Battalion Oil (NYSE:BATL) recently reported its Q2 2023 earnings after a delay attributed to its former CFO suddenly leaving the company in early August. Battalion’s recent wells have performed solidly and it should see substantial cost savings once its acid gas injection project is fully ramped up. However, the acid gas injection facility is now expected to be online by the end of 2023, when it had previously been expected to have a significant effect on 2023 costs.

Battalion is hampered by high interest and preferred dividend costs along with hedges that are below strip prices. It also has limited liquidity and is required to make regular payments to pay down its term loan. This has resulted in plans to raise up to another $38 million from issuing preferred equity.

Battalion’s limited liquidity is likely to prevent it from investing much in new development, resulting in production levels that may decline faster than Battalion can reduce the combined amount of its net debt and preferred shares.

As a result, the value of Battalion’s common shares is likely to be eroded by interest costs and the increasing liquidation preference on its preferred shares.

Management Turnover

Kristen McWatters was appointed as Battalion’s CFO in January 2023 after Kevin Andrews decided to leave to pursue other opportunities. After just over six months, McWatters notified Battalion (apparently with limited notice) that she would resign to pursue other opportunities.

CEO Matthew Steele has taken over McWatters’s financial supervisory responsibilities for now, but the sudden change led to Battalion’s Q2 2023 report being delayed.

Steele only became CEO of Battalion in April 2023 after Richard Little resigned. This high level of management turnover is indicative of a company that is in quite a challenging position.

Production Declines

Battalion’s Q2 2023 production ended up averaging 14,253 BOEPD (49% oil). This was down significantly from its average production of 16,200 BOEPD (50% oil) in Q1 2023. Battalion’s total daily production declined by 12% quarter-over-quarter, while its daily oil production declined by 14% quarter-over-quarter.

This significant decline was attributed to natural well declines as Battalion brought online four net wells in Q4 2022 (making Q1 2023 the first full quarter of production from those wells) and one net well in Q1 2023, but no new wells in Q2 2023.

Potential 2H 2023 Outlook

Due to liquidity constraints, Battalion does not appear capable of drilling more wells in the near-term. I have thus modeled its 2H 2023 production at approximately 13,050 BOEPD (48% to 49% oil), assuming that its production continues to decline, albeit at a slower rate of decline than from Q1 2023 to Q2 2023.

At current high-$70s WTI strip, Battalion is projected to generate $111 million in oil and gas revenues before hedges, while its hedges have negative $10 million in estimated value.

If Battalion’s production declines as modeled here, it will have around 96% of its 2H 2023 oil production hedged at $67.36 per barrel, contributing to those hedging losses.

|

Type |

Barrels/Mcf |

$ Per Barrel/Mcf |

$ Million |

|

Oil |

1,166,100 |

$77.00 |

$90 |

|

NGLs |

570,400 |

$20.50 |

$12 |

|

Gas |

3,992,800 |

$2.25 |

$9 |

|

Hedge Value |

$-10 |

||

|

Total |

$101 |

Battalion is thus projected to generate $14 million in free cash flow over the second half of 2023. This assumes minimal capex and that its cash G&A costs are reduced to $5 million in the second half of the year as a result of its April workforce reductions.

I have also assumed that the acid gas injection facility doesn’t meaningfully reduce gathering and other costs during 2023. That facility was previously expected to be “mechanically complete in early April”, reducing gas treating costs significantly during 2023. However, Battalion’s Q2 2023 report now indicates that the facility would be online by the end of 2023.

|

$ Million |

|

|

Lease Operating and Workover |

$26 |

|

Production Taxes |

$7 |

|

Cash G&A |

$5 |

|

Gathering and Other |

$33 |

|

Cash Interest |

$14 |

|

Capital Expenditures |

$2 |

|

Total |

$87 |

Battalion had $19 million in cash on hand at the end of Q2 2023. Battalion’s projected free cash flow in 2H 2023 adds $14 million, but Battalion also has $20 million in term loan payments due in 2H 2023. With the net proceeds from its preferred equity offering, it would end 2023 with approximately $50 million in cash on hand, assuming there are no working capital changes.

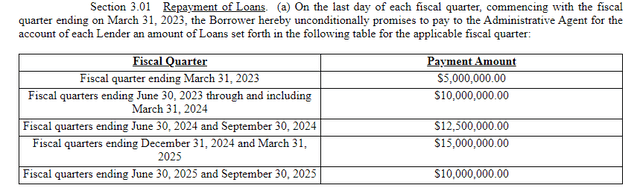

Battalion’s Term Loan Repayments (battalionoil.com)

Battalion’s accounts payable and accrued liabilities exceed its net accounts receivable by $25 million, so there is a decent chance that working capital changes reduce its cash on hand.

Potential 2024 Outlook

Assuming that development capex continues to be minimal, I have modeled Battalion’s 2024 production at approximately 11,400 BOEPD (48% oil).

At the current strip for 2024, Battalion would generate $191 million in oil and gas revenues, while its hedges have negative $22 million in estimated value. In this scenario, Battalion would have 90% of its 2024 oil production hedged at a WTI price of $63.69 per barrel.

|

Type |

Barrels/Mcf |

$ Per Barrel/Mcf |

$ Million |

|

Oil |

2,000,000 |

$75.00 |

$150 |

|

NGLs |

1,000,000 |

$21.00 |

$21 |

|

Gas |

7,000,000 |

$2.90 |

$20 |

|

Hedge Value |

$-22 |

||

|

Total |

$169 |

I’ve assumed that Battalion’s acid gas injection facility is fully operational during 2024, leading to significant savings for its gathering and other expense category.

|

$ Million |

|

|

Lease Operating and Workover |

$50 |

|

Production Taxes |

$13 |

|

Cash G&A |

$10 |

|

Gathering and Other |

$36 |

|

Cash Interest |

$23 |

|

Capital Expenditures |

$5 |

|

Total |

$137 |

Battalion could thus generate $32 million in free cash flow during 2024. As noted before, it was projected to end 2023 with $50 million in cash on hand before working capital changes.

However, Battalion is also required to make $50 million in term loan payments in 2024, so it would then end 2024 with $32 million in cash on hand before any working capital changes.

Debt Situation

At the end of 2024, Battalion is projected to have $32 million in cash on hand (before working capital changes) along with $150 million in remaining term loan debt.

With the 16% PIK interest rate on its preferred shares, the liquidation preference on those share will increase relatively quickly. The liquidation preference on the preferred shares was $26 million at the end of Q2 2023. This is expected to end up at $65 million at the end of Q3 2023 if the agreement for an additional $38 million in preferred shares closes by the end of the quarter.

| Quarter End | Amount ($ Million) |

| Q2 2023 | $26.0 |

| Q3 2023 | $65.0 |

| Q4 2023 | $67.6 |

| Q1 2024 | $70.3 |

| Q2 2024 | $73.2 |

| Q3 2024 | $76.1 |

| Q4 2024 | $79.1 |

The PIK interest would then increase the liquidation preference for its preferred shares to $79.1 million by the end of 2024.

At the end of 2024, there would thus be $143 million in net debt (including the working capital deficit) and $79 million in preferred shares ranking ahead of the common shares.

This combined $222 million total may be around 3.2x Battalion’s EBITDAX at $75 WTI oil and Battalion’s 2024 exit rate production. Without further development, Battalion’s 2024 exit rate production may be around 10,500 BOEPD.

Conclusion

Battalion appears to be largely stuck in a difficult position right now. It is required to make regular payments on its term loan (including $20 million in 2H 2023 and $50 million in 2024). This has resulted in it needing to issue more preferred shares to maintain some liquidity.

These preferred shares have a high PIK interest rate of 16%, which starts eating into the value that is left for the common equity. The acid gas injection facility should help reduce Battalion’s costs once it is fully operational, but it doesn’t appear that Battalion has the financial ability to do additional development.

Battalion is projected to have $222 million in net debt and preferred shares ranking ahead of the common shares at the end of 2024. This compares to $252 million in net debt and preferred shares at the end of Q2 2023.

This is a 12% reduction in net debt and preferred shares, but Battalion’s production is projected to decline by around 24% over the same period. Thus there may be quite limited value left for Battalion’s common shares in the end, while its hedges prevent it from benefiting much (without additional development) from any major rise in commodity prices.

Read the full article here