot of room for subjectivity in this metric.

In addition, their interest coverage ratio is broadly defined as: “LTM EBITDA as a multiple of implied annualized cash interest”. This is quite different from the standard definition of an interest coverage ratio, which we usually see defined using EBIT. So perhaps the current 1.6x interest coverage ratio could be seen as quite a rosy metric as well. In general, to give a clear picture, we would need to see a metric using free cash flow as an interest coverage ratio, or at least a ratio using EBIT to gauge the actual riskiness of their portfolio.

Ares Capital IR

The Bottom Line

In general, Ares Capital is a great BDC with an excellent management team and has a track record of superb execution. But as things stand right now, we’re very precarious and wary about the economic situation, given there are very serious risks that are to the downside in case of a recession or credit event.

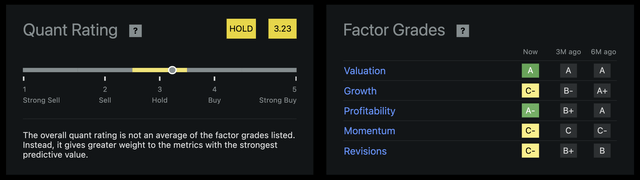

On top of which, it remains to be seen to which extent the BDC industry will be able to adjust itself to the end of the 40-year bond bull market and a potential long-term environment of “higher for longer” interest rates. In conclusion, we believe Seeking Alpha’s Quant to be right, currently assigning a “Hold” to Ares Capital.

Seeking Alpha

Read the full article here