Investment Thesis

ARMOUR Residential REIT, Inc. (NYSE:ARR) has been on a downward trajectory, losing over 33% of its share value over the last year and underperforming the market by a margin of about 55%.

Seeking Alpha

I anticipate a sharp decline in the company’s shares due to the company’s 40% reduction in dividends. To add to its woes, the company appears to have little to nothing attractive to offer investors, as evidenced by poor EPS, high debt-to-equity ratio, and low dividend coverage ratio. To further compound my bleak outlook for this stock, revisions are trending lower, indicating deteriorating fundamentals and leading me to a bearish stance. I recommend selling this stock before it declines further due to the deteriorating fundamentals, especially the downward revisions to revenues and earnings and the significant dividend cuts.

Weakening Fundamentals: Catalyzing The Downward Trajectory

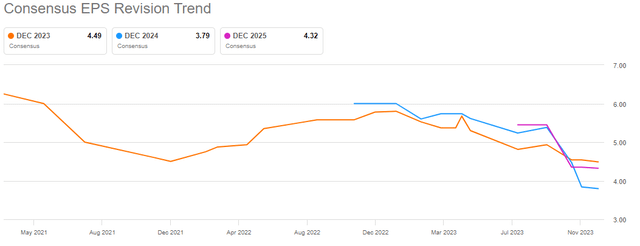

According to my experience, when a company’s earnings estimates rise, so does its stock’s fair value. A higher fair value than the current market price increases investor interest in purchasing the stock, causing its price to rise and vice versa. Given this context, ARR has earnings and revenue revisions that are trending downward, indicating a downward share price trajectory, in my opinion. To begin with, ARR has 2023 and 2024 consensus estimates of 4.49 and 3.79, representing a YoY growth of -22.63% and -15.44% respectively. In my view, this marks the weakening fundamentals of the stock, which is set to persist until 2024.

Seeking Alpha

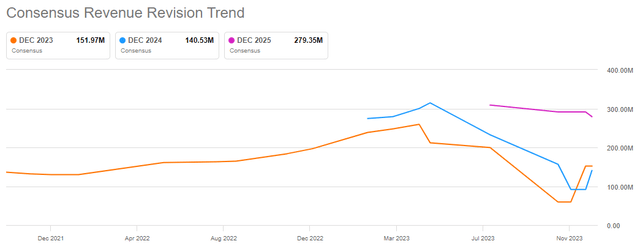

Regarding revenue, the consensus estimates are $151.97million in 2023 and $140.53 million in 2024, representing a YoY growth of -7.53% between 2023 and 2024.

Seeking Alpha

Even though a company’s ability to grow its earnings is probably the best measure of its financial health, if it is unable to increase revenues, not much will happen. A company can hardly hope to increase its earnings over the long run without increasing its revenue, which explains why these two parameters interest me.

To shed light on the company’s current situation concerning these two crucial metrics, $3.6 million in revenues were reported in the MRQ, representing an 85.7% year-over-year change. The same period’s EPS of $1.08 is in comparison to $1.60 from a year ago. Only once in the previous four quarters did the company beat EPS projections. Over the past four quarters, the company has failed to surpass consensus revenue estimates. These trends, in my opinion, indicate deteriorating fundamentals, and I anticipate that these trends will worsen when the company’s interest swaps, which have been providing a sizable income stream for the company, expire. With this background, I believe the weakening fundamentals shall catalyze a downward trajectory now and in 2024, as the above projections show.

Investors In Losses

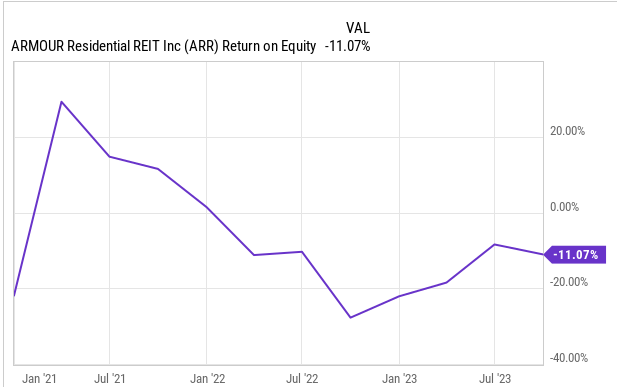

While the goal of any investment is to get considerable returns on investment, ARR appears not to offer an avenue to actualize that goal. This is evidenced by several poor attributes exhibited by the company. To begin with, ARR has a very low return on equity [ROE]. It has a ROE of -11.07%, which means it does not generate any profit for its shareholders relative to their equity investment. This indicates that it is not creating value for its shareholders or rewarding them adequately for their capital contribution.

YCharts

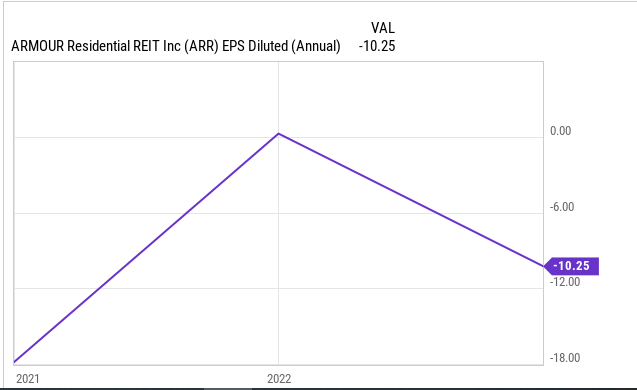

Additionally, the company has a negative and declining annualized EPS of -10.25, which means investors are losing money for each share they own. I believe this loss could be majorly due to the impairment charges it incurred from the decline in the value of its RMBS portfolio due to rising interest rates and prepayment risk. This challenge is set to persist, given that interest rates are projected to stay elevated for a long time.

YCharts

In addition, the company has a total debt of $11.5 billion. With total assets of $13.9 billion and total liabilities of $12.6 billion, ARR has equity of $1.3 billion. This translates to a very high debt-to-equity ratio of 8.8, which means it relies heavily on borrowed funds to finance its operations and growth. This increases its interest expenses and financial leverage and exposes it to the risk of default or bankruptcy if it cannot meet its debt obligations. For instance, its TTM interest expenses amount to $123.2 million, and with negative profitability, its earnings cannot cover these interest expenses. This implies that the company faces a big risk of defaulting on its debt servicing. Further, with a cash flow from operation of $179.89, it means that its operating cash flows can cover its outstanding debt by about 1.56%, which is a very precarious state in my view. Although I appreciate the company’s high liquidity level, I believe it cannot sustain the company for long because I expect a very high cash burn rate, especially when its interest rate swaps expire.

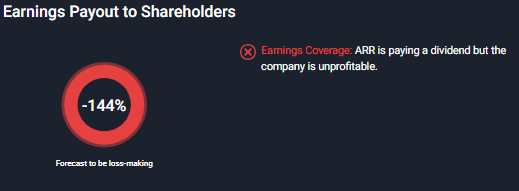

Lastly, it has poor dividend coverage given that they are distributing more than 100% of its earnings, which means it pays out more dividends than it generates from its earnings. This reduces its financial flexibility and ability to invest in new opportunities or maintain its dividend payments in the future.

Wallstreet

Based on this information, I believe selling ARR is long overdue because investors are in losses, which I expect to magnify as the company’s fundamentals weaken.

Technical Analysis

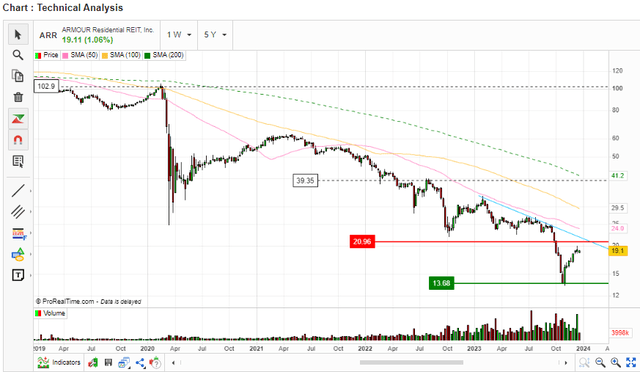

Based on several indicators, this section will cover the technical analysis of ARR. To begin with, this is the trend. ARR is currently in a downtrend, making lower highs and lower lows since Feb 2020. The stock has broken below its 50-day, 100-day, and 200-day moving averages, which are all sloping downward and acting as resistance levels. The stock also trades below a downward trend line that connects the highs of August, September, and October. The stock may face further downside pressure if it breaks below the support level of $13.68, which is the current lowest low.

Author Analysis On Market Screener

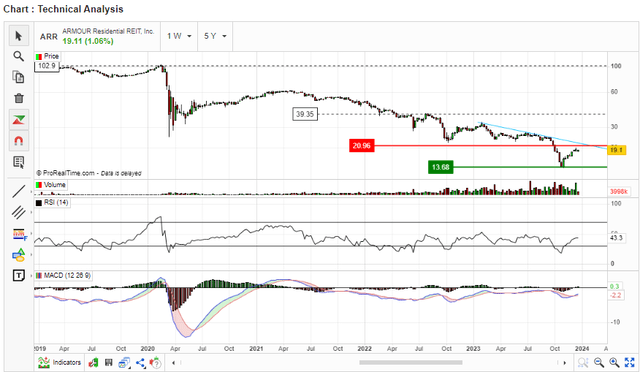

Moving to momentum, ARR is currently showing a strong momentum as it has been trading in a wide 52-week range between $13.32 and $33.38. The stock’s Relative Strength Index [RSI] is 43.3, which is neither overbought nor oversold. However, the RSI also shows a bearish convergence with the price, as it has made a higher low, while the price has made a lower one. This suggests the bearish trend is still on. The stock’s Moving Average Convergence Divergence [MACD] is at -2.2, a sign of a bearish trajectory. The MACD also shows a crossover with its signal line, indicating an increase in momentum.

Author Analysis On Market Screener

Based on the technical analysis, ARR is currently in a downtrend with strong momentum. The stock may face more downside risk if it breaks below the support level of $13.68.

My Final Thoughts

In summary, given ARR’s deteriorating fundamentals and the losses it is causing investors, I think the time is right for those who still own it to sell. Technical analysis indicates that the stock is in a bearish trend with a strong momentum. Given the weakening fundamentals and the recent dividend cuts, I believe a significant downward trajectory is on the horizon due to the selling pressure from investors.

Read the full article here