Today, we are putting Axsome Therapeutics, Inc. (NASDAQ:AXSM) in the spotlight for the first time in several years. The shares of this mid-cap biopharma have had somewhat of a bumpy ride over the past 12 months. Axsome made Mizuho Securities short list for stock of the month in the healthcare space early in July. The company has a couple of products approved and on the market, and several others in late-stage development. What is ahead for Axsome in the quarters ahead? An analysis follows below.

Seeking Alpha

Axsome Therapeutics is headquartered in New York City. This biopharma is focused on the development of novel therapies for central nervous system or CNS disorders. The company has approved drugs on the market:

Sunosi – This a compound approved for the treatment of excessive daytime sleepiness in patients with narcolepsy or obstructive sleep apnea. Sunosi was acquired from Jazz Pharmaceuticals (JAZZ) in 2022 for an upfront payment of $53 million, and the company pays JAZZ high single digit royalties on sales. Phase 3 trials to evaluate Sunosi to treat major depressive disorder or MDD and binge-eating disorder were recently initiated. Topline results from a Phase 3 trial evaluating Sunosi to treat ADHD should be out before the end of the year as well.

Auvelity – This is a N-methyl-D-aspartate receptor antagonist with multimodal activity, greenlighted for the treatment of MDD. Auvelity was blessed by the FDA in the summer of 2022.

The stock currently trades around $85.00 a share and sports an approximate market capitalization of just north of $4 billion.

Axsome Therapeutics also has several candidates, mid to late-stage development, within its pipeline.

June 2024 Company Presentation

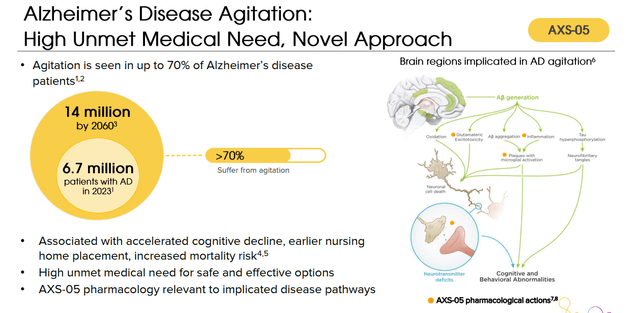

AXS-05 – An oral, investigational NMDA receptor antagonist with multimodal activity that is a proprietary formulation of a combination of dextromethorphan and bupropion. AXS-05 has completed a Phase 2 clinical trial for the treatment of smoking cessation and is being evaluated in a Phase 3 study to treat Alzheimer’s disease agitation. The compound has Breakthrough Therapy designation for this indication. A pivotal trial evaluating AXS-05 to treat smoking cessation should kick off before this year is out as well.

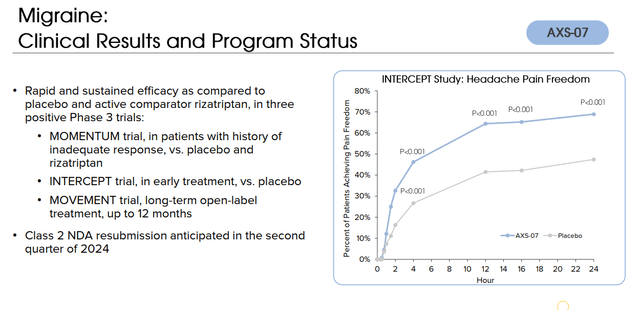

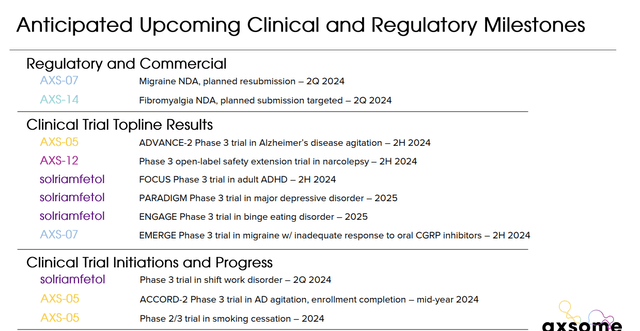

AXS-07 – A combination meloxicam and rizatriptan that results in an oral, rapidly absorbed, multi-mechanistic compound that has completed Phase 3 studies for treating acute migraines. The company plans to resubmit is marketing application for AXS-07 for this indication before the end of 2024.

June 2024 Company Presentation

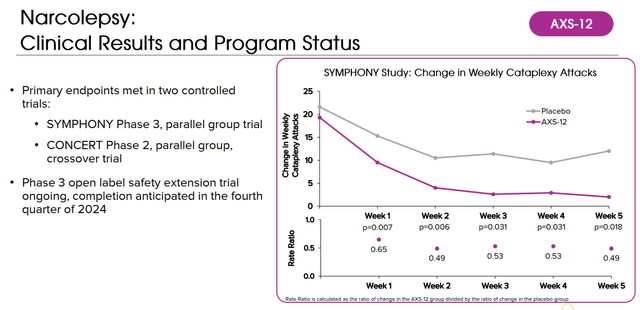

AXS-12 – A highly selective and potent norepinephrine reuptake inhibitor. AXS-12 has successfully completed Phase 2 testing and now is being evaluated in a Phase 3 trial to treat narcolepsy.

June 2024 Company Presentation

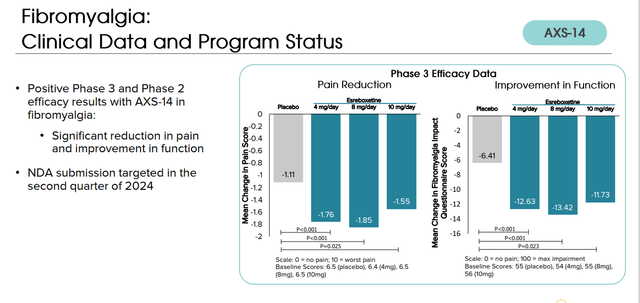

AXS-14 – Another highly selective and potent norepinephrine reuptake inhibitor. AXS-14 has produced primary endpoints and demonstrated positive and statistically significant results in both Phase 2 and Phase 3 studies for the treatment of fibromyalgia. A marketing application for this indication should be submitted any week now.

June 2024 Company Presentation

Recent Results:

Axsome Therapeutics posted mixed Q1 numbers on May 6th. The company posted a GAAP loss of $1.44 a share, over 20 cents a share below the consensus. SG&A costs rose significantly to $99 million compared to $74.2 million from the prior period a year ago. This was primarily due to an expansion of Axsome’s sales force.

Revenues fell just over 20% on a year-over-year basis to $75 million, which was $2 million above expectations. Net product revenues for Sunosi came in at $21.6 million for the quarter. This represented 64% year-over-year growth. The product had 42,000 prescriptions for the quarter, down slightly from 4Q2023. Auvelity net product products rose 240% to $53.4 million. 95,000 prescriptions were written during the quarter, a 12% sequential increase from the fourth quarter.

Analyst Commentary & Balance Sheet:

The analyst community is positive on the prospects of Axsome Therapeutics currently. Since first quarter results hit the wires, 10 analyst firms including Piper Sandler, Morgan Stanley and Citigroup have reissued/assigned Buy or Outperform ratings on the stock. Price targets range between $100 to $190 a share, with most estimates in the $115 to $130 range. Bank of America maintained its Hold rating and AXSM following quarterly results.

Axsome Therapeutics ended the first quarter with just over $330 million in cash and marketable securities on its balance sheet. The company did post a net loss for the quarter of $68.4 million, of which $21 million was for non-cash charges. Management has stated it has cash on hand to reach positive cash flow status. Several insiders have sold off just over $8 million worth of share collectively since last September. Prior to that there had been no insider activity in the stock since late in 2021.

Conclusion:

Axsome Therapeutics lost $5.27 a share on just over $270 million in revenues in FY2023. The current analyst firm consensus has losses coming down somewhat to $4.74 a share FY2024 on just under $378 million in sales. They project a huge reduction in red ink in FY2025 with losses of just under 50 cents a share as revenues are expected to surge by just under 80%.

June 2024 Company Presentation

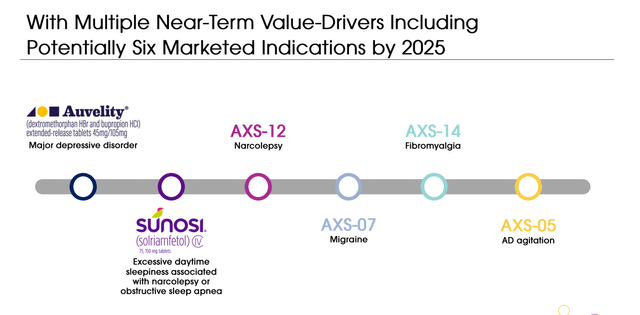

There is a lot to unpack around the investment case around Axsome Therapeutics as the company could have a half dozen approved products by the end of 2025. In addition, Axsome Therapeutics is targeting some significant potential markets.

June 2024 Company Presentation

I admit I have a soft spot for the company as it was one of the few 10-baggers I have had as an investor, and I first wrote positively about this company in 2018 when the stock traded at under three bucks a share. I took huge profits on that stake some years ago. Since then, I have successfully executed covered call trades around the stock. Options against the stock are liquid and lucrative. In addition, the shares seem to have one or two significant dips annually. This is how I currently have a stake in AXSM.

If analyst firm projections hold, Axsome could become profitable as soon as FY2026 and management has stated it has no need to do a dilutive capital raise to achieve positive cash flow status. That said, the stock is trading at nearly FY2025E sales. Pricey, but not outlandish given the potential of Axsome’s pipeline. For patient, long-term investors, accumulating a stake over time via straight equity in this growth play seems prudent, particularly if the stock dips back in the low to mid $70s range.

June 2024 Company Presentation

Read the full article here