Prominent Billionaires such as Jamie Dimon of JPMorgan (JPM) and Warren Buffett of Berkshire Hathaway (BRK.A)(BRK.B) have recently signaled that the market is overvalued and may be due for a sharp correction. In this article, we will explore the details of their recent actions that indicate this, take a look at leading market valuation models, and then share our approach to investing in the current environment.

Why Jamie Dimon and Warren Buffett Seem To Think That Markets Are Overvalued

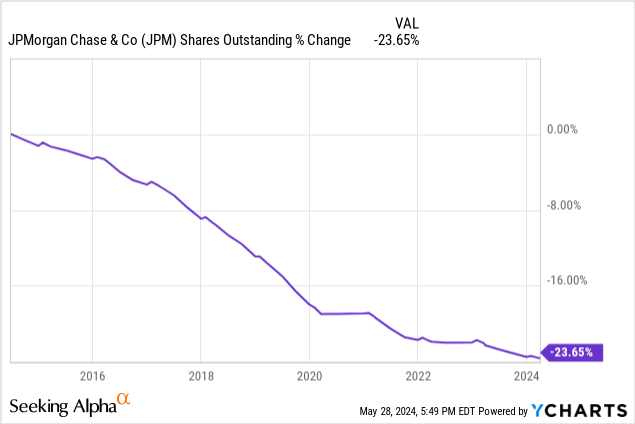

Jamie Dimon, who typically has his company buy back significant amounts of JPMorgan stock and has, in fact, reduced the shares outstanding by nearly 1/4 over the past decade, recently stated that

we’re not going to buy back a lot of stock at these prices. We’ve been very, very consistent. When the stock goes up, we’ll buy less, and when it comes down, we will buy more.

Putting two and two together, it appears that Jamie Dimon thinks that his stock is overvalued. Additionally, Mr. Dimon has said that he is cautiously pessimistic about the outlook for markets and the economy, given the rising geopolitical tensions and risks as well as inflation remaining quite sticky. In fact, he has previously said that he would not be surprised if interest rates soar into the high single digits, which would likely pose enormous problems for both the economy and the United States fiscal situation.

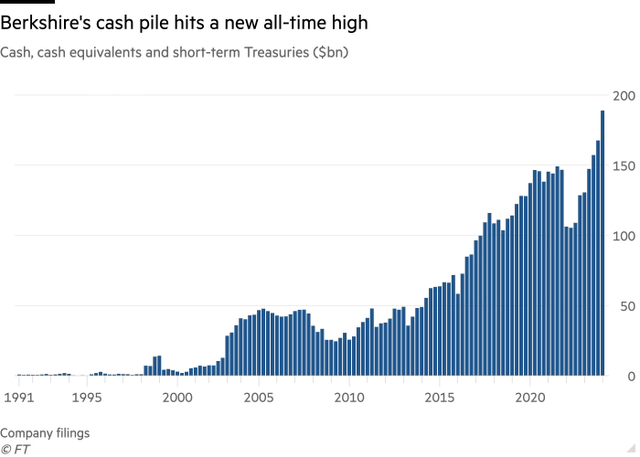

Meanwhile, Warren Buffett is also signaling that the market may be overvalued by allowing Berkshire’s cash stockpile to reach a record high of $189 billion, and is rapidly closing in on $200 billion. The reason he has given for letting the cash pile grow so large is that there is a lack of attractive alternative investments for him that would move the needle for Berkshire Hathaway, which apparently also includes his own stock. When compared against the nearly 5.5% yield that can be earned on holding cash in short-term treasury bills, it makes sense why Warren Buffett is letting his cash pile get so big.

Berkshire’s Cash Pile (Financial Times)

What Market Valuation Models Are Signaling

When looking at current market valuation models, we can see why these leading billionaire CEOs are growing increasingly cautious on the markets and are refraining from allocating their capital towards buying stock, even if it’s their own. For example, the Buffett Indicator model is currently at 197%, which is about two standard deviations above the historical trend line. This implies that the stock market is strongly overvalued. The price-to-earnings ratio model is currently 1.7 standard deviations above the modern-era average and is 68.7% above the modern-era market average of 20.3 on a 10-year PE basis of the S&P 500 (SPY). This implies that the market is overvalued. The interest rate model also implies that the US market is overvalued relative to a normal interest rate environment, as it sits at 1.8 standard deviations above the trend line. Finally, the mean reversion model sits at 1.8 standard deviations above the modern-era historical trend value, indicating that the market is also overvalued as the S&P 500 is currently trading at a 62% premium to the long-term trend line.

Not only that, but there are also growing indicators that recession risk is on the rise. In addition to numerous foreign countries, including major trading partners like Japan and the United Kingdom, being in a recession, China is facing economic challenges of its own. Meanwhile, the yield curve model implies that there’s a very high risk of recession, and the unemployment rate in the United States is also on the rise, rapidly approaching 4% even as excess consumer savings from the COVID-19 stimulus have been completely wiped out and consumer debt is sitting at record levels. All this seems to signal that the markets are more than due for a pullback, and therefore Buffett’s and Dimon’s caution seems quite warranted.

Our Investing Approach In The Current Environment

While some may think that this all means that we should go completely to cash and run for the hills, we also believe that market timing is a fool’s errand. As Warren Buffett himself once said,

We haven’t the faintest idea what the stock market is going to do when it opens on Monday. We never have. I don’t think we’ve ever made the decision where either one of us has either said or been thinking we should buy or sell based on what the market is going to do, or for that matter, what the economy is going to do.

Instead of investing purely off of where the market currently stands, we like to invest in businesses that we think trade at a clear discount to their intrinsic value and have the quality of both their business model and their balance sheet to be able to survive a recession or any other kind of economic disruption with an eye towards achieving outsized long-term total returns. That being said, when the market is frothy like it currently is, we are much less likely to find attractive opportunities among the big and popular companies and instead get much more creative in where we search for opportunities.

Moreover, when we find opportunities that are a little bit less correlated to the broader market, we tend to put a greater weighting on those in our portfolio in order to position our portfolio such that if the market does experience a sharp pullback or a long-term period of underperformance, we should have sufficient resources allocated in other places that we can still generate decent returns in the short term and have some capital on hand to be able to recycle opportunistically if and when more mainstream stocks begin to trade at compelling bargains.

For example, during the recent pullback in market-making stock Virtu Financial (VIRT) earlier this year, we doubled down on our investment and since then, have been rewarded with very attractive returns. However, given that the stock profits off of volatility, should the market crash, we expect it to shoot even higher. Since it is one of our very largest positions at the moment, we would be very easily able to sell some of our shares at a sharp profit and recycle the capital into undervalued more traditional dividend growth stocks. Additionally, we loaded up on yield-focused precious metals investments last fall in anticipation of a gold (GLD) and silver (SLV) bull market, which has certainly manifested so far in 2024. Finally, we are also finding significant opportunities still in infrastructure businesses, such as a recently very profitable investment in Brookfield Renewable Partners (BEP)(BEPC) and very profitable longer-term positions that have generated attractive returns in the midstream space, such as Energy Transfer (ET) (which we recently sold) and Enterprise Products Partners (EPD).

Investor Takeaway

While billionaires like Jamie Dimon and Warren Buffett are becoming increasingly cautious and are amassing cash on their companies’ balance sheets, and the markets are signaling that their valuations are quite stretched even as geopolitical and macroeconomic signals imply that risks are rising, we are not running for the hills. That being said, we are being increasingly selective, focusing on more niche and non-correlated areas of the market to position us to generate attractive returns and potentially be able to capitalize on a sharp correction in the major indexes moving forward. While we wait, we collect a very attractive mid to high single-digit dividend yield as well.

Read the full article here