Investment Thesis

Astera Labs, Inc. (NASDAQ:ALAB) has an impressive story, one of being well-positioned to meet the growing capex spend of hyperscalers.

And also, along with its narrative, its very near-term revenue growth rates look eye-popping.

And yet, I believe that once we get beyond Q2 2024, its revenue growth rates will significantly decelerate to around 130% compared with more than 500% which is expected for Q2 2024.

Moreover, to further complicate matters, I believe that even with some strong growth, this barely free cash flow breakeven stock is priced at around 28x forward sales.

All in all, I struggle to see its upside potential. But at the same time, I’m no longer bearish either. I’m on the fence here.

Rapid Recap

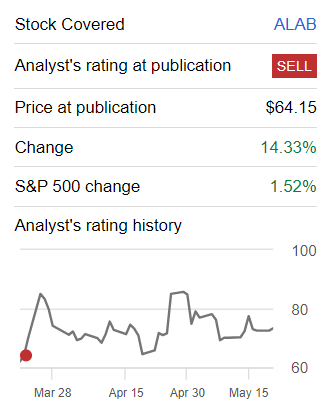

Back in March, I said in a bearish article,

The business looks squeaky clean, with its strong balance sheet and alluring narrative.

However, once we dig into its financials, we can see that this stock, priced at 33x forward sales, is not quite as compelling as it first appears. Therefore, I’m rating Astera Labs, Inc. stock as a sell, notwithstanding its meme-like momentum.

Since that time, the stock has been very volatile, but it has in earnest moved higher, see below.

Author’s work on ALAB

Today, I’m more on the fence about ALAB’s prospects. It’s not a clear-cut sell rating on this stock.

Why Astera Labs? Why Now?

Astera Labs develops technology to help computers communicate faster and more efficiently. They create special chips and software that enable large computer systems, such as those used in cloud computing and AI, to connect and share data quickly. Their products solve the problems that come with processing large amounts of data, helping companies build faster and more reliable systems for AI and data analysis.

Astera Labs works with major companies that build large-scale computer systems, supplying them with millions of devices. This growth is driven by the high demand for their solutions.

Moving on, Astera Labs has developed innovative solutions to address connectivity bottlenecks in AI and cloud computing, partnering with leading hyperscalers and AI platform providers. As AI model sizes continue to expand rapidly, Astera Labs’ products, are increasingly in demand to manage the growing data processing requirements.

The pitch here is that Astera Labs is well-placed to capitalize on the capex of hyperscalers, who are ramping up their AI infrastructure deployments to meet the rising demand for advanced AI capabilities.

However, there are challenges too. For instance, Astera Labs’ revenue growth is fully tied to the capex cycle of hyperscalers. So if there’s a slowdown in spend by the major hyperscalers this would impact its growth rates as it did in late-2022 to mid-2023.

Given this background, let’s now discuss its financials.

Revenue Growth Rates Require Interpretation

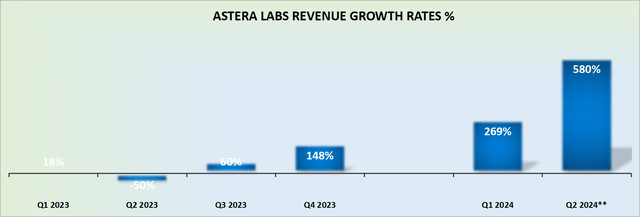

ALAB revenue growth rates

It’s not immediately obvious, but Q2 of the prior year saw Astera Labs’ revenue growth rates fall 50% y/y. Naturally, on the back of some growth, Astera’s growth rates were always going to shine strongly this time around.

That being said, the key question we truly have to get to grips with is, what sort of growth rates can we expect beyond H1 2024?

The problem here is that growing off a small base is relatively easy. Sign a few contracts, and suddenly, the company’s revenue growth rate looks nothing short of a ”generational opportunity.”

Indeed, once Astera Labs gets closer to $100 million in revenues, moving beyond that, its growth rates will start to normalize somewhat.

And my question is this, what sort of normalized growth rates can we expect from Astera? Remember, starting Q4 2022, its revenues were shrinking into Q2 2023, for those 3 consecutive quarters (page 76). So, it’s not impossible for this to happen once again, and therefore I feel apprehensive to be too aggressive with this extrapolation.

Nevertheless, my job is to take some sort of view on its normalized growth rates into its future growth rates. Allow me to provide an illustration.

Let’s say that Astera Lab’s revenue growth rates in Q3 grow by approximately 10% from Q2 2024. This would put its revenue growth rates in the ballpark of $85 million. And that would mean that ALAB would then only be growing at 130%, which, is a steep deceleration from the 580% y/y revenue growth rate it’s expected to report in Q2 2024.

Given this context, let’s now discuss its valuation.

ALAB Stock Valuation — 28x Forward Sales

Let’s make the case that ALAB’s forward revenues reach $400 million as a forward run rate at some point in early 2025. A figure that is well within its reach.

Given that revenue, the stock today is priced at 28x forward sales. A figure that I believe really leaves very little room to maneuver. Particularly when we consider that the business is only just about breaking even on the free cash flow line.

That being said, given its IPO proceeds, the business is very well capitalized with approximately $800 million of cash and equivalents (including marketable securities) with no debt.

The Bottom Line

In conclusion, Astera Labs presents a complex investment case. While its near-term revenue growth rates are impressive, I anticipate a significant deceleration beyond Q2 2024.

The stock’s current valuation of around 28x forward sales, coupled with its just-breakeven free cash flow status, leaves me concerned about its upside potential.

Despite its strong positioning to capitalize on the capex spend of hyperscalers and robust financial backing, I find myself on the fence regarding its future prospects.

Thus, I am neither bullish nor bearish on Astera Labs, Inc. stock now.

Read the full article here