Overview

There are so many different avenues that you can invest in and collect a distribution from. This is why I believe that this is one of the best times in modern history to be an income investor. abrdn Global Infrastructure Income Fund (NYSE:ASGI) is one of these relatively new funds, with the inception dating back to 2020. ASGI operates as a closed end fund that aims to provide a high total return while maintaining exposure to assets that are considered essential services to society. ASGI has assets under management totaling slightly over $500M and is actively managed by abrdn’s Global Equity and Real Assets team. ASGI has a net expense ratio of 1.65%.

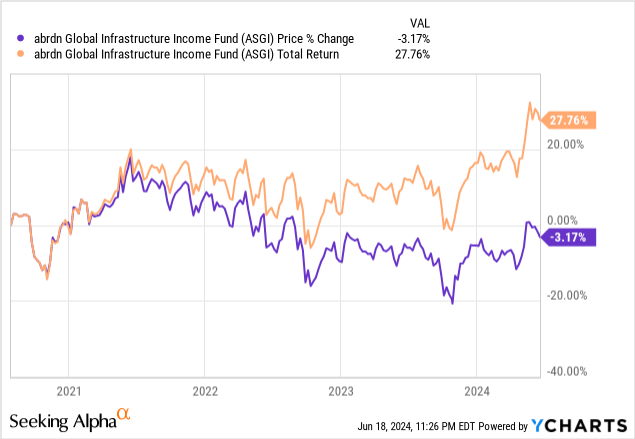

We can see that the price stayed mostly flat since inception, being down only 3%. However, due to the high distribution yield of about 12.5%, we can see that the total return sits at 27%. Something that makes this fund attractive for income focused investors is the high yield that issues its distributions out on a monthly basis. Additionally, the latest annual reports reveal that the distribution is well supported from the net investment income as well as realized gains from the underlying equities within.

Since the fund is still relatively new, it hasn’t had enough time to establish enough of a reputation in more typical macro environments. When the fund launched, interest rates were at near zero levels. Only two short years later, interest rates were hiked to decade highs. This is why I believe that once the macro environment starts to improve, I believe that there is a nice upside potential for ASGI, since most of the sector exposure within the fund is set to benefit from lower interest rates. Additionally, the fund currently trades at a decent discount to NAV. However, I would like to first start by discussing the portfolio of holdings and the strategy ASGI follows.

Strategy & Holding Breakdown

Since ASGI operates as a closed end fund, we shouldn’t expect much upside potential from the fund since it primarily focuses on income generation. Closed end funds have a common flaw where growth can be limited due to underperformance of the underlying assets. As a result, the NAV shrinks due to this underperformance in combination with the possibility that closed end funds typically take the distribution out of the net assets when performance can’t cover it. This is an important concept to understand so that expectations are realistic.

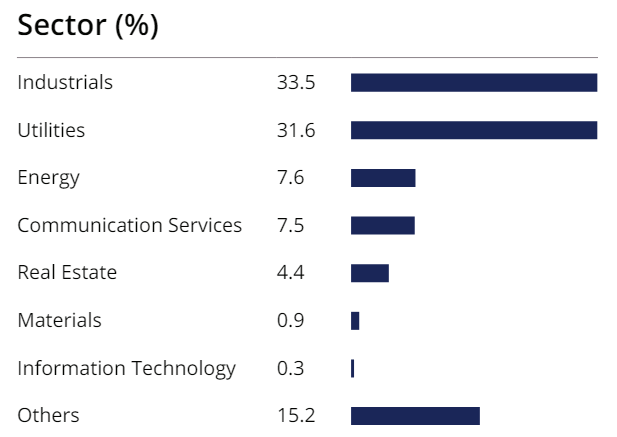

Since the fund has a focus on infrastructure, we can see that the top sectors are in areas that we deem essential to living a high quality life. This includes businesses that are exposed to roadways, railways, water treatment facilities, and electricity just to name a few. Industrials is leading the sector exposure, accounting for 33.5%. This is closely followed by utilities, which make up 31.6% of the fund. Industrials and utilities make up the majority of ASGI and all remaining sector weightings account for less than 8%.

ASGI Factsheet

It’s also worth noting that ASGI invests a substantial percentage of its net assets outside of the US. According to the most updated factsheet, North American exposure only accounts for 54.1% of the geographic composition. The second largest geographic exposure is within the Europe markets, accounting for 23%. ASGI also has varying amounts of exposure to Latin America, Asian markets, Africa, and the Middle East. For reference, here are the top ten holdings of ASGI.

| Holding | Weight % |

| NextEra Energy | 3.2% |

| Trinity Gas Holdings | 2.8% |

| Vinci SA | 2.6% |

| Engie SA | 2.6% |

| Aena SME SA | 2.5% |

| FERROVIAL SE | 2.5% |

| Zon Holdings | 2.4% |

| American Tower Corp | 2.4% |

| Cellnex Telecom SA | 2.4% |

| Norfolk Southern Corp | 2.4% |

An exposure mix like this can be seen as a double edge sword. On one hand, investing in infrastructure is something that can be seen as a no-brainer since we are collectively all looking for ways to improve our society as a whole. On the other hand, the industries that infrastructure operates within, typically relies on lots of debt financing and can be very sensitive to economic shifts and interest rates.

Dividend & Financials

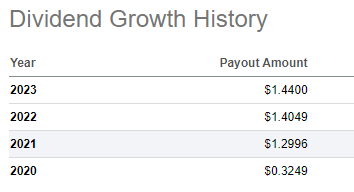

The dividend yield of ASGI currently sits at 12.5%. The distribution was recently raised in mid-June to $0.21 per share. Distributions are paid out on a monthly basis, and this is one of the things that makes ASGI such an attractive income focused investment. Even though the history of ASGI is quite short, we can already see the dividend growth taking place. We can see that the annual payout amounts have gradually increased since the fund’s inception.

Seeking Alpha

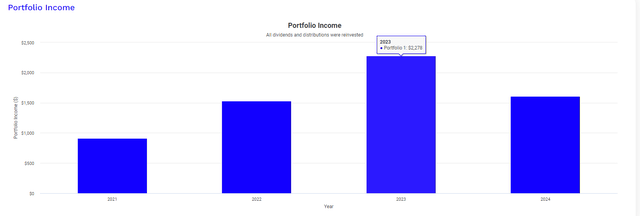

Even though the fund’s history is short, investors have had the opportunity to create a growing stream of dividend income. In order to prove this, I ran a back test using Portfolio Visualizer. This graph assumes an original investment of $10,000 at the start of 2021 and includes a monthly contribution of $500 to your investment throughout the entire holding period. In addition, it also assumes that all dividends received were reinvested back into ASGI to obtain more shares and create a snowball effect.

In the first year of your investment, you would have collected $909 in dividend income. This total would have grown to $2,278 by the end of 2023 due to the increased payout amounts combined with the continued monthly contributions added to your position. Over the next couple of years, I believe conditions will be improved for infrastructure, and we have a solid chance of seeing larger distribution increases as the fund’s performance improves.

Portfolio Visualizer

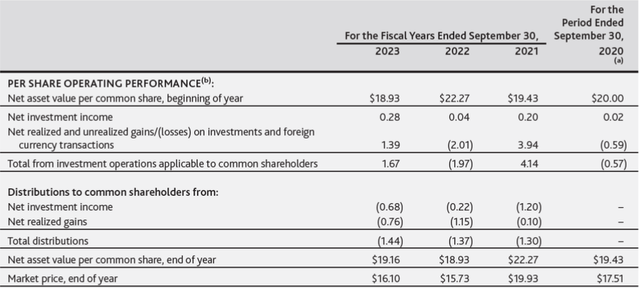

I am basing these assumptions on ASGI’s net investment income and realized gains performance so far over the last couple of years. Taking a look at ASGI’s 2023 annual report, we can see that the distribution for 2023 was fully covered by earnings. Net investment income amounted to $0.28 per share and while this may not have been impressive, it was offset by a strong net realized gain total of $1.39 per share. The combined total amounted to $1.67 per share, which fully covered the distribution amount of $1.44 per share.

ASGI 2023 Annual Report

The performance of 2023 was a large improvement over 2022’s performance. In 2022, we saw net investment income only amounting to $0.04 per share, while net realized losses amounted to $2.01 per share. This means that the performance of 2022 was not sufficient enough to fully cover the distribution of $1.37 per share for that year. However, something that I like about ASGI is that it retains some earnings from stronger years that can be used to cover the performance miss of underperforming years. In 2021, the net realized gains were very strong at $3.94 per share. This was a large excess over the distribution amount and as a result, the excess was retained and used over the course of 2022.

Although it hasn’t happened yet, I assume that if we encounter a scenario of multiple years of underperformance in a row, ASGI may have to use the return of capital to fund the distribution and make up the difference. As a fund that focuses on income generation and stability of distribution, I doubt that management would cut the distribution. For now though, there’s absolutely nothing to worry about as the distribution is fully supported and NAV has increased over the prior year.

Valuation

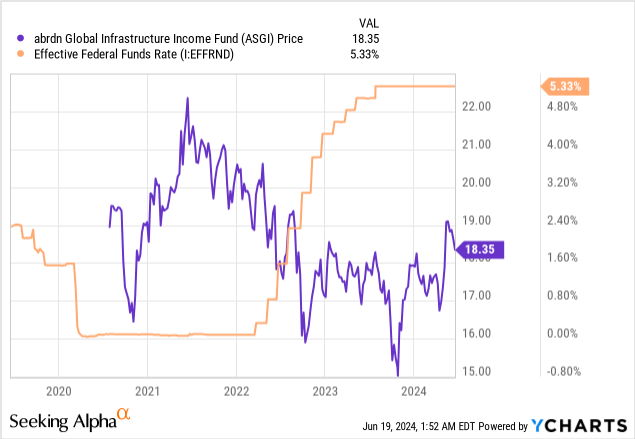

In terms of valuation, it sits slightly below its inception price of $20 per share, but I believe that future interest rate cuts may serve as a catalyst to the price growth of ASGI. Even though the fund’s history is short, we can already see the inverse relationship taking place between ASGI’s price and the federal funds rate. When the fund launched in 2020, rates were near zero levels and the price accelerated to the upside. Conversely, when interest rates were hiked to the current decade high, we can see that ASGI’s price quickly reversed directions and slide downward.

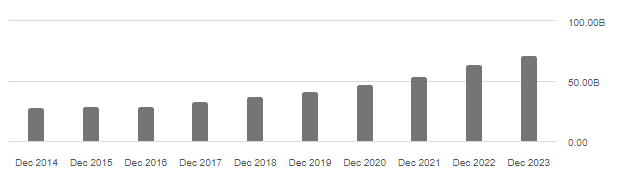

This sensitivity can be explained by the fact that ASGI’s most heavily weighted sectors typically rely on acquiring cheap debt as a way to fund operational growth. When debt is cheaper to access and maintain, we are likely to see increased growth initiatives from sectors such as utilities, energy, and industrials because they use this debt to fund different things such as acquisitions, plant development, research, and expansion of business operations. For example, ASGI’s largest holding is NextEra Energy (NEE) and the company currently sits on a large pile of debt totaling nearly $80B!

NextEra Energy Debt Total (Seeking Alpha)

Since ASGI operates as a closed end fund, the price can vary from the net assets. At the moment, ASGI trades at a discount to NAV of 7.5% and even though we can see this is higher than the historical average, I believe that this still serves as a great entry point. For reference, ASGI has traded at an average discount to NAV of 13.2% over the last three year period. In addition, I think that interest rate cuts may be on the horizon despite the Fed leaving rates unchanged at their last meeting. Additionally, inflation has slowly started to cool and get closer to the expected levels, which is an encouraging indicator. Lastly, the unemployment rate in the US has slowly crept to the 4% level and may end up peaking above this soon.

CEF Data

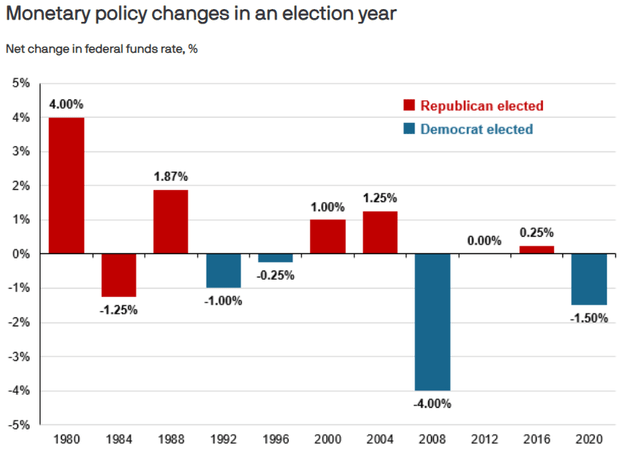

It seems like the Fed is still awaiting more economic data to roll in before making their decision around interest rates. However, another indicator that I believe rates are on the horizon is the fact that the US Presidential elections are coming up. Historically, the fed has made changes in the monetary policy for every election year dating back to 1980, with the exception of 2012. JPMorgan compiled an awesome graphic that shows us that rate cuts happen more frequently on election years, no matter which party is elected. There may be an elevated level of uncertainty and volatility in the markets around this time and this may encourage the Fed to initiate rate cuts.

JPMorgan

Vulnerabilities

Now that we’ve established that there’s a clear link between interest rates and ASGI’s main sector exposure, this reveals vulnerabilities. If we remain in an environment of higher interest rates for a longer period of time, we may see ASGI’s performance suffer. This is likely in the case of more interest rate hikes taking place as well. If ASGI has consistent periods of underperformance due to these macro influences, we may see deterioration of the NAV over time. Continued underperformance may also mean that return of capital needs to be used to help fund the distribution during periods where the net investment income or realized gains are not sufficient enough.

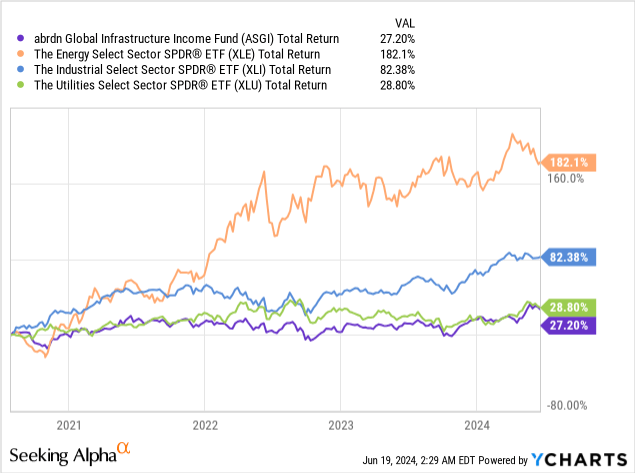

In addition, there is likely very little price upside that will be captured here over time. Unless you are an investor that is prioritizing income, you are likely to get a better total return if you were to just invest in ETFs that track these individual sectors. From a total return perspective, we can see that the energy sector (XLE), industrial sector (XLI), and utilities sector (XLU) have all outperformed ASGI despite having a much lower dividend yield.

This is just a typical symptom of closed end funds and doesn’t reflect anything necessarily wrong with ASGI. CEFs operate a bit different from traditional ETFs in a sense that they have a fixed number of shares, which can suppress the price appreciation potential. Additionally, since they are focused on distribution, closed end funds like ASGI usually are distributing out most of the earnings and not retaining and reinvesting enough to leave a meaningful impact on growth.

Takeaway

In conclusion, ASGI provides exposure to lots of infrastructure related sectors that are deemed to be essential parts of life. Therefore, investing in these sectors can be seen as steady, reliable, and predictable as their revenue streams are easier to forecast. However, the closed end fund nature of ASGI may limit growth potential, so if you are looking for consistent price appreciation, ASGI may not be the right choice for you. Conversely, if you are an income investor that is looking to capture a distribution that’s generated from this diverse sector mix, the high 12.5% yield on ASGI may be a good fit. Financials reveal that net investment income and net realized gains fully support the current distribution. In addition, the price trades at a current discount to NAV, but I can see this discount window get smaller as we approach interest rate cuts on the horizon. As a result, I rate ASGI as a buy.

Read the full article here