When it comes to investing, it’s important to be aware of your weak spots. One of my greatest weaknesses is timing. I can call good investments and I can call bad ones. But sometimes, the timing results in missed upside or unnecessary downside. One example of this can be seen by looking at Bar Harbor Bankshares (NYSE:BHB), a relatively small financial institution with a market capitalization, as of this writing, of $388.1 million.

Back in December of last year, I ended up revisiting the firm. In my initial article about the company in July, I ended up rating it a ‘buy’ because of how cheap shares were and other important metrics. But by December, I was thinking about whether or not it made sense to downgrade the stock. This was based in large part on the fact that shares had already seen upside since my July article of 15% at a time when the S&P 500 inched up only 1.3%. But ultimately, I concluded that it was premature to do so.

Fast-forward to today, and the ‘buy’ rating I kept the company at has not turned out the best. While the S&P 500 has moved up another 7.2%, shares of Bar Harbor Bankshares have seen a downside of 14.8%. To be honest with you, I understand why the company saw this downside. On the other hand, it’s difficult to ignore how high quality the firm’s assets are and how cheap the stock is relative to earnings. At the present moment, even though the stock has fallen, I would make the case that it is still premature to downgrade the company. But given recent financial results, I do think it should be monitored for a potential downgrade.

A difficult time

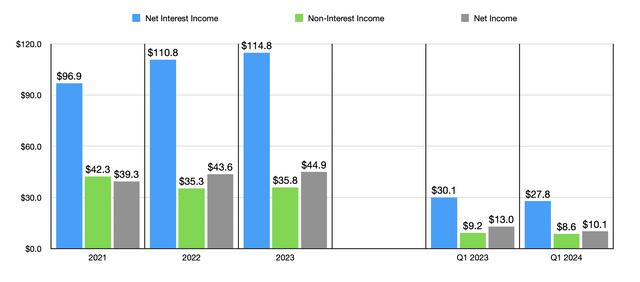

When I last wrote about Bar Harbor Bankshares late last year, we only had data covering through the third quarter of the 2023 fiscal year. Today, that data now extends through the first quarter of 2024. But before we touch on the most recent results, I think it would be important to figure out how the company performed for 2023 in its entirety. In the chart below, you can see net interest income, non-interest income, and net income, for the institution, not only for 2023, but also for the two years prior to that. As the chart shows, there was a slight increase across the board from 2022 to last year. Some of this has undoubtedly been the result of a growing balance sheet.

Author – SEC EDGAR Data

Unfortunately, that trend reversed in the first quarter of this year. Net interest income of $27.8 million came in lower than the $30.1 million reported one year earlier. Part of this, undoubtedly, has been the result of a decline in net interest margin from 3.54% to 3.14%. Although that may not seem like a huge disparity, when applied to the total earning assets of the company during the most recent quarter, it would translate to an extra $14.7 million in net interest income had the net interest margin not declined. Given the current environment, such contraction is not terribly surprising. High interest rates have made it competitive to capture deposits.

Unfortunately, net interest income wasn’t the only weak spot from a revenue and profit perspective. Non-interest income dropped from $9.2 million to $8.6 million. Although there were multiple contributors to this change, the largest by far was a decline in bank owned life insurance income from $1.1 million to only $0.6 million. That was enough when combined with a drop in net interest income and a rise in non-interest expenses of nearly $1 million (mostly from salaries and employee benefits), to bring net profits for the bank down from $13 million to $10.1 million.

Author – SEC EDGAR Data

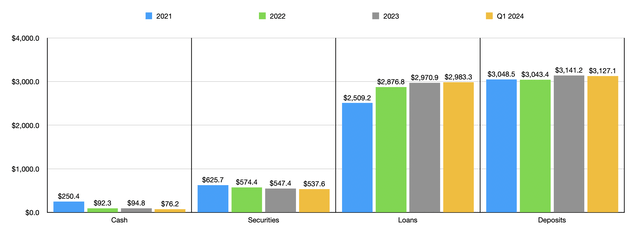

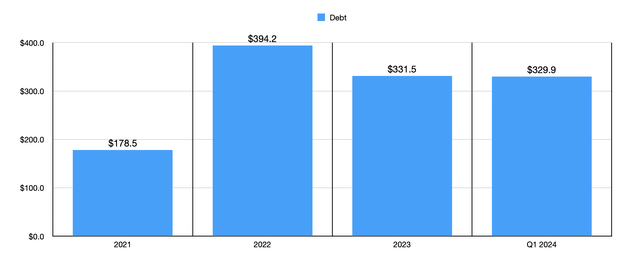

There were some other interesting developments during this window of time. Although deposits grew from $3.04 billion in 2022 to $3.14 billion in 2023, we saw a slight decrease to $3.13 billion in the first quarter of 2024. This is not large enough to cause any significant concern. But I don’t like seeing deposit decreases, and investors should continue to pay attention to this metric to see if a trend begins to develop. Although deposits shrank, the bank did benefit from a rise in loans from $2.97 billion to $2.98 billion. At the same time, however, the value of securities dipped from $547.4 million to $537.6 million, while cash on hand fell from $94.8 million to $76.2 million. At the same time, the institution did see a slight improvement in the amount of debt it has outstanding. This managed to dip down from $331.5 million at the end of 2023 to $329.9 million in the first quarter of this year.

Author – SEC EDGAR Data

These results are, in my opinion, something of a mixed bag. I don’t like seeing deposits decline, and the drop in revenue and profits is discouraging. The decline in cash and securities is also less than ideal, though the overall drops are not significant by any means. The good news is that the value of loans managed to continue its upswing. And the value of debt is falling, although that decline is just by a hair’s breadth.

Author – SEC EDGAR Data

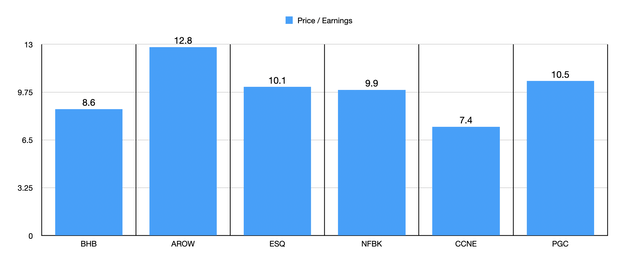

When it comes to valuing the company, there are three different approaches that I like to use. In the chart above, you can see the price to earnings multiple of the institution compared to the price to earnings multiple of five similar firms. On an absolute basis, the 8.6 reading that we get is most certainly attractive. Many of the banks that I have looked at and enjoyed have multiples ranging between 6 and 9. So this is right in my sweet spot. And relative to similar enterprises, shares also look cheap, with only one of the five firms cheaper than it.

Author – SEC EDGAR Data

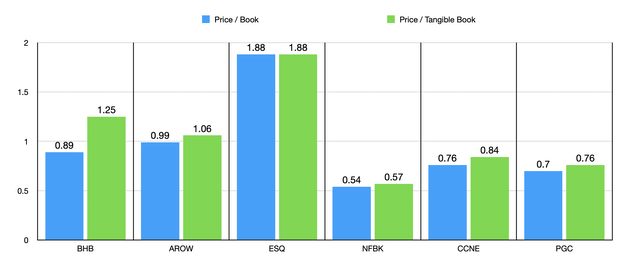

The picture does change, unfortunately, when it comes to the price to book and price to tangible book approaches. In the chart above, you can see what this picture looks like. On an absolute basis, I would actually make the case that Bar Harbor Bankshares appears fairly attractively priced. But it’s not the cheapest of the group. Three of the five companies ended up being cheaper than it on a price to book basis, while four of the five ended up being cheaper when it came to the price to tangible book approach.

Author – SEC EDGAR Data

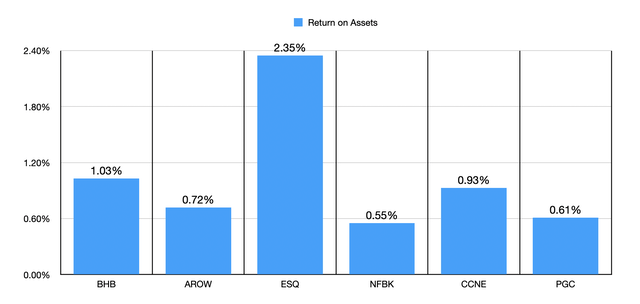

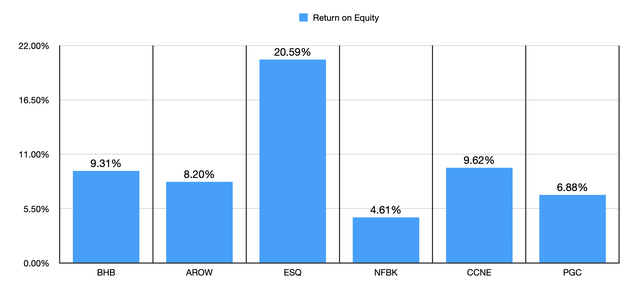

Relative to similar firms, we have a company that looks to be more or less fairly valued. But one area in which it does shine through and can justify trading at a slight premium involves the quality of its assets. In the chart above, you can see the return on assets, not only for Bar Harbor Bankshares, but also for the same five firms I have compared it to throughout this article. It ended up having the highest reading of the bunch. And in the chart below, you can see the return on equity for each of the firms, with only two of the five enterprises having readings that are higher than what Bar Harbor Bankshares currently has.

Author – SEC EDGAR Data

Takeaway

Based on the data provided, I must admit that while Bar Harbor Bankshares is most certainly not my favorite play in the space, it’s far from the worst. It has some positive attributes to it, including growing loan values, a cheap stock price, and relatively high asset quality. On the other hand, there have been some weak spots as well, particularly when it comes to the most recent quarter for which data is available. All combined, I would say that Bar Harbor Bankshares likely does deserve some upside from here. In fact, I would argue that it’s enough upside to warrant a ‘buy’ rating. But on the other hand, it wouldn’t take a great deal much for me to consider a downgrade.

Read the full article here