China’s leading AI technology and search leader, Baidu, Inc. (NASDAQ:BIDU), demonstrated that its recovery continues despite the stumbles in China’s economic recovery.

As such, BIDU has outperformed China’s e-commerce and cloud leader Alibaba (BABA) stock since January 2023, suggesting buyers seem confident about its AI growth prospects.

Baidu’s recent second-quarter or FQ2 earnings release lifted investors’ confidence about its ambitions to integrate AI into every aspect of its products and services. Bolstered by its robust search data advantage and deep-rooted full-stack ecosystems, Baidu is well-primed to maintain its AI leadership in the generative AI era.

Therefore, I’m not surprised that BIDU is now my preferred Chinese stock pick, as its core business has demonstrated a remarkable revival despite China’s economic malaise. The company’s well-diversified verticals mitigated the impact of weak physical goods spending, bolstering strong growth in online marketing revenue.

Accordingly, management telegraphed “strong performance observed in sectors like healthcare, business services, local services, and travel.” In addition, it also saw “robust” e-commerce performance, leveraging China’s ad market recovery.

Furthermore, Baidu indicated that AI engagement has increased among its active user base, leading to more effective search queries and results. In addition, Baidu also indicated improved monetization on advertisers’ ROAS, bolstering Baidu’s search market leadership.

Investors must note that Baidu is by far the most significant search advertising leader in China. Given its astute and early investments in AI, it has positioned the company exceptionally well to capitalize on China’s ambitions on the global AI stage.

Management stressed that few companies possess the scale and data advantage to develop highly advanced large language models or LLM, such as its rapidly evolving Ernie LLM. Therefore, generative AI is expected to be a sustaining innovation for Baidu to entrench its wide economic moat further and help it penetrate the AI cloud market, dominated by Alibaba, Tencent (OTCPK:TCEHY), and Huawei.

Moreover, Baidu’s AI leadership on autonomous ride-hailing has broadened, leading to higher operating efficiencies as it scales. Permits were approved for Baidu to “conduct fully driverless testing on open roads in the Shanghai Pudong area.” It adds further to the company’s deployment in Beijing, Shenzhen, Wuhan, and Chongqing.

Revised analysts’ estimates suggest Baidu’s operating leverage growth story is still in the early innings. However, investors should expect near-term margin dilution from its ongoing investments in its robotaxi business and generative AI. However, these are critical long-term growth optionalities in Baidu’s margin trajectory moving forward that could solidify its AI leadership in the vast Chinese economy. Monetization efforts are still very early, indicating significant opportunities for growth, particularly if Baidu could improve its competitive edge against China’s cloud computing leaders.

Seeking Alpha Quant’s “A-” growth grade corroborates my conviction of its growth thesis. Underpinned by a best-in-class “A” profitability grade, I have confidence in Baidu’s ability to execute its growth optionalities. Moreover, its valuation is attractive, as the market discounted the geopolitical uncertainties, with a Quant valuation rating of “B-.”

Critically, I also gleaned constructive buying sentiments amid the challenging backdrop, indicating investors have been buying significant dips in BIDU.

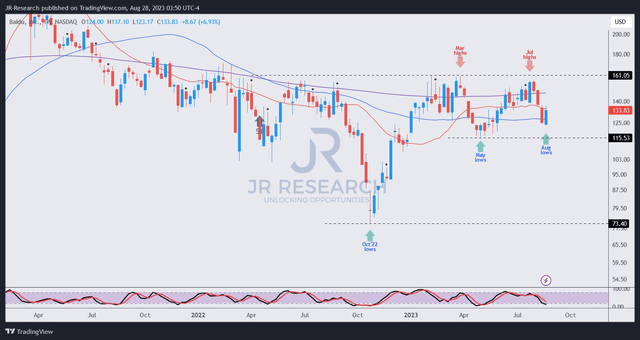

BIDU price chart (weekly) (TradingView)

BIDU buyers have robustly defended its March 2023 lows, even as it saw a steep three-week selloff before its recent FQ2 earnings release. Buyers look ready to support another bottoming process in BIDU, leading to a higher high market structure.

While a pullback toward its March lows cannot be ruled out, given the recent market volatility, I see that as another opportunity to add exposure rather than sell in a panic.

BIDU needs to break decisively above the $160 level, which is unlikely in the near term unless buying sentiments improve markedly. Notwithstanding that caution, I urge investors to capitalize on the recent market pessimism to add more shares as China’s AI leader looks ready to resume its market outperformance.

Rating: Maintain Buy. Please note that a Buy rating is equivalent to a Bullish or Market Outperform rating.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here