We previously covered ASML Holding N.V.(NASDAQ:ASML) (OTCPK:ASMLF) in April 2024, discussing why it remained a long-term winner as we entered the next cloud super cycle, thanks to the insatiable demand for generative AI SaaS and Nvidia’s (NVDA) double-digit growth.

Despite the growing bookings and multi-year backlog, we had also encouraged readers to wait for a moderate retracement for an improved margin of safety, preferably at its previous trading range of between $770s and $880s.

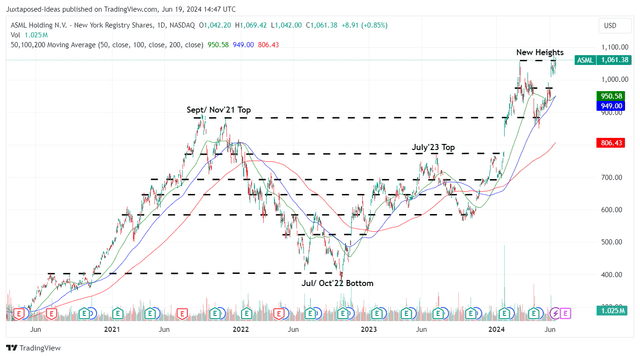

Since then, ASML has indeed pulled back by -13.4% to $850s by early May 2024, before recording another impressive rally of +24.4%. Even when comparing to the higher prices of $985.42 at the time of publication, the stock continues to perform relatively well at +6.6% compared to the wider market at +6.2%.

It is apparent that we are still at the early innings of hyper growth, with multiple semiconductor and server companies guiding robust numbers and intensified capex to capture the booming AI market.

With ASML currently constrained by capacity instead of demand and 2025 bringing forth drastically expanded manufacturing capabilities, we believe that it continues to offer robust long-term capital appreciation prospects, with competition still numerous years away from catching up.

ASML Is The Linchpin To The Next Cloud Super Cycle – Demand Remains Robust

ASML 4Y Stock Price

Trading View

For now, ASML has rallied to a new high and appears to be retesting its all-time heights of $1.06Ks while running away from its 50/ 100/ 200 day moving averages.

We believe that much of the tailwinds are attributed to the management’s recently raised FY2025 revenues to be at “the upper half of the guidance range” between €30B to €40B, with adj gross margin of up to 56%.

This is compared to the original guidance of between €24B to €30B offered in September 2021 and the raised guidance of between €30B to €40B in November 2022.

With 2025/ 2026 expected to bring forth raised annual production capacity to 600 units for DUV, 90 units for low NA EUV, and 6 units of High NA EUV (up to 20 by 2028), compared to 2023 levels of 396, 42, and 1 units, it is apparent that ASML’s top/ bottom lines are merely constricted by capacity and not demand.

This is especially when observing its “fully booked” position in 2024, robust multi-year backlog of €38B (-2.5% QoQ/ -2.5% YoY), and still healthy net bookings of €3.61B in FQ1’24 (-60.6% QoQ/ -3% YoY).

While some analysts lament about the “slipping demand” for ASML’s EUV machines in FQ1’24, we are not overly concerned since most of the orders are already in, with the lithography company set to ship multiple high NA EUV units to the top three global foundries in 2024 and Intel (INTC) already in the assembly process.

This is an important development indeed, since Taiwan Semiconductor Manufacturing Company Limited (TSM) has previously raised concerns regarding the expensive high NA EUV machines priced at $380M – capable of printing wafers at 8 nanometers thick.

This is compared to the previous generation of EUV machines at $180M for 13.5 nanometers thick.

It is apparent from these developments that none of the foundries are willing to take chances during the ongoing generative AI boom, since the high NA EUV machines are capable of producing the highest-end “AI applications and advanced consumer electronics.”

This is especially since it remains to be seen when the foundries may be able to achieve the same economy of scale and profit margins using the higher specification machines, when the older EUV machines are equally capable in producing the next-gen semiconductor chips.

Either way, with ASML’s high NA EUV capacity already fully booked in 2024 with more deliveries staggered through 2025, it is apparent that its prospects remain extremely bright as the generative AI boom triggers intensified foundry capex.

ASML, NVDA, TSM, & SMCI 1Y Stock Price

Trading View

We do not expect this boom to wane anytime soon as well, with NVDA recently reporting robust FQ1’25 revenues of $26.04B (+17.8% QoQ/ +262.1% YoY) while guiding FQ2’25 revenues of $28B (+7.5% QoQ/ +107.4% YoY), well exceeding the consensus estimates of $24.56B and $26.84B, respectively.

Despite so, the consensus continues to raise their forward estimates with NVDA expected to report another doubling in revenues to $120.01B in FY2025 (+96.9% YoY) and a further doubling to $245.91B by FY2029 (expanding at a CAGR of +32.2%).

Given the robust demand for AI chips over the next few years, it is unsurprising that TSM has highlighted intensified FY2024 capex, with up to 80% reserved for advanced process technologies.

The same has been highlighted by Super Micro Computer, Inc. (SMCI), a company offering complete server solutions, with the management raising their FY2024 top/ bottom-line guidance while drastically expanding their manufacturing capacities over the next two years.

Readers must also not forget that the automotive and renewable energy end markets are increasingly consuming more semiconductor chips, with ASML likely to enjoy multiple growth drivers moving forward, along with NVDA and TSM, as observed in their stocks’ massive rallies over the past year, well exceeding the wider market.

So, Is ASML Stock A Buy, Sell, or Hold?

For context, we had offered a fair value estimates of $769.60 in our previous article, based on ASML’s 1Y P/E mean of 35.55x then and the FY2023 adj EPS of $21.65, as the management also reiterates their guidance of FY2024 sales to be similar to FY2023 (and likely in adj EPS performance).

ASML Valuations

Tikr Terminal

Since then, ASML’s FWD P/E valuations continues to climb to 44.57x, nearing the peak of 47x observed in November 2021 before the painful market wide correction occurred.

While we concur that ASML has an “effective monopoly on the world’s most advanced chip-making machines and technology,” this also meant that it may be hard to relatively value the stock, with the closest currently being Canon (OTCPK:CAJPY) priced at FWD P/E at 13.13x.

On the one hand, we believe that ASML’s 20Y moat is unlikely to be contested, with CAJPY’s nanoimprint lithography machines likely used for the “production of memory chips before expanding to other areas.“

Market analysts already expect minimal commercial impact for CAJPY over the next few years, attributed to the “big gap in research and development or concept capability at leading-edge nodes… vs. high-volume execution and [being] manufacturing ready, and that’s the challenge.”

On the other hand, with ASML’s consensus forward estimates unchanging over the past few months, we believe that it may be more prudent to maintain our original fair value estimate of $769.60 using the more reasonable 1Y P/E mean of 35.55x, with it also offering interested investors with an improved margin of safety.

We are maintaining our 2Y price target of $1.29K as well, as discussed in our previous article based on the consensus FY2026 adj EPS estimates of $36.50, with there remaining an excellent upside potential of +21.6% from current levels despite the stock’s recent rally.

As a result of the attractive risk/ reward ratio, we are reiterating our Buy rating for the ASML stock though with no specific entry point, since it depends on individual investors’ dollar cost average and risk appetite.

With the stock currently retesting its all-time heights of $1.06Ks, interested investors may want to observe the stock movement for a little longer and adding upon a moderate retracement to its previous trading ranges of between $915s and $970s for an improved margin of safety.

We believe that ASML remains the linchpin to the next semi super cycle, significantly aided by the Semiconductor Nationalism observed after the COVID-19 pandemic, with us recommending investors to always buy the dip.

Risk Warning

As discussed above in our valuation section, it is apparent that the market is overly exuberant about the prospects of generative AI and the resultant impact on foundry capex.

While we believe in the multi-year demand for AI chips with the world still in the early innings of the next cloud super cycle, readers must also note that with the new foundries in Arizona set to be operational from 2027 onwards, we expect to see a slowdown in bookings once most of their fit outs are completed.

At the same time, ASML’s expanded capacity also means that we are likely to see its multi-year backlog moderate from 2025 onwards, with consumers placing orders as needed instead of doing so in advance and consequently triggering reduced visibility into its intermediate term top/ bottom lines.

As a result, investors may also want to temper their intermediate term expectations and avoid being disappointed.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here