Blackrock (NYSE:BLK) delivered a strong Q1 2024 performance, beating analyst consensus estimate on both topline and earnings. During the first quarter, Blackrock’s revenues, operating earnings, and assets under management increased by 11%, 18%, and 15% YoY. Reflecting on strong Q1 results, paired with confident management commentary on the FY 2024 outlook, I see Blackrock poised for significant earnings upside, buoyed by the resurgence of a bull market across equities, cryptocurrencies, and various tradable asset classes, which is expected to drive higher asset under management levels and increase the company’s capital base for fee generation. On valuation, I see upside too: Considering a residual earnings valuation framework, I calculate that Blackrock shares may be about 15% undervalued.

For context: Blackrock stock has grossly underperformed the broader U.S. stock market YTD. Since the start of the year, BLK shares are down about 6%, compared to a gain of approximately 7% for the S&P 500 (SP500).

Seeking Alpha

Strong Q1 Results Beat Estimates …

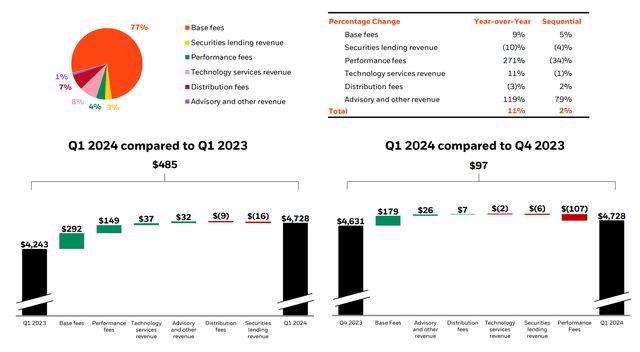

Blackrock delivered a strong set of Q1 2024 results, topping analyst consensus estimates with regard to both topline and earnings: During the period from January through end of March 2024, the world’s largest investment company by AUM saw a 11% YoY growth in revenues, bringing the total topline to $4.73 billion (vs. about $4.71 billion estimated by consensus, according to data collected by Refinitv). In that context, I point out that Blackrock’s growth has been driven mostly by higher base fee income, which I view as a high-quality, recurring revenue stream similar to the ARR metric seen in software businesses: In Q1 2024, Blackrock’s fee income jumped by 9% YoY and 5% QoQ. Overall, fee income accounts for about 77% of Blackrock’s total revenue

BLK Q1 2024 Results

On profitability, I highlight that Blackrock’s operating margin in Q1 2024 expanded by about 190 basis points compared to the same period one year earlier, bringing the operating margin to 36%, and operating income to about $1.7 billion. Notably, Blackrock’s profit growth, at 15% YoY, outpaced the company’s topline growth, and reflects a sustainable efficiency improvement on the backdrop of investments in technology. In that context, Blackrock’s CEO Larry Fink highlighted:

So people do more, and the whole organization is doing more with less people. That is really our ambition […] As we continue to be investing in AI, our most recent experience of having $2.5 trillion more assets with the same headcount is a real good indication of how we are trying to drive more efficiencies, more productivity

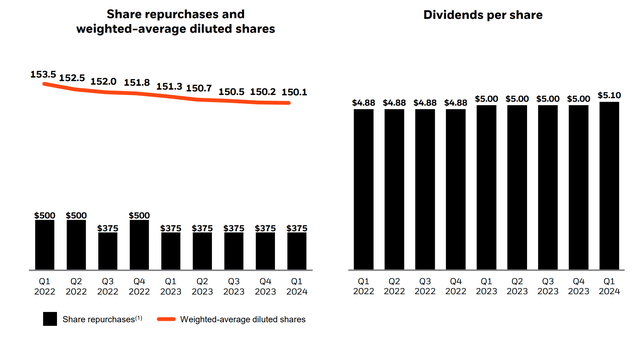

Blackrock’s net income surged 36% YoY, to approximately $1.6 billion. For context, Analysts had expected net income of about $1.35 billion (~10% beat), according to data compiled by Refintiv. While about 30% of income is retained for growth/ re-investment opportunities, investors will appreciate that about 70% is distributed to investors, suggesting a close to 4% equity yield: In Q1, Blackrock paid about $750 million in the form of dividends. Moreover, in Q1 2024 Blackrock repurchased $375 million worth of common shares; and management reiterated its previously set commitment to “repurchasing at least $375 million of shares per quarter for the balance of the year”.

BLK Q1 2024 Results

… And Support A 2024 Bull Thesis

Looking to the remaining quarters of 2024, I am confident to project that Blackrock’s commercial momentum is set to strengthen even further. In fact, expecting that markets remain bullish, I project that Blackrock’s assets under management are poised to continue growing at a 10-15% YoY rate, extrapolating recent Q1 results, driven by both equity appreciation on clients’ invested assets, as well as new inflows. On that note, I highlight that in Q1, Blackrock’s assets jumped by about $500 billion, to a record $10.5 trillion in AUM, up $1.4 trillion YoY.

Looking ahead, I am also bullish on the potential for AUM growth on the backdrop of anticipated rate cuts that could start as early as June. In my view, lower rates should prompt a move of capital that currently on the sidelines into riskier, and longer-duration assets such as equities and equity-linked notes. If the thesis of asset re-balancing towards risk assets holds true, then I see BlackRock positioned to capture a disproportionately large share of the capital flows, as evidenced by the company’s track-record to outperform peers on AUM expansion.

In line with Blackrock’s business model, the higher AUM balance will undoubtedly support healthy fee income expansion. Moreover, in bullish markets, many of BlackRock’s investments are likely to deliver strong results for clients, potentially triggering performance-based fees. Notably, in Blackrock revealed that in Q1 2024 performance fees surged by 271% YoY, accounting for approximately 4% of total revenue.

Valuation: Set TP AT $880/ Share

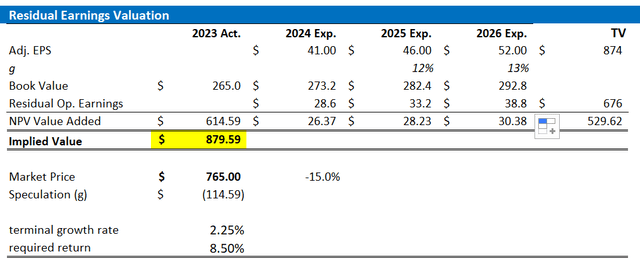

In my opinion, companies with steady and relatively predictable business fundamentals like Blackrock are quite easily and precisely valued with a residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my Blackrock stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal till 2026.

- To estimate the capital charge, I anchor on BLK’s cost of equity at 8.5%, which is approximately in line with the CAPM framework.

- For the terminal growth rate after 2026, I apply 2.25%, which is about in line with estimated nominal global GDP growth.

Given these assumptions, I calculate that the base-case target price for BLK stock is about $880 per share.

Analyst Consensus; Company Financials; Author’s Calculations

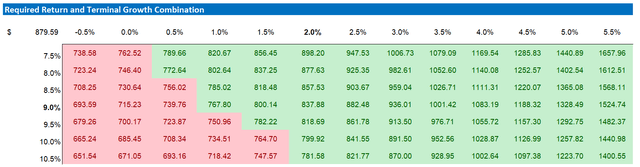

As I argued that my estimates for growth and equity charges may be conservative, I acknowledge that investors may hold varying assumptions regarding these rates. Therefore, I’ve included a sensitivity table to test different scenarios and assumptions. See below.

Analyst Consensus; Company Financials; Author’s Calculations

A Note On Risks

Overall, I view Blackrock as the leading asset manager in the world. And given the company’s strong commercial momentum with both retail as well as institutional investors, I am not really concerned about competitive risks. That said, in my opinion, the major potential downside in Blackrock’s growth and earnings narrative relates to macro factors. Specifically, I highlight that the bull thesis for Blackrock stock builds a continuation of the ongoing bull market. If the valuation levels of assets (mostly equities, fixed income) would see a major correction in the forecasted time period, then the demand for Blackrock’s services and products would likely fall, and AUM inflows would likely slow.

Investor Takeaway

BlackRock outperformed estimates in Q1 2024, surpassing consensus projections for both revenue and earnings. Notably, the world’s leading investment franchise saw its revenues, operating earnings, and assets under management grow by 11%, 18%, and 15% YoY, respectively. Buoyed by these robust results and positive management outlook for FY 2024, BlackRock is well-positioned for significant earnings growth, in my opinion. This optimism is fueled by a revitalized bull market in equities, cryptocurrencies, and other tradable assets, which is expected to boost asset management levels and enhance fee-based revenue. All things considered, I see a compelling entry point for this high-quality asset management franchise, currently trading at a 15x projected 2025 P/E ratio, according to data collected by Refinitv. Anchored on a residual earnings framework, my calculation calls for a fair implied target price of $880/ share, suggesting approximately 15% upside to fundamentals. “Buy”.

Read the full article here