Investment Thesis

I believe Automatic Data Processing (NASDAQ:ADP) stock is a buy. The company’s strategic positioning in the growing HR solutions market, high client retention rates, and strong financials make it a compelling investment opportunity. With a robust ROIC and a history of shareholder value creation through share repurchases and dividends, ADP demonstrates financial strength. Moreover, a conservative estimate projects a five-year price target of $424.67, implying an 11% Compound Annual Growth Rate from today’s share price of $245.31. Given these factors, ADP appears to be a promising buy for investors looking for both growth and stability.

Company Overview

Automatic Data Processing offers human resources software and services, including payroll processing and benefits administration. The company operates on a subscription-based business model, where clients pay fees for cloud-based software. They also provide services like tax filing and compliance. ADP serves a range of clients, from small businesses to large enterprises, in various industries. ADP’s revenue comes mainly from two segments: Employer Services and Professional Employer Organization (PEO) services. Employer Services offers HR software, while PEO services provide outsourced HR functions. The company operates globally, in over 140 countries. ADP competes with companies like Paychex (PAYX), Workday (WDAY), and Ceridian HCM Holding Inc. (CDAY). These competitors offer similar services and differentiate mainly through pricing and features.

ADP To Benefit From Structural Industry Trends

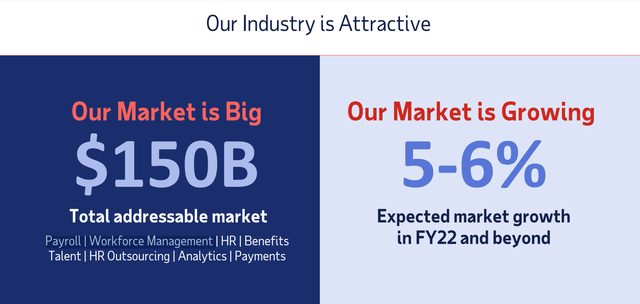

In my opinion, Automatic Data Processing will benefit from the expected 6% growth in demand for Payroll and Workforce Management software. Several factors support this view.

ADP 2023 Investor Presentation

In my opinion, the intricate landscape of labor laws and tax regulations creates significant challenges for businesses, especially when it comes to managing payroll. ADP’s expertise in this specialized area provides it with a competitive advantage. Many businesses, particularly those that are small to medium-sized, often lack the internal capabilities to navigate these complexities. ADP fills this gap by offering outsourcing solutions, which not only save time but also mitigate the risks associated with errors and compliance issues. Furthermore, ADP’s reputation for being reliable makes it a go-to option for companies seeking dependable payroll services. The company’s agility in adapting to ever-changing regulations adds another layer of appeal, as it can swiftly update its systems to maintain compliance.

I believe the digital transformation trend is not only expanding ADP’s customer base but also offering tangible benefits to small and medium-sized enterprises (SMEs) in terms of operational efficiency and cost savings. One of the most significant advantages is the reduction in labor required to complete payroll and HR activities. Traditionally, these tasks would involve manual data entry, calculations, and compliance checks, which are both time-consuming and prone to errors. Cloud-based HR solutions from ADP automate many of these processes, allowing businesses to reallocate human resources to more strategic activities. This automation directly impacts the bottom line by reducing labor costs associated with HR and payroll management. Moreover, the efficiency gains from automation can lead to quicker decision-making and more streamlined operations. For instance, automated time-tracking and attendance systems can feed directly into payroll calculations, reducing the time needed to close payroll cycles. This efficiency not only saves time but also reduces the likelihood of costly errors, such as overpayments or compliance fines.

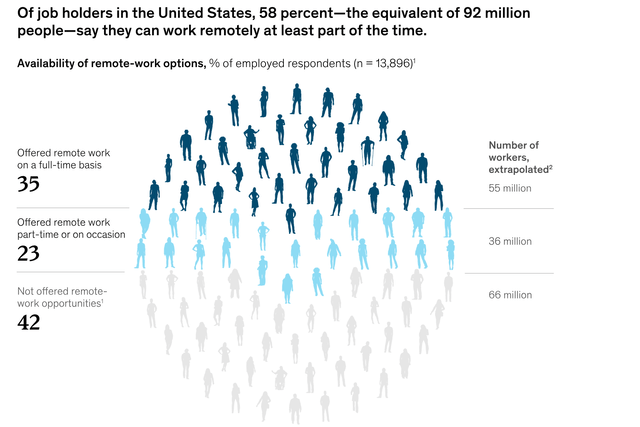

Personally, I think the rise of remote work is a pivotal factor that could boost ADP’s market share in HR and payroll solutions. A survey study completed by McKinsey revealed that 58% of American workers said they could work remotely at least part-time. This statistic underscores the growing complexity of workforce management, as businesses now have to manage employees who are spread across various locations and potentially different time zones. This dispersed work environment increases the need for efficient, cloud-based HR software capable of handling these new challenges, something that ADP specializes in. Coupled with ADP’s international operations—15% of its revenue comes from markets outside the U.S.—the company is well-positioned to capitalize on these trends. Its global presence allows it to tap into similar remote work trends and HR outsourcing needs worldwide, further diversifying its revenue streams and growth opportunities.

McKinsey & Company

Additionally, ADP’s operations in over 140 countries give it a unique advantage in tapping into international market trends, such as the growing trend of outsourcing HR functions. Interestingly, 15% of ADP’s revenue currently comes from international markets, indicating a significant foothold outside the U.S. This international presence not only diversifies its revenue streams but also provides opportunities for growth as more businesses globally adopt digital HR solutions.

ADP 2023 Investor Presentation

ADP Has a “Switching Moat”

In my opinion, ADP’s strong “switching moat” and impressive client retention rates make it a resilient and dominant player in the HR and payroll solutions market. Once a business integrates ADP’s services, the inconvenience and risks associated with switching to a competitor—such as the need to migrate data, reconfigure settings, and retrain staff—create a form of customer lock-in. This is further complicated by the potential for serious financial and legal repercussions due to errors during the transition. ADP’s Q4 2023 conference call revealed a retention rate increase of 10 basis points, bringing them back to a record level of 92.2%, even while absorbing market normalization impacts. This strong performance was especially notable in ADP’s U.S. mid-market and international businesses and was accompanied by record-level client satisfaction in the fourth quarter. These metrics validate ADP’s ability to deliver reliable, high-quality services that keep clients loyal, thereby enhancing its competitive moat.

Shareholder Friendly Capital Allocation

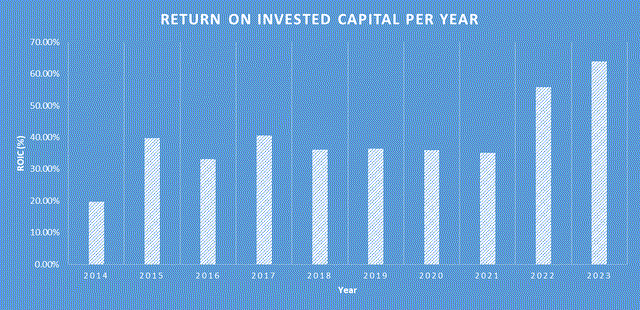

ADP boasts an excellent Return on Invested Capital, commonly reaching around 30%. This strong ROIC is fueled by a combination of organic reinvestment and strategic mergers and acquisitions (M&A). On the organic side, investments into Systems Development and Programming have been key drivers of growth. In terms of M&A, ADP has made effective acquisitions that complement its core business, including Global Cash Card, WorkMarket, and Celergo. These acquisitions have not only expanded ADP’s service offerings but also contributed to its impressive ROIC.

DJTF Investments

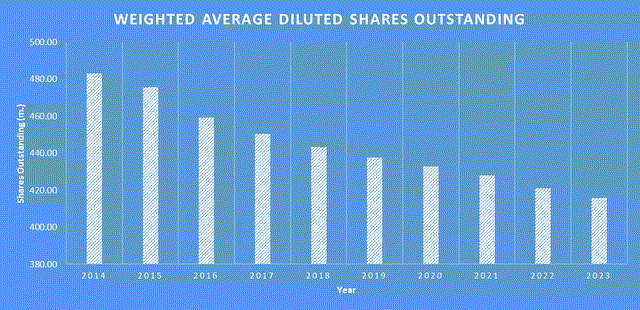

ADP has consistently returned capital to shareholders through share repurchases. From 2014 to 2023, the company reduced its share count from 483.10 million to 415.70 million, representing an annual decrease of approximately 1.5%. This strategy enhances shareholder value by effectively distributing profits back to investors and boosting earnings per share.

DJTF Investments

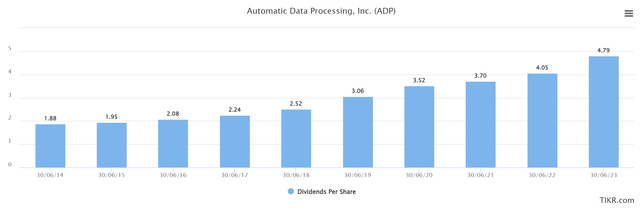

In my view, ADP’s dividend program is noteworthy for its consistency. The company targets a payout ratio of 55-60% and has increased its dividend for 48 consecutive years. The dividend per share rose from $1.88 in 2014 to $4.79 in 2023, marking an annual growth rate of about 11.5%. This track record suggests that ADP is focused on returning value to shareholders.

Tikr Terminal

Financial Analysis

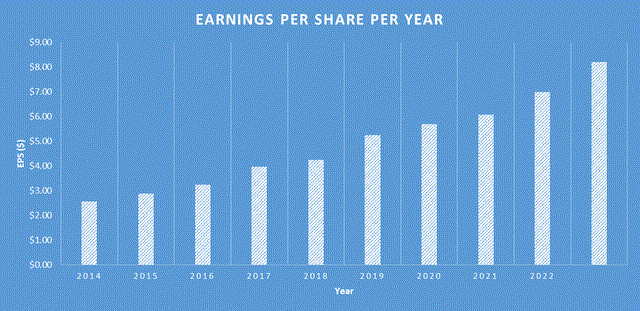

Over the past 5 years, the company has demonstrated remarkable financial performance. Its revenue has shown a consistent growth, increasing from $12,807.70 million in 2018 to $17,198.80 million in 2023, representing a compound annual growth rate (CAGR) of 6%. The earnings per share (EPS) have grown steadily from $4.25 to $8.21, reflecting the company’s ability to translate revenue growth into bottom-line success.

DJTF Investments

As of the most recent quarter, the company reported cash and cash equivalents of $2,098.20 million. The company’s total debt stands at $2,989.00 million, a modest amount that can be paid back in 1 years’ worth of free cash flow, reflecting the company’s conservative approach to leverage. The company’s current ratio, a measure of its ability to cover short-term liabilities with short-term assets, is 1.00, which is generally considered healthy.

In my view, ADP is well-positioned for future growth due to factors like digital transformation, increasing remote work, and international presence. The company’s strong financials, high client retention rates, and expertise in navigating complex regulations further strengthen its outlook. Additionally, its history of effective acquisitions suggests multiple avenues for expansion.

Valuation

When considering valuation, I always consider what we are paying for the business (the market capitalisation) versus what we are getting (the underlying business fundamentals and future earnings). I believe a reliable way of measuring what you get versus what you pay is by conducting a discounted cashflow analysis of the business as seen below.

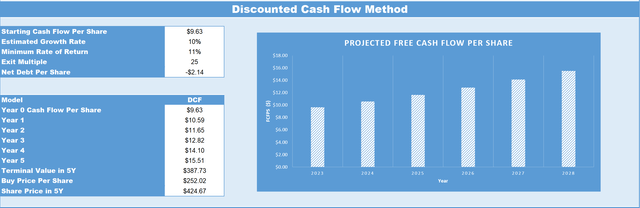

ADP’s current LTM Cashflow per Share as of Q4, 2023 is $9.63. I believe that ADP’s Cashflow per Share should grow conservatively at 10% annually for the next five years. Therefore, once factoring in the growth rate by Q4 2028 ADP’s Cashflow per Share is expected to be $15.51. If we then apply an exit multiple of 25, which I have deemed as a fair multiple based off ADP’s past price to free cashflow ratio for the previous 10 years, this infers a price target in five years of $424.67. Therefore, based on these estimations, if you were to buy ADP at today’s share price of $245.31, this would result in a CAGR of 11% over the next five years.

DJTF Investments

Conclusion

ADP presents itself as a compelling buy in the current market. The company is strategically positioned to capitalize on growing trends in labor laws, digital transformation, and remote work. Its high client retention rates and significant barriers to switching underscore its dominant role in the HR solutions sector. Financially, ADP is robust, often achieving an ROIC of around 30%. It has consistently returned value to shareholders through share repurchases and a strong dividend program. Furthermore, with a conservative estimate of 10% annual growth in Cashflow per Share, the company’s five-year price target is projected to be $424.67. This suggests an 11% Compound Annual Growth Rate from today’s share price of $245.31.

Read the full article here