Armada Hoffler Properties, Inc. (NYSE:AHH), incorporated in 2012 and headquartered in Virginia Beach, VA, is a REIT that owns, acquires, develops, and leases a diversified portfolio of office, retail, and multifamily properties in the U.S.

Although the performance hasn’t been spectacular, the market outlook is positive and the company is well-positioned to take advantage of any macro improvement. The REIT is also conservative in its use of leverage and poses strong liquidity, which also provides a margin of safety for investors. But more importantly, the shares are cheap here and the market should correct the valuation once general market conditions improve.

Portfolio

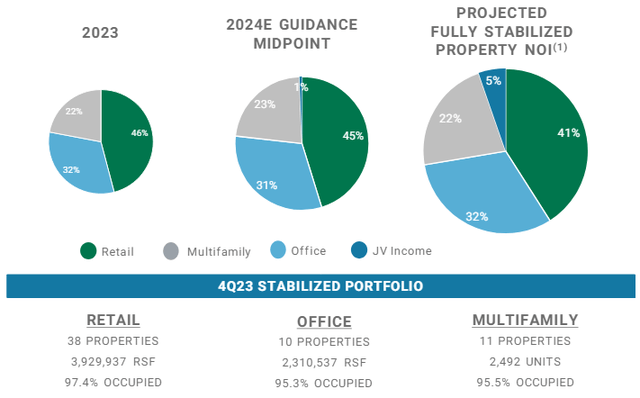

The REIT’s portfolio consists of 59 properties that aggregate 6.2 million square feet and are spread across Virginia, Indiana, Florida, South Carolina, North Carolina, Georgia, and Maryland. Almost half of the NOI comes from retail properties, while the rest is split between office and multifamily:

Investor Presentation

This already diversified source of income, though, is projected to also include income coming from JV investments.

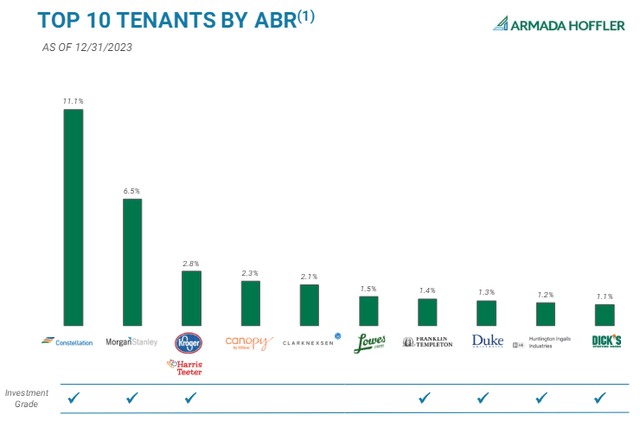

My only objection is in regard to the tenant base, with the two top tenants by ABR being disproportionally responsible for rent generation at 11.1% and 6.5%. To be fair, however, both of those tenants are investment-grade companies:

Investor Presentation

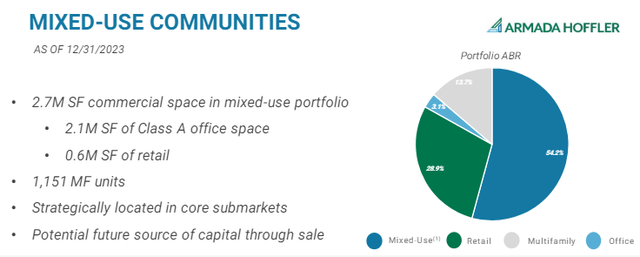

What really differentiates this REIT from others, though, is that it has focused on creating a portfolio of primarily mixed-use communities that allows for a synergy between the 3 property types:

Investor Presentation

Even if that weren’t the case, the outlook for retail and office real estate, which comprise most of Armada’s portfolio, is overly positive. Based on JLL, demand has been outpacing supply for the retail market in the first quarter of 2024 and limited starts coupled with moderate deliveries could continue to constrain supply in the short term. Based on another report, though the U.S. office market had mixed results in the first quarter as negative net absorption remains high, occupier demand is improving. That being said, a slight oversupply is expected for apartments this year, which will decelerate rent growth and increase vacancy.

Performance

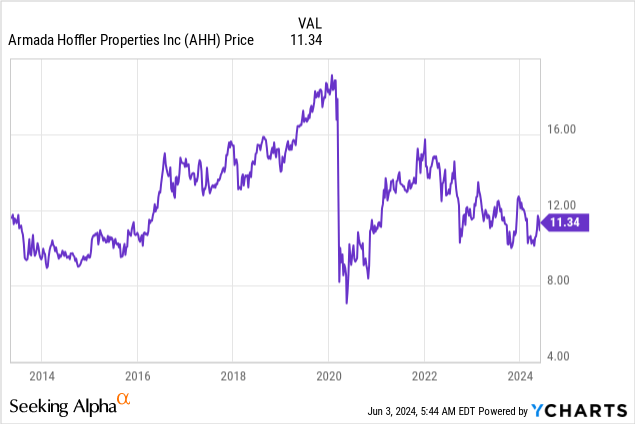

The price of AHH enjoyed modest growth in the last decade up until 2020, surged during QE up until 2022, and fell back to 2021 levels after QT began:

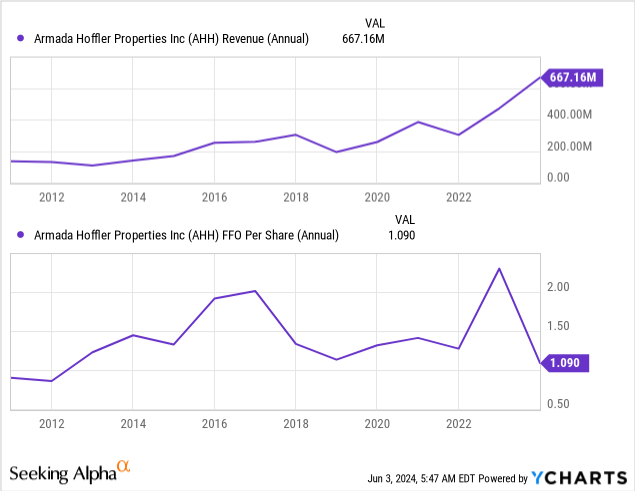

In the last 10 years, Armada’s revenue saw a lot of growth, but the FFO per share had its ups and downs:

More recent results reflect a modest growth in rental income and a decrease in AFFO, but same-store cash NOI has experienced more growth. Below, I compare the annualized figures from the last 10-Q with the average ones from the last 3 fiscal years:

| Rental Revenue Growth | 10.83% |

| Same-Store Cash NOI Growth | 35.23% |

| AFFO Growth | -13.52% |

By not capturing the past 3 years, however, growth has slowed, with same-store NOI only increasing by 0.43% YoY; rental revenue increased by 10% and AFFO decreased by 6.8%.

Now, portfolio occupancy was at 94.7% as of March 31, down from 97% in the same period a year ago. Occupancy for the retail segment was 95.4%, down from 98% a year ago. While office occupancy decreased from 97% in the first quarter of 2023 to 93.6% in 1Q24, it is still a lot higher than the ~80% occupancy rate you observe these days with office REITs and the average for office real estate. Predictably, multifamily proved the most resilient segment, as occupancy decreased YoY from 96% to 95.1%.

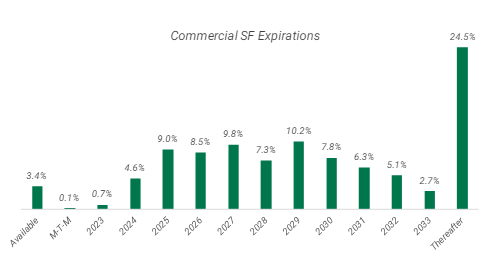

In any case, I don’t think occupancy will decrease much more because the market outlook is improving and Armada’s commercial lease expirations are structured well:

Investor Presentation

Moreover, management has recently shown confidence in its ability to sign new leases at market rates, as it rejected the terms that WeWork proposed. As the COO explained in the 4Q23 earnings call:

We are not willing to impair our trophy asset with a long-term punitive lease and therefore, we’re not willing to accept the terms WeWork needed to stay in the building. As a result, we canceled the lease and simultaneously reduced our forward exposure to the tenant, while maintaining earnings consistent with our guidance target in 2023.

On April 2, the REIT also announced that it renegotiated its lease with WeWork at market rates and the COO commented:

As previously communicated, we have diligently worked to refine lease terms, and we are pleased to have reached an agreement that ultimately results in market-rate rent.

Leverage & Liquidity

Based on the latest report, 61.48% of the REIT’s assets are funded by debt, a structure I find conservative. Debt to EBITDA is decent at 7x and the interest coverage at 2.43x highlights a strong liquidity level, which is not surprising given the debt’s low weighted average interest rate of 4%.

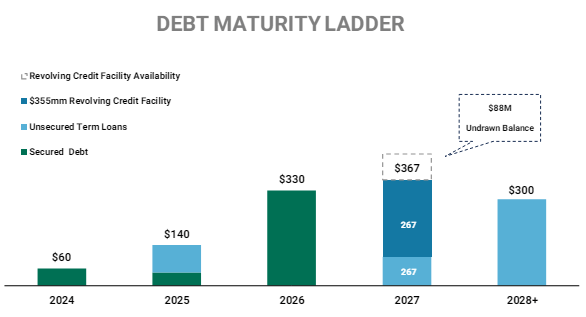

Also, because its debt amounts to about $1.6 billion and Armada’s portfolio is BBB-rated, the upcoming maturities shouldn’t be difficult to deal with:

Investor Presentation

Dividend & Valuation

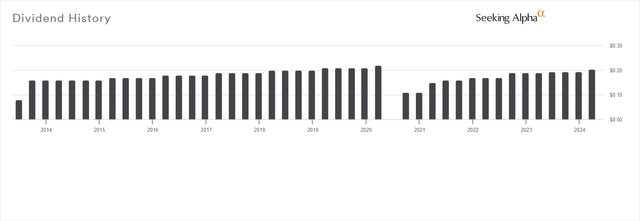

AHH currently pays a quarterly dividend of $0.205 per share, resulting in a forward yield of 7.19%. With a 61.88% payout ratio, the dividend is well covered and though Armada had to suspend it back in 2020, the distribution has returned to pre-pandemic levels:

Seeking Alpha

The yield is also quite attractive right now and along with the 9.11 FFO multiple, it represents good value. Consider that AHH with the rest of the diversified REITs that invest in the same property types as Armada averages 10.39x; AHH also has the lowest multiple:

| Stock | P/FFO |

| (AHH) | 9.11 |

| JBGS | 12.84 |

| AAT | 9.51 |

| ESRT | 10.1 |

| Average | 10.39 |

Moreover, the implied cap rate AHH is trading at is 6.51%; while the weighted average cap rate at which its portfolio could be sold today is probably around 6.9% based on 2024 forecasts, this would be a very conservative rate to use for NAV as it seems that 2024 cap rates may prove to be the highest they have been in a very long time and Armada’s properties enjoy a synergistic quality that places them above the average.

But even using this cap rate for the calculation, the shares seem to be trading at a 13.86% premium to NAV ($9.96). In reality, they could be trading at a large discount, but it’s hard to determine what cap rate is appropriate for such a portfolio.

Risks

While I don’t find such a small premium based on pessimistic assumptions representative of a risk, I am concerned about interest rates remaining high for longer than anticipated by the market because inflation doesn’t seem to be reaching the Fed’s target soon. In any case, this dividend yield is high enough to pay shareholders to wait more comfortably.

Another risk you should be aware of is that of Armada losing two of its largest tenants by ABR; since it is reliant on them for nearly one-fifth of its rental revenue, that could have a serious impact on its bottom line, at least in the short term.

Last, even though I have based my NAV calculation on a very conservative assumption, if cap rates expand more, NAV may prove to be optimistic for as long as they are elevated. Calculating NAV is not an exact science, and the market may negatively react to rising cap rates by adjusting down the price of AHH.

Verdict

Since I find the price of AHH very attractive at such an FFO multiple and implied cap rate, I am rating it a buy. Also, I believe that the portfolio is well-diversified, profitability is about to improve, and the shares are too cheap to ignore right now.

What do you think? Do you own this REIT or intend to? Let me know and I’ll get back to you soon. Also, please leave a comment if you found this post useful; it means a lot! Thank you for reading.

Read the full article here