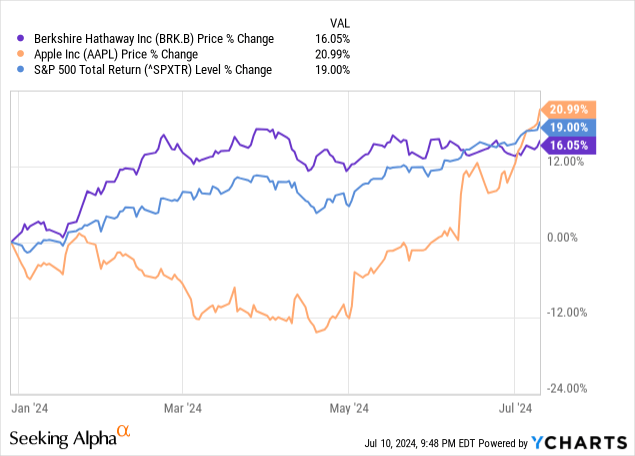

After a hot start to the year, Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) has cooled down and is now trailing the S&P500 for the year, despite a major resurgence in Apple (AAPL).

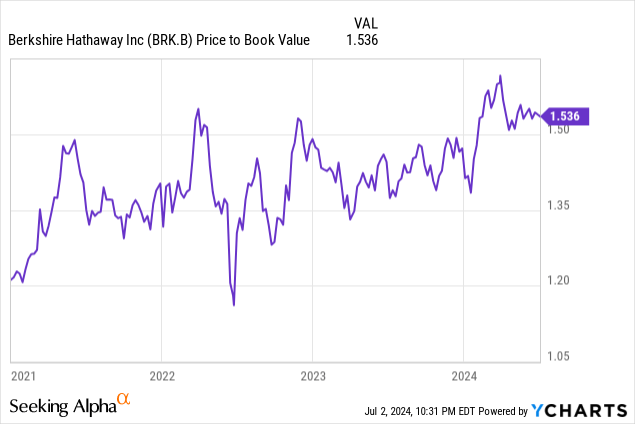

Since I sold around $425, Berkshire has become less expensive, with Price/Book Value nearing 1.4x as of this writing, versus being north of 1.6x where I sold. With indexes increasing 11% since then, the relative value of Berkshire has increased even more. As a result, I’ve repurchased half the shares I previously owned, despite my views on Berkshire’s operating performance (which have not changed.)

Q2 Holdings Update

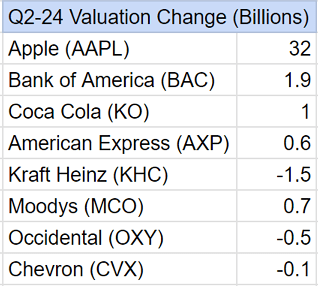

I estimate the value of Berkshire’s investments in equity securities excluding Kraft Heinz (KHC) and Occidental (OXY) rose $37.6 billion, or 11% to $373.3 billion, nearly all on strength from Apple, which rose $170.03 to $216.75 in the quarter.

Berkshire Top Holdings (Author’s Calculations)

From the $37.6 billion gain, after increasing the liability for future income taxes on the balance sheet as “income taxes, principally deferred” by 21%, we see an estimated net book value gain of $29.7 billion for Q2.

I still don’t have a positive view of Berkshire’s portfolio, despite all the wonderful stories we get on Coca-Cola (KO) and American Express (AXP) and other long term holdings. There’s an awful lot of survivorship bias in Berkshire’s anecdotes, as they sell off the losing investments along the way for the tax loss but continue to discuss the winners.

I am happy to see Berkshire starting to sell down its Apple stake, and believe their reasoning is sound, especially at 35x CY earnings. It’s amazing how much sentiment shifted from “AI Loser” to “AI Winner – AI enabled phones will drive next upgrade cycle!” I’m not sure what an AI enabled phone would do, why you’d want to do any AI processing locally in the first place (memory limitations, power consumption), or who is truly interested in it, but narrative drives price in the short term, and I’m glad to see Berkshire taking advantage of it.

Q2 Operating Earnings

Insurance underwriting could show ~$2.25 billion underwriting profit in my view. The insurance industry price hikes have been sticky, but these are bound to normalize soon. Q2 did not feature any significant catastrophe events, and GEICO should remain strong. Q1 was the first quarter in a long time that GEICO noted increased advertising expenses.

Insurance investment income should come in around $2.65 billion, driven by higher short term interest rates and cash balances.

BNSF earnings should come in around $1.1 billion, tracking in-line with last quarter and down significantly from the last 2 years. Intermodal transport is way up year to date, but carloads are off significantly. This quarter looks very similar to last quarter for BNSF so I expect similar results.

BHE should come in around $900 million. I believe the accruals for the 2020 wildfires should be done. Berkshire Hathaway HomeServices is now a major negative for this business, losing $159 million in Q1 of this year (I estimated a $75 million loss this quarter.) In Q1, they noted interest expense was a $102 million headwind over 2023 as the subsidiary debt was refinanced at higher rates (as I mentioned in But All That Cash in a previous article, Berkshire has $123 billion in debt to go along with all that cash you see in the headlines).

Other Controlled Businesses containing dozens of companies like Precision Castparts, Lubrizol, Marmon, and other industrial businesses, including Pilot, I expect to be down year over year. I think the Q1 trends continue here, with Manufacturing up a bit, Service and Retailing down a bit, with most of the shortfall coming from poor results from Pilot.

I’ll estimate $3.3 billion in earnings from this group.

Non Controlled Businesses, defined as business where Berkshire has between a 20% and 50% ownership interest, which represents the interests in Occidental, Kraft-Heinz, and Berkadia. I’ll estimate $700 million in earnings from this group, mostly coming from OXY (high ownership stake, higher crude oil prices in Q2).

Other should show a $500 million gain due a strong US Dollar.

In total, I expect Q2 operating earnings around $11.4 billion, up 14% from last year’s $10 billion, and setting another record for Berkshire.

Current Book Value and “Two Column” Method Valuation

As reported in Berkshire’s 2024 Q1 10-Q, book value as of March 31, 2024 was $571.5 billion.

Adding the $29.7 billion from the equity investments and adding $11.4 billion in operating earnings, I project Q2-24 book value at $612.6 billion.

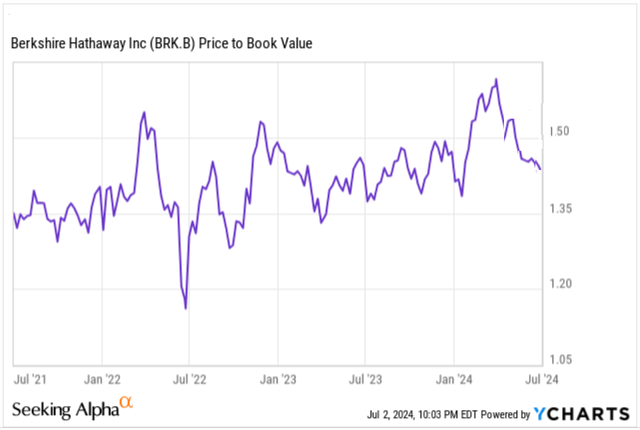

Berkshire Hathaway Price to Book (Q2-21 thru Q1-24 YCharts, Q2-24 Author’s Estimates)

Berkshire’s market cap as of June 30th was $874 billion. Dividing this by $612.6 billion yields a Price/Book Value of 1.43x for Q2.

For the two-column valuation method, over the last four quarters (last three actuals plus my estimates for Q2) Berkshire had $28.6 billion in Operating Earnings after excluding all investment income.

Using my estimates for this quarter, Berkshire has $563 billion in cash and investments excluding equity method investments (as those get counted in earnings.)

If we use a 13x after tax multiple, this implies an Intrinsic Value of $935 billion, not too far above Berkshire’s quarter end market capitalization of $875 billion. One could make an argument that 13x is too conservative, especially in this environment. But I would counter that the insurance businesses currently have unsustainably good underwriting results, and the rest of the businesses have declining earnings over the past two years. I think 13x is about right.

Repurchases

Berkshire has slowed its purchases dramatically in recent quarters.

In 2021, Berkshire repurchased ~$27 billion in shares, including $6.9 billion in Q4. Share count decreased 5.3% over the prior year.

In 2022, Berkshire repurchased $7.9 billion in shares. Share count decreased 2.8% over the prior year.

In 2023, Berkshire repurchased $9.2 billion in shares. Share count decreased 1.4% over the prior year.

In Q1 of this year, $2.6 billion was used to repurchase shares, a pace to repurchase around 1.2% of the float.

I was disappointing that we did not get a question on the slower repurchase level at the Annual Meeting. If Berkshire isn’t in a rush to repurchase shares despite ballooning cash balances, should we?

2nd Half 2024 Outlook and Recommendations – Where do we go from here? Did I make a mistake selling?

I recently repurchased half of the shares I sold at $425 a bit under $405 a few weeks back.

Did I make a mistake by selling in the first place? Perhaps I’ll feel differently in April when I’m writing the IRS a large check, but I believe I made the right decision because Berkshire has underperformed despite many things going right in that timeframe.

- Broader market has advanced 11%.

- Apple has advanced 29%.

- Berkshire had a record quarter of earnings.

Yet, I was still able to repurchase shares 5% below where I sold them, as Berkshire has quickly gone from a Price/Book valuation level it has rarely seen in recent times back towards the upper part of the “normal” recent range.

Several things have pushed me back in the shares lately, despite my dim view of many of Berkshire’s operating businesses.

- Berkshire starting to monetize its Apple holdings. I think selling Apple up here materially de-risks the shares. I think we’ll see further sales over the rest of the year if Apple shares remain this high.

- By year end, with continued earnings, shares could be back near the 1.35x book level where Berkshire was a large buyer of its own shares in 2021.

- With more cash from selling down Apple coupled with lower short term interest rates in 2025, Berkshire could shift back to a higher level of repurchases.

- I believe the acquisition spree of the last 15 years, which yielded such poor results, is over. I think Pilot was the last straw with this failed strategy. Almost entirely absent from this year’s annual meeting were discussions of elephant guns and things like that. Running a massive conglomerate is hard, and I hope Berkshire has learned from this.

- The Fed’s latest dot plot has short term interest rates declining to ~4% by next year and to ~3% the year after. Despite its mixed history in actually predicting what happens, I do think short term rates decline from here. That makes Berkshire more attractive than cash for me.

I still believe Berkshire’s 2024 operating earnings will be the high watermark for a long time, perhaps until the end of the decade, as I believe lower short term interest rates and normalizing insurance underwriting results could create a $5+ billion headwind by year-end 2025. But with the relative valuation improvement and cash build, share repurchases could become a major driver again, like they were in 2021. I think Berkshire is a reasonable buy versus the S&P500 or treasuries at these levels.

Read the full article here