This Analysis Recommend a “Hold” Rating For Artemis Gold Inc.

This analysis confirms the recommendation given in the previous analysis for the shares of Artemis Gold Inc. (OTCPK:ARGTF) (TSXV:ARTG:CA) and therefore reiterates the rating “Hold”.

The previous “Hold” rating supported the view that, despite its technically high valuation, the stock still offered the opportunity to benefit from further increases in the price of safe-haven gold ahead of a risk of recession in 2024.

The Hold rating involved waiting for a dip in the share price, which emerged on January 22 after a nearly 15% price correction, as then-withered market pricing centered on the Federal Reserve’s rate cut as early as March temporarily weighed on non-yielding gold, and on US-listed stocks. Over that week, as a benchmark for the US stock market, U.S. equity ETFs recorded the bulk of outflows driven by information technology (XLK), which was perceived to be on the downside, moderately offset by consumer discretionary (XLY) and energy (XLE)’s above-average inflows.

Higher interest rates raise the risk of a significant slowdown in consumption and investment activity, pushing the Fed toward its goal of reducing inflation, or the rate at which shopping prices increase. While fears of an economic slowdown drive demand for gold as a safe haven and set the stage for a trend toward robust gold prices, the fears, when they sit in, lead to the assumption that the weaker economic conditions are not reflected in the valuation of U.S.-listed equities. It happens that market sentiment for US-listed stocks temporarily deteriorates, and since securities linked to the safe-haven gold price are not exempt from the rest of the market trading in a bearish mood, Artemis Gold shares may also experience sudden corrections.

Artemis Gold benefited from the impact of the Fed’s “Higher for Longer” interest rate policy on long-term demand for gold as a safe-haven investment strategy. After the dip, the stock price resumed its uptrend, rising 60.19 percent since the last article, while the change in the S&P 500 was 12.48 percent.

About Artemis Gold Inc. and its Goal of Pouring the First Gold in the Second Half of 2024

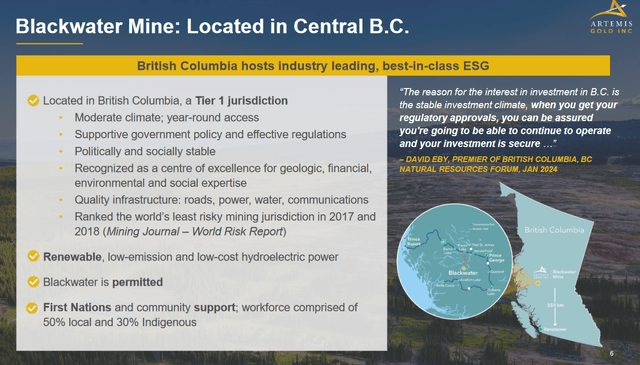

Artemis Gold Inc. is based in Vancouver, Canada, and is engaged in the gold and silver mining and exploration industry as it aims to bring a project called the “Blackwater Project” or simply “Blackwater” into gold production. Artemis Gold Inc. (hereinafter simply “Artemis”) is the sole owner of the Blackwater project, and this project is expected to deliver its first gold in the second half of 2024. The fully permitted Blackwater Project is located 110 km southwest of Vanderhoof, British Columbia, Canada. This is a country with mining-friendly legislation, which, according to the Sprott ESG Mining Risk Heat Map 2024, results in minimal investment risk, and this is as true for Artemis as it is for its investors and shareholders. Key communications infrastructure connects Blackwater to potential markets and upcoming gold production will be okay from an environmental and decarbonization perspective. In Canada, mining permits are granted an average of two years after application, while in the United States and Australia, which are also known for their openness to this type of sector, it can take up to ten years, as indicated by North American and European experts, contributing to the minimal risk of Blackwater compared to other projects of peer companies.

Artemis Gold Inc. Corporate Presentation June 2024

Blackwater Mine: A Gold Equivalent Production Facility Moving Through Fully Funded Phases

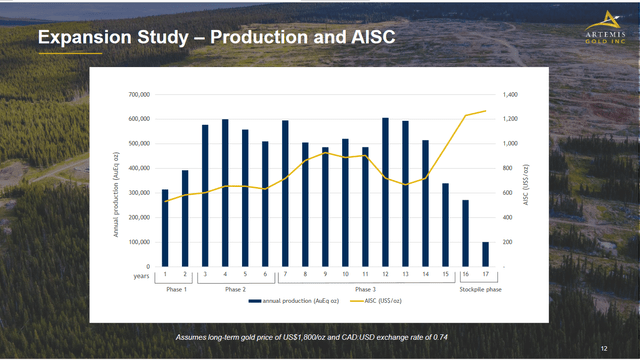

Blackwater is a 22-year mine life gold equivalent deposit that projects a viable expansion to the 500,000 gold equivalent ounces (or “GEO”) that the asset would produce on average in each of the first 10 years of expanded production at an average All-In-Sustaining Cost (or “AISC”) of $712 per ounce.

Artemis Gold Inc. Corporate Presentation June 2024

Blackwater’s total operating life consists of three phases:

- During the first of the two years of Phase 1, the open pit mine will produce just over 300,000 GEOs, and in the second year a little bit under 400,000 GEOs, with the processing plant capable of processing 6 million tonnes per year (or “tpa”).

- After Phase 1, Blackwater will reach the 500,000 GEO target sometime in year 3 of Phase 2 (that is the first year of this phase), once this phase is completed, in the sense that the plant will be able to process a throughput of up to 15 million tonnes per annum (or “tpa”). Thus, the plant is expected to reach approximately 580,000 GEOs by the end of Year 3 of Phase 2, which runs through Year 6.

During phase 2, production will fluctuate between 500,000 and 600,000 GEOs.

- Phase 3 then begins immediately after a further expansion of the processing plant is completed, increasing its capacity to 25 million tpa in year 7. This phase lasts until year 15, with GEO production peaking at (or just below) 600,000 in years 7, 12, and 13.

The Proven and Probable 8.4 million GEO (334.3 million tonnes grading 0.75 g/t gold and 5.8 g/t silver) reserve-based expansion study states that these increased production levels from the 2021 feasibility study highlighted in the previous analysis will be fully funded by internally generated cash.

For this scenario to become a reality, a gold price of at least $1,800/oz is needed. This is quite possible, as gold’s reputation as a safe-haven asset offers solid prospects not only in the face of the current risk of recessionary headwinds but also in the face of long-term geopolitical tensions between countries. Plus, assuming AISCs behave according to the yellow line in the chart – at $712/oz, Blackwater gold production will be significantly cheaper than many in the industry, bolstering expectations not a little.

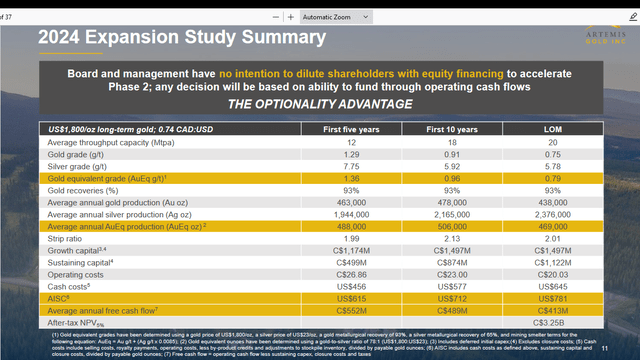

Returning to the financing of the project, for Phase 1 specifically, this is how the start of production comes online: The initial capital guidance of CA$730 million to CA$750 million is allocated to bring Blackwater into production and thus complete Phase 1, which is fully funded. Since the construction of the mine began, the company has spent CA$523 million through Q1-2024, and for the remainder spent at CA$207 million to CA$227 million, there is already CA$295 million of committed funding. The latter is derived from the following sources: It will be financed with CA$154.5 million in cash on hand as of March 30-2024, plus C$100 million in project credit facilities (including capitalized interest) and C$40 million in cost overruns. There is an option to receive an additional CA$25 million from 26.3 million warrants with an exercise price of CA$1.08 expiring in August 2024. At the end of March 2024, the mine was 73% complete.

A Low-Cost Production of Gold Equivalent from Mid-Tier Mine

Blackwater will be a low-cost gold producer compared to the benchmark created by S&P Global Market Intelligence based on an analysis of the world’s 11 largest gold miners. These companies had an average AISC/oz of $1,345 in the fourth quarter of 2023. Neither when it is expected to peak during its 17 years of fluctuations will AISC/oz for Blackwater production be even close to the average cost that the gold mining industry bears today.

Sticking to Blackwater’s projected production and costs, let’s draw a parallel between Artemis’ gold business proposition in British Columbia and some of its future competitors already operating today. With 500,000 to 600,000 ounces from the Blackwater mine, Artemis would be a “mid-tier gold stock,” as analyses of this U.S. stock market sector assign this designation to gold mining companies with annual gold production of 300,000 to 1,000,000 ounces. Leading mid-tier gold-stock benchmark VanEck Junior Gold Miners ETF (GDXJ) the second largest gold exchange-traded fund after (GDX) with $5.08 billion in net assets at the time of writing, identifies, Equinox Gold Corp. (EQX) (EQX:CA), Eldorado Gold Corporation (EGO), OceanaGold Corporation (OTCQX:OCANF) (OGC:CA) as potential competitors for when Blackwater extracts the yellow metal and bears all the associated costs. Equinox, Eldorado Gold, and OceanaGold have very similar production levels, but significantly higher AISC compared to Artemis’ Blackwater. This means that if their earnings/revenues attracted the market enough to drive their shares very energetically high, shares of Artemis are theoretically better positioned to enjoy the yellow metal’s rally due to the Blackwater project. Of course, without underestimating the important role that the strong upward momentum in gold plays for these companies.

Rising Gold Prices Are Crucial, but Potential Artemis Peers Are not Mining Cheaply

It has pulled up more expensive mid-tier competitors and with production not always on an upward trend, who knows what a rising gold price could mean for Blackwater.

Equinox Gold Corp.: EQX operates eight gold mines, including 100% ownership of Greenstone Gold Mine GP Inc. since last month, which poured the first gold on May 23. Equinox Gold had a strong start to the year with 111,725 ounces of gold at an AISC of $1,950 per ounce in the first quarter of 2024. The company is on track to achieve its full-year 2024 production and cost guidance of 660,000 to 750,000 ounces of gold at an AISC of $1,630 to $1,740 per ounce. Equinox reported non-GAAP earnings per share of -$0.04 for the first quarter, beating expectations by $0.03, while revenue rose 3.1% year-over-year to $241.3 million. The increase in revenue was primarily due to a 9% increase in the average realized gold price to $2,066/oz year-over-year, which offset lower gold sales volumes, down 5.5% YoY to 116,504 oz and a 17.6% YoY increase in AISC/oz to $1,950.

Concerns about a significant slowdown in the US economy – likely reflected in Chinese investors’ flock to gold, aided by the reduction in US cash reserves that appeared threatened by adverse conditions – also started to improve Western sentiment toward the yellow metal as a safe haven in the face of headwinds from the US cycle.

The rising positive sentiment for gold as a safe haven among Western investors led the gold spot price (XAUUSD:CUR) to hit an all-time high on May 20, reaching $2,450.13/oz intraday. Gold bulls boosted Equinox shares, with EQX up 5.5% (+10% on May 20) and EQX:CA up 4.6% (+9.3% on May 20) since its Q1 2024 report.

Eldorado Gold Corporation: A positive reversal of free cash flow to $33.7 million (after outflows of $19.2 million in Q1 2023) occurred thanks to an 8% increase in the average realized gold price to $2,086/oz in Q1 2024, offsetting Turkish winter conditions and ore grade volatility that increased AISC/oz (+4.6% y/y to $1,262/oz), on slightly improved gold production (+5% y/y to 117,111 oz).

Skouries open pit/underground gold/copper mine in Palaiochori, Greece is scheduled to begin production in the third quarter of 2025. With momentum building at the Lamaque complex in Quebec, the company is on track to achieve its 2024 annual production guidance of 505,000 to 555,000 ounces of gold at an average AISC of $1,190 to $1,290 per ounce. Eldorado Gold reported first-quarter non-GAAP earnings per share (EPS) of $0.27 on April 25, beating analysts by $0.13, primarily due to higher gold prices. Revenue increased 12.5% year-over-year to $258 million.

Traders bracing for a possible U-turn by the Federal Reserve after earlier hints of a rate cut had not boded well for the short-term changes in gold prices in late April. On the other hand, the outlook for safe demand for the yellow metal was good as intensive central bank purchases pointed to increasing headwinds as high interest rates notoriously dampen consumption and investment. As continued strong safe-haven demand helped gold post its third consecutive monthly gain at the end of April 2024 despite a short-lived dip, EGO’s Q1 2024 results released on April 25 were further embellished, reflected in a stock price rally. The latter gained additional upside momentum with improved Western sentiment for gold around May 20, as described above. EGO shares have risen 10.7% since the company’s first-quarter 2024 report (or up nearly 12% to the May 20 high).

OceanaGold Corporation: A record average realized price of $2,092 per ounce (up 9% year-on-year) offset a 4.3% year-on-year decline in gold sales volumes to 116,800 ounces in the first quarter of 2024 at OceanaGold Corporation. Its production fell 11.3% year-on-year to 104,800, resulting in an AISC of $1,823, or 16.3% higher year-on-year. However, given the robust gold price outlook, the company is increasing free cash flow expectations and forecasting strong production growth in 2024 at all four operating locations in the United States, the Philippines, and New Zealand. OceanaGold wants to deliver 510,000 to 570,000 ounces of gold in the full-year 2024 at AISC of $1,475 to $1,600/oz. sold.

April 30, 2024, OceanaGold Corporation reported first-quarter non-GAAP earnings per share of $0.01 on revenue growth of 10.8% year-over-year to $270.3 million (+10.8% year-over-year), topping expectations of analysts by $19.3. million. Supported by a higher gold price amid strengthening safe-haven demand, as previously illustrated, Q1-2024 results and guidance attracted even more stock market interest around shares of OceanaGold. The company’s payment on 04/26/2024 of a semi-annual dividend of $0.01/share for a trailing 12-month annual payment of $0.02/share also contributed, sending shares of OCANF up 10.2% and OGC:CA up 8.4% since the report.

As improved revenues or profits have strongly boosted US gold mid-tier stocks, the same dynamic should apply to Artemis Gold Inc. (OTCPK:ARGTF) (ARTG:CA). The price of gold, in turn, is expected to remain supportive when Blackwater comes online in the second half of 2024.

The Gold Price Outlook: Strong Upside Potential for Artemis

Since the Fed’s rate hike policy does not stimulate growth, but has the opposite effect, the risk of an economic slowdown increases: the longer interest rates remain high, the longer they can curb consumption and investment as part of the goal of fighting inflation. Investors will seek protection for the value of their portfolio assets in safe-haven assets such as gold, as David Meger of High Ridge Futures signaled as a long-term scenario: “higher uptrend in gold will continue as the Federal Reserve might not be cutting rates as soon as the market expects.” The recession, together with geopolitical tensions, will be an additional driver for healthy demand for gold as a portfolio hedge.

This week provided a new slate of additional signals of an impending recession: The expectations sub-index of the Conference Board’s consumer confidence index of 74.6 points to a possible near-term recession, as below 80 indicates a significant decline in business conditions. Although inflation has fallen dramatically since the Federal Reserve’s aggressive interest rate policy, according to the Fed’s May 2024 Beige Book, U.S. households are still very price-sensitive, and as a result, retail spending is suffering. Attempts to boost demand, such as buy-down strategies to facilitate the purchases of new houses or incentives for buying new vehicles including electric vehicles, are not enough to boost the overall growth outlook, which instead remains weak. In addition from the Fed Beige Book, current macroeconomic conditions continue to do nothing to improve the outlook: persistent inflation and increased borrowing costs are discouraging economic actors from spending/investing, and high interest rates are leading to a stagnation in lending activities to finance growth projects. The US economy is gloomier: The updated estimate of US GDP growth for the first quarter of 2024 assumes that the economy grew more slowly, by 1.3% compared to the previous estimate of 1.6%, and versus 3.4% in the fourth quarter of 2023. All major components of the economy (consumption, investment, and government spending) were estimated to be significantly weaker than in previous readings.

The strong demand for gold as a portfolio hedge against a recession gives the market enough support to predict ever-higher gold prices in the future.

With these premises, Artemis shares should not remain undervalued for long compared to Net Present Value per share (or “NVP”).

Artemis Gold Inc. Corporate Presentation June 2024

The after-tax NPV at a 5% discount for the expanded Blackwater project is C$3.25 billion over its entire life, assuming a very likely gold price of $1,800 per ounce as explained. Dividing CA$ 3.25 billion by the number of shares outstanding (ticker) of 201.87 million, Artemis Gold Inc.’s NPV/share is CA$ $16.10 or US $11.77 at the time of this writing. Currently, shares are trading as follows.

The Stock Price: A Dip Cannot Be Ruled Out

Shares in ARGTF are trading at $7.77 per share, giving it a market cap of $1.62 billion at the time of writing. Shares are well above any of the MA Ribbon lines and near the upper limit of the 52-week range of $3.38 to $8.16/share.

Source: Seeking Alpha

The chart shows the 14-day Relative Strength Indicator at 57. This signals that the shares are not yet overbought, although they are trading well above the MA ribbon and close to the share price’s 52-week range upper limit. But with the Fed expected to keep rates higher for longer Artemis shares, since they are gold-backed securities, could come under downward pressure and pull back significantly from current levels.

Higher interest rates are not beneficial for gold because owning the precious metal, which does not generate income, comes with the higher opportunity cost associated with not owning U.S. Treasury bonds, which instead offer interest income based on fixed rates. Negative impacts from higher rates also affect Artemis stock, as gold prices and Artemis Gold share prices are positively correlated.

According to the CME FedWatch tool, interest rate traders put a 50% probability that the US central bank will cut borrowing costs at the September meeting. But this exposes the metal to a significant period from now when market participants could prefer the US Treasury yield to the yellow metal.

In addition, the yellow metal price is exposed to 2 negative drivers in the short term:

- With the US jobs number coming in much higher than expected in May 2024 (272,000 additions, the most in 5 months), there is a risk that inflation will be even more stubborn than it is now. As a result, the Fed may make even more aggressive statements through its policymakers in the coming weeks, ultimately leading the CME FedWatch tool to reduce expectations for a first-rate cut in September.

- With the holidays underway, people tend to spend more money on vacations, so inflation may rise: Perhaps the Fed is waiting to see what effect the summer vacation will have on inflation.

Artemis offers interesting growth prospects due to the Blackwater momentum and the rosy gold price forecast. However, investors should Hold onto the shares for now as the short-term negative factors of higher interest rates hindering the rise in gold prices will impact the share price of Artemis Gold stock, potentially enabling more attractive valuations.

Additionally, the average volume of ARGTF stock is 27,480 shares traded in the past 3 months. Scroll down this Seeking Alpha page to the “Trading Data” section to view it. For this reason, ARGTF stock is a low-liquidity stock, and investors should not hold too large positions, otherwise they will find it difficult to reduce them accordingly if circumstances require it.

The same considerations apply to shares traded on the TSX Venture Exchange under the symbol ARTG:CA.

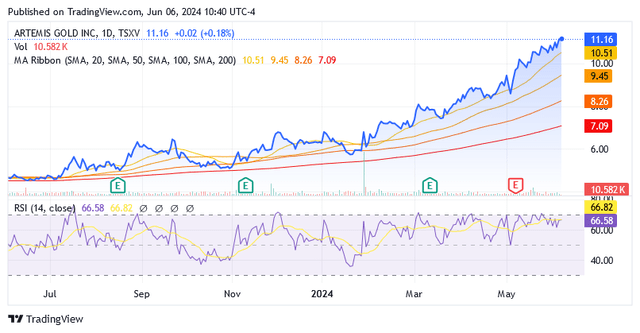

Shares in ARTG:CA are trading at CA$11.16 per share, giving it a market cap of CA$2.22 billion at the time of writing. Shares are well above any of the MA Ribbon lines and near the upper limit of the 52-week range of CA$4.45 to CA$11.19/share.

Source: Seeking Alpha

The 14-day relative strength indicator is at 66.58 on the chart, signaling that shares are not yet overbought despite their strong uptrend since the start of the year.

Additionally, the average volume of ARTG:CA stock is 155,507 shares traded in the past 3 months. Scroll down this Seeking Alpha page to the “Trading Data” section to view it.

Conclusion

The Artemis Gold project of Blackwater aims to install low-cost mid-tier annual production of ounces of gold equivalent in British Columbia. The region is well known to host deposits of precious metal ore and traditionally is mining-friendly. Plus, bureaucratic hurdles to obtaining mining permits do not exist, and the presence of key infrastructure reduces the risk of Blackwater to a very low level. The open pit mine is expected to produce its first gold in the second half of 2024. The construction of the mine is well supported financially, and all necessary funds have been committed. The final step is imminent for the completion of Phase 1, which will coincide with the start of production. The expanded phases 2 and 3 will then be financially supported by internally generated funding sources.

Blackwater is very profitable on a gold price assumption that is likely to be reflected by future markets, as today there are signs of strong use as a portfolio hedge: this demand for gold will be driven by the risk of recession and, in the longer term, from an uncertain scenario due to geopolitical tensions.

The exploitation of gold deposits is also becoming more and more expensive for most miners who are going to be burdened with significantly higher production costs than Artemis’s Blackwater.

Given Blackwater’s solid prospects, investors may want to Hold the stock for now, as near-term headwinds for gold could impact Artemis stock and more attractive price levels cannot be ruled out.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here