In March this year, I issued an article about BlackRock TCP Capital Corp (NASDAQ:TCPC) downgrading the BDC from buy to hold due to suboptimal Q4 results and the signs of negative fundamental momentum going forward.

More specifically, the key reasons behind the downgrade were the following:

- Increasing leverage.

- Declining adjusted NII results.

- Depressed net investment funding flows.

At the same time, I did not make a case for a short (or sell) move since the dividend coverage level still remained solid at 129% even after factoring in the most recent NII figure. Plus, and this is more general argument, the current environment, where we see a strengthening of higher for longer scenario in conjunction with decently performing economy makes it very risky to go against any BDC out there.

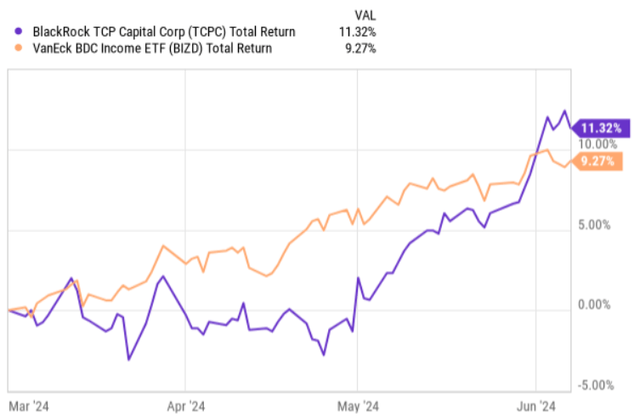

Since the publication of my article, TCPC has slightly outperformed the BDC index even though until the issuance of Q1, 2024 earnings results, the Stock was clearly lagging behind the index (and even finding itself in a negative return territory).

YCharts

Right after the Q1, 2024 earning release, TCPC really surged higher. With that being said, we have to also be cognizant of the fact that the recent macroeconomic data points have been suggesting that the interest rates will remain higher for longer, which has, in turn, introduced notable tailwinds that benefit the most leveraged and high beta BDCs.

Let’s now review the recent financial results of TCPC and see whether this share price run-up is justified or not.

Thesis review

The Q1, 2024 performance could be deemed decent with no major negative surprises either to the downside or upside.

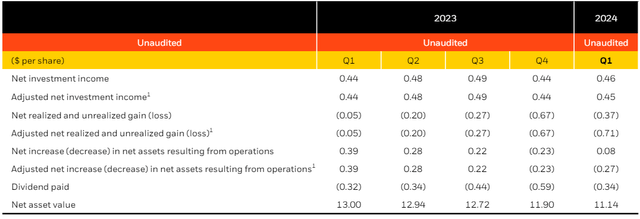

For the first quarter of 2024, TCPC registered adjusted net income of $0.45 per share – i.e., an increase from $0.44 per share in the prior quarter, but still below the previously achieved highs in Q2 and Q3 of 2023.

Yet, from the NAV perspective, the picture is not that stable as during Q1, 2024 the total NAV dropped by 6.4% mostly due to net unrealized losses on two (with a relatively significant size) portfolio companies. These markdowns were high enough to offset the surplus cash retention from adjusted NII after dividend distributions.

BlackRock TCP Capital Q1, 2024 earnings results

In this context, Raj Vig – Chairman and CEO – commented during the recent earnings call that these write-downs were not an indicative of the overall portfolio quality, which continues to remain robust:

The write-downs in the first quarter are mostly the result of circumstances specific to a handful of companies, and as we have stated before, we do not believe these situations are any indication of broader credit challenges in our portfolio. The majority of our portfolio companies continue to report revenue and margin expansion, with many generating sustained performance improvements.

Also, if we look at the non-accrual front, we will notice that the actual data are quite solid with only five portfolio companies put under non-accrual, representing 1.7% of the portfolio at fair value, which could be considered below sector average.

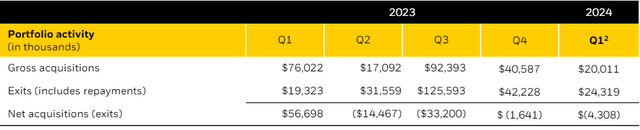

Another relatively suboptimal dynamic was registered at the portfolio activity front, where the gross acquisitions continued to drop, disabling TCPC from growing the portfolio size as the exits still came in at higher volumes than the new fundings for a fourth quarter in a row.

BlackRock TCP Capital Q1, 2024 earnings results

Here, however, it is worth underscoring that these new fundings at ~$20 million were underwritten at quite attractive yields. For example, currently, the overall effective yield of TCPC’s debt portfolio is 14.1%. The investments in new companies during the Q1 had a weighted average effective yield of 14.7%, which is roughly 70 basis points above the total portfolio yield.

From this, we can conclude that TCPC remains rather selective on the new investments by keeping the margins and credit quality optimal. On the latter component, Phill Tseng – President – gave a nice color during the earnings conference cell:

In reviewing new opportunities, we emphasize transactions where we are positioned as a lender of influence, where we have a direct relationship with the borrower and the ability to leverage our more than two decades of experience in negotiating yield terms and conditions that we believe provide meaningful downside protection. We believe this has been a key driver of our low realized loss rates over our history.

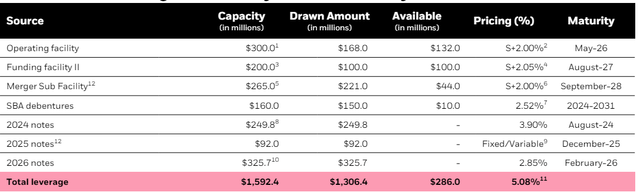

Finally, because the new funding volumes have come in negative for four quarters in a row, the leverage profile has decreased accordingly. The current net debt to equity of TCPC stands at 1.08x, which is in line with the overall sector average levels.

However, the debt maturity profile embodies some risks, which are heavily dependent on how the interest rate curve will evolve. Namely, if we look at the table below, we will see that there is roughly $660 million of borrowings (or a bit less than half of the total drawn amount) that is based on below market level fixed rate financing. About $250 million of this is set to mature in 2024, which will immediately expand the interest expense component for TCPC as the cost of financing converges to a market-level rate after the refinancing / debt rollover event.

BlackRock TCP Capital Q1, 2024 earnings results

After this, the next event of notable fixed rate debt refinancing is set to take place in early 2026, which, if interest rates remain unchanged or close to the prevailing levels, should introduce additional headwinds for TCPC adjusted NII generation.

The bottom line

In a nutshell, TCPC exhibits some positive and some negative dynamics, which together render the investment case suboptimal.

On the one hand, the dividend coverage is solid at 132% leaving ample amounts of cash at the books that could be directed towards incremental fundings or debt optimization. On the other hand, the net funding volumes continue to remain negative, which in combination of forthcoming fixed rate debt rollovers should impose additional headwinds for TCPC to generate growth in the adjusted NII segment.

Given the aforementioned elements and the fact that TCPC trades at P/NAV of 0.99x (effectively in line with the underlying NAV), in my opinion, there are more attractive BDC picks out there.

Read the full article here