Investment Thesis

I recommend holding Banco Bradesco S.A. (NYSE:BBD) shares. The process of banking digitization and increased competition has hit the bank’s results hard, which presents the most depreciated financial indicators in the sector.

However, the bank’s managers seem to have seen this, even if belatedly, and are making a series of changes to the company’s corporate structure, processes, and culture.

Despite being cheap, to make an analogy, the bank is a transatlantic ship turning around, and I prefer to wait for a more robust improvement in results before recommending buying the shares.

Introduction

Before the Brazilian banking sector suffered competition from neobanks such as Nu Holdings Ltd. (NU), Inter & Co, Inc. (INTR) and others, it had an oligopolistic characteristic, dominated by private players such as Itaú Unibanco Holding S.A. (ITUB), Banco Santander (Brasil) S.A. (BSBR) and Banco Bradesco S.A. (BBD), and state players such as Banco do Brasil S.A. (OTCPK:BDORY) and Caixa Econônica.

Local characteristics are also entirely different from other markets, as results from services such as cards, investments, and insurance are very relevant for local banks. Another local characteristic is that only 3% of the Brazilian adult population does not have a bank account.

An important observation is that, although banks compete with each other, they have sought to focus on certain customer profiles. Bradesco, for example, has always focused on classes with lower disposable income.

And this became a problem as the last cycle of rising interest rates brought record inflation to this public, and Nu consolidated itself as a major player, serving more than half of the Brazilian population and becoming notable for being able to operate in a healthy manner in a segment with so much delinquency. But before we talk more about the competitive environment, we have to take a step back and learn more about Bradesco.

History and Business Model

Bradesco is the third-largest private bank in Brazil by market value, behind Nu and Itaú. The bank offers a range of financial products and services to retail and wholesale customers, and has a dominant position in the life insurance and pensions market.

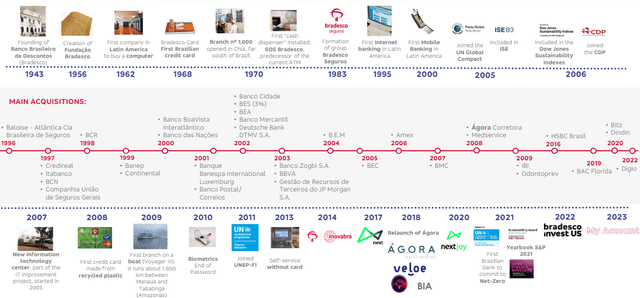

Bradesco currently has more than 10% of domestic credit operations, as well as more than 14% of payroll loans. Below is their timeline until the present day:

History (IR Company)

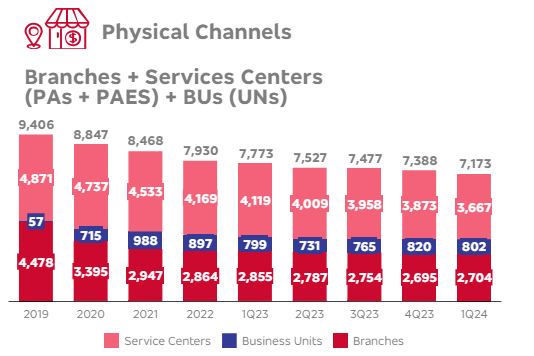

Bradesco has 71 million customers, serving a population of 38.3 million account holders through its network of physical branches, which has 2,704 units in operation.

Physical Channels (IR Company)

Now, we will delve deeper into the company’s credit portfolio and customer profile, and later we will carry out a financial analysis of Bradesco and its competitors.

Loan Portfolio

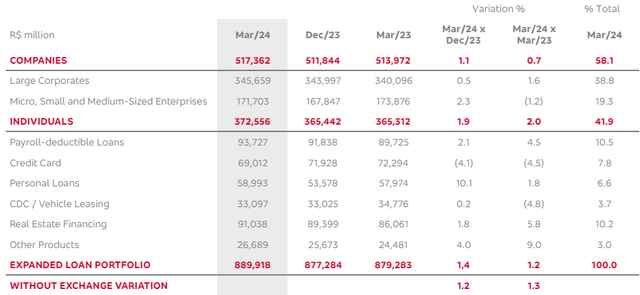

Historically, Bradesco has opted for a diversified portfolio, high provision for doubtful debt reserves and disciplined risk management. Currently, the bank indicates that 38.8% of its credit portfolio is made up of the large corporate segment, 19.3% of SMEs, 10.5% of payroll loans, and 10.2% of real estate financing.

Expanded Loan Portfolio (IR Company)

However, due to the challenges imposed by the economic scenario, the bank has a more diligent credit-granting policy, which has even reduced provisions for loan losses in recent quarters.

This information already corroborates my thesis of holding the shares. However, now we are going to carry out a financial analysis of the company against its peers to understand the impacts that competition has had on results, and then talk a little about valuation and prospects.

Bradesco Fundamentals

In the following, I will use Seeking Alpha data to compare Bradesco with its peers in Brazil, like Itaú Unibanco Holding S.A. (ITUB), Banco Santander (Brasil) S.A. (BSBR), Banco do Brasil (BDORY) and Nu Holdings Ltd. (NU).

| Name | Bradesco | Itaú |

Banco do Brasil |

Nu |

Santander |

| Market Cap | $26B | $59B | $31B | $55B | $20B |

| Net Income TTM | $2.6B | $7B | $6.2B | $1.3B | $1.9B |

| Net Income Margin | 19.2% | 27% | 28% | 29.7% | 23% |

| Net Income CAGR 3Y | -11% | 19% | 31.5% | – | -11.4% |

| Loan Portfolio | $177B | $181B | $227B | $20B | $103B |

| ROE | 8% | 19.3% | 19.7% | 21% | 8.3% |

| Dividend Yield | 3.13% | 1.54% | 8.84% | – | 6.36% |

When we carry out the financial analysis, we see how the bank is being impacted by competition. Bradesco has the worst net income margin, the worst net income growth in the last 3 years, and the lowest ROE in the sector.

In my opinion, this discrepancy limits any possibility of recommending buying the shares at this time. But what is the real cause of these numbers?

Perfect Storm

It can be said that Bradesco went through a perfect storm, when a rare combination of events caused a company to lose a lot of value. In this sense, after the massive use of expansionary fiscal policies during the pandemic, what was seen was strong inflation across the world.

In Brazil, it was no different, and the Central Bank here entered a cycle that took the interest rate from 2% to 13.75% until August 2023, when the rate began a new cycle of decline. But what were the immediate effects of this?

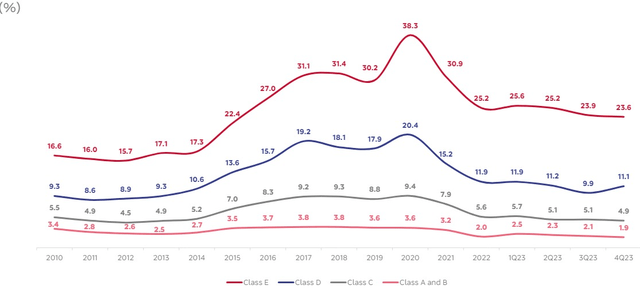

As we said, Bradesco has a strong focus on middle and low-income economic classes, and this class was hit hard by inflation. The effect of this was a brutal increase in delinquency to historic levels and extremely high unemployment rates for the bank’s customers:

Unemployment Rate (IR Company)

In parallel to this, Nu consolidated its presence in Brazil and actually began to threaten the big banks. As I said in my initial coverage report on Nu, the bank has built such a good customer experience and such a strong brand that today more than half of adults in Brazil have an account with the bank.

Furthermore, as colleague and analyst Daniel Urbina cited in his report, Nu has an 83% activity rate. Bradesco does not disclose the number, but considering that it has around 71 million customers and 38.3 million current accounts, the activity rate should be close to 54%, similar to that of Santander Brasil.

Finally, the icing on the cake! In the big event of the request for judicial recovery of the retailer Lojas Americanas, Bradesco was one of the most exposed to the company and suffered a lot amid the negative momentum.

Basically, these were the three reasons for the shares’ performance, and this situation corroborates my thesis of holding the shares, but does the valuation take all of this into account?

Cheap Valuation, But With Justifications

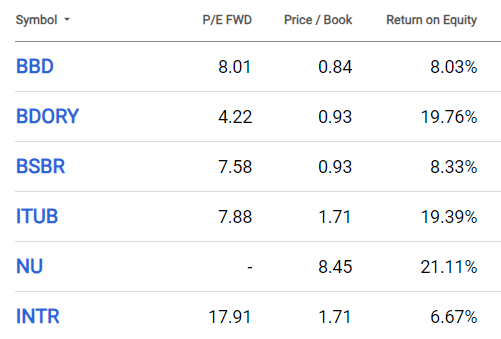

When analyzing the banking sector, which is characterized by stable profits, a good comparison multiple is Price/Earnings in a sectoral comparison. But we will also use P/B in conjunction with ROE.

P/E and P/B (Seeking Alpha)

Well, we can see that the company’s valuation is cheap, however Itau itself has a more attractive P/E, and has better prospects, as I mentioned in my coverage initiation report.

Furthermore, the P/B can be seductive, but if we analyze the ROE, Banco do Brasil is much more attractive, with an ROE of 19.76% and a P/B of 0.93. This comparative analysis supports my thesis about holding the shares. But for the investor, it is important to understand as much data as possible, so let’s analyze Seeking Alpha’s Quant Ranking and Factor Grades.

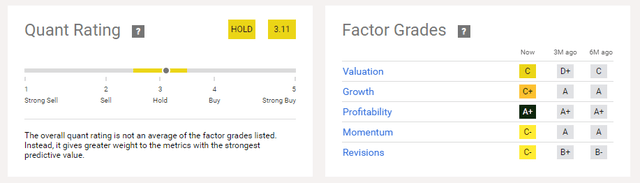

Seeking Alpha Quant Rating and Factor Grades

According to the notes, the only thing that stands out is profitability:

Quant Rating and Factor Grades (Seeking Alpha)

However, all other scores are average, meaning that the Quant tool’s recommendation is also to hold the shares, which makes me very confident in my recommendation. After knowing the current scenario and the market’s pricing for the company, we will understand what Bradesco is doing to recover value.

Restructuring

After weak results and an ROE well below its historical average, Bradesco appointed the new CEO, Marcelo Noronha, to assume the company’s main position. The CEO has been at Bradesco for over 20 years.

The change draws attention and shows a sense of urgency, as CEO changes at Bradesco normally occur on a scheduled basis and by age. Since its founding in 1943, Bradesco has only had five CEOs, and all of them spent 10 years or more in the role.

After his arrival, the new CEO is carrying out an in-depth assessment of people, and recently, four more senior executives were removed from their roles. However, this is still not enough, in my opinion.

As a long-term investor, I would like the bank to have a clear plan for how it will get back to 20% ROE and how soon. The bank does not have this plan, just guidance, unlike Inter & Co, Inc. (INTR) for example, which has its 60-30-30 growth plan, as I describe in my report.

This is why I recommend holding the company’s shares. There is a lack of clear and direct planning for the investor, and again, using the analogy, it takes time for a large transatlantic ship to turn around. Now, we will talk a little about the results that the new management has achieved and the risks next.

Latest Earning Results

Bradesco’s results in the first quarter were, in general terms, within what was expected from the bank at the beginning of its restructuring process.

Forecasts (IR Company)

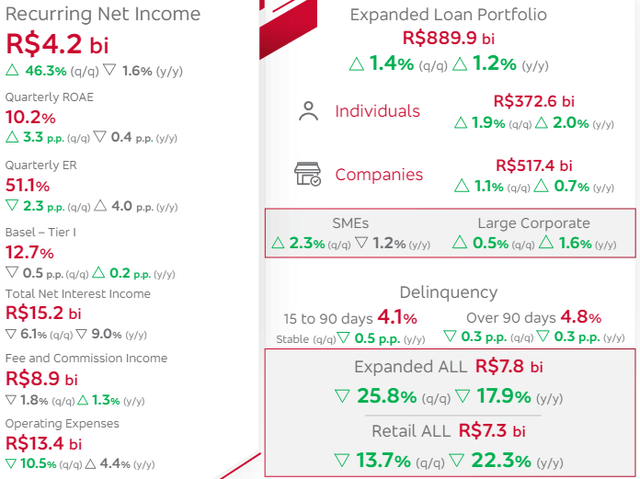

After two quarters of decline, the bank returned to growth in credit, with an expansion of 1.4% in relation to 4Q23 and 1.2% in 1Q23. In the earnings call, the CEO said that first the credit expansion is focused, and then the margin, lending money in higher risk lines. Below are other highlights:

Main Data (IR Company)

In my view, the bank has not yet reached an inflection point, and with the absence of a clearer plan, I see no reason to recommend buying the shares despite the cheap valuation.

Potential Risks to the Bullish Thesis

Well, for investors who follow my recommendation and don’t buy the stock, we have risks that could make the stock rise. I mainly see the macroeconomic risks for Bradesco’s clients and for competitors.

This is because in cycles of interest reduction, as Brazil is going through, it is common for there to be a reduction in delinquency and greater disposable income for families. As a result, Bradesco’s customer profile, low and medium-income families, may be able to consume more of the bank’s services.

Another risk for shares to rise is that the current level of interest makes the operation of fintechs in Brazil extremely complex. We can consider Nu an exception to the rule due to the brand it created, but the situation is quite complex for other fintechs, and Bradesco’s financial strength can help it get through this complex period and stand out in the end.

The Bottom Line

Bradesco was once one of the largest Brazilian banks at a time when there was no competition. However, digital banks have brought a great customer experience, no annual fee on the card, and are growing more and more.

Furthermore, the bank trades at multiples similar to those of Itaú and Banco do Brasil, which in my view has much better prospects of facing the competition. Bradesco is starting to move, it’s true, but the lack of a clear plan makes me skeptical about the robust improvement in results.

Based on this analysis, I recommend holding Bradesco shares. In my opinion, investors should understand that turning around a transatlantic ship, or in this case, a gigantic bank, takes time. In this case, the risk-return ratio does not seem attractive for a buy recommendation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here