Life happens fast in the stock market. In our coverage of Blackstone Mortgage Trust, Inc. (NYSE:BXMT) in June, we highlighted the risks that were front and center and suggested investors stick with the bonds rather than chase high-yield.

Of course, the reason you have made far less money than even this 7% a year is that the stock trades at a wide discount to NAV versus what it did at inception. But regardless of that observation, we think the 8% yield to maturity bonds should outperform the common, despite the latter yielding almost 14%.

Source: 8% On Bonds Beats 14% On The Stock.

While we did not pen a separate piece on BXMT until today, we did downgrade the company to a “Sell” when we wrote about Apollo Commercial Real Estate Finance, Inc. (ARI).

That said, we think at this level of leverage, ARI is about as dangerous as it can get. We rate the firm a Sell. We are also moving BXMT to a Sell, which has rallied 13% since our last article.

Source: Comparing 13% Yielder Vs. Peers.

That was four days back. We look at the results announced today, the distribution cut which was thrown in as the icing and tell you why it is not too late to run for the exits.

Blackstone Mortgage Trust Q2 2024 Results

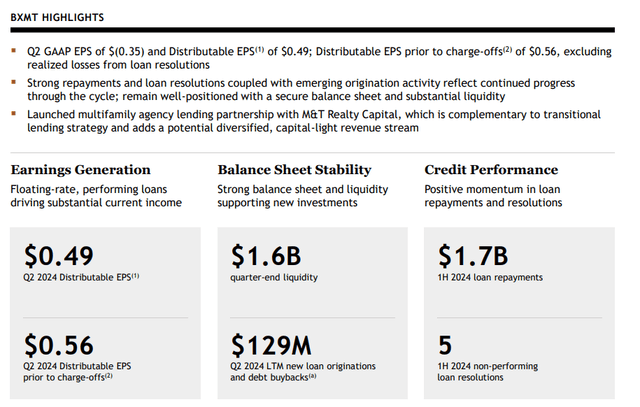

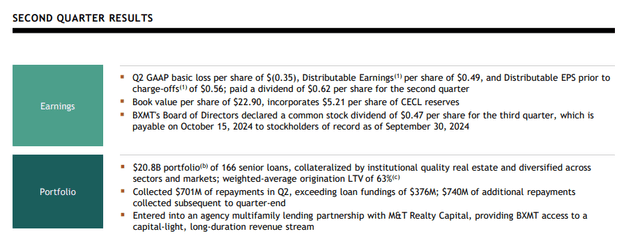

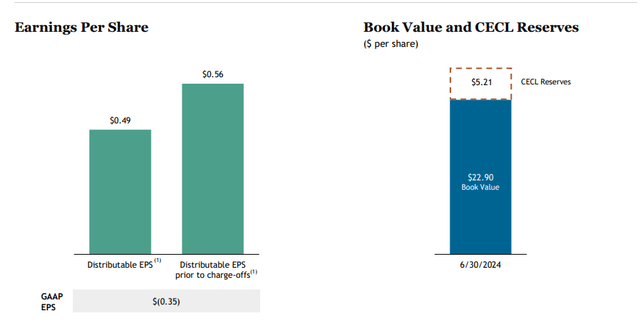

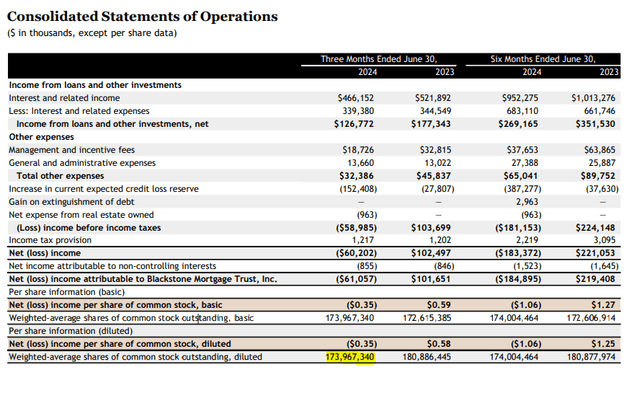

If you are an income investor, you likely focused on the distributable EPS when you saw the press release. That number came in at 49 cents a share. Even that was comfortably below the prior distribution of 62 cents. So there was no real surprise that the distribution was cut. But it does get far worse than that. GAAP EPS was negative 35 cents, and there were another round of CECL adds and charge-offs for investors to contend with.

BXMT Q2-2024 Presentation

Sure, if you work hard at it, you can ignore those GAAP numbers. But the reason you did not see this distribution cut coming is precisely because you ignored the message. BXMT was reporting quarter after quarter of poor numbers, and investors hit the snooze button. However, where we are today is very relevant. The company’s distributable EPS barely covers the new distribution as well. The interest income has peaked as all the floating rate loans have the rate hikes in the rearview mirror. We are likely to see at least 1 Fed rate cut soon. So there are more problems to be had.

Outlook

From our perspective, there are several reasons not to invest in BXMT, and the poorly covered distribution is just one. For starters, we don’t see the loan to value ratios providing an adequate buffer today. The slide below shows the 63% loan to value, and investors might think that offers some kind of stability. It does not. The reason is the tiny “C” next to that value.

BXMT Q2-2024 Presentation

The footnote attached to that “C” says the following.

Reflects weighted average loan-to-value (“LTV”) as of the date investments were originated or acquired by BXMT excluding any loans that are impaired and any junior participations sold.

That loan to value is as of the date when BXMT originated (or acquired, most likely originated) the loan. Values are down 40%-60% in the office sector, and we think the bulk of its US office portfolio is already underwater using realistic marks. Some of it has been taken into account in its CECL numbers. The company has $5.21 of CECL reserves, which are excluded from tangible book value per share.

BXMT Q2-2024 Presentation

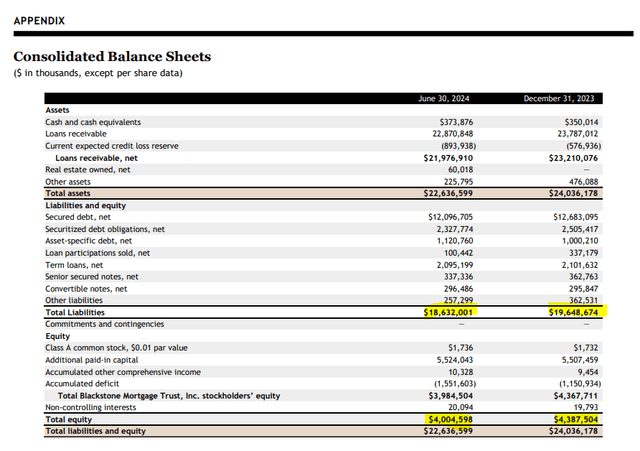

But in the grand scheme of things, this $5.21 is minor. You can get a sense of the risks here by just poring over the balance sheet. The company’s liabilities are over 4.5X the total equity. The $18.6 billion of liabilities is truly daunting, and this is despite the $1.0 billion of reduction over the past 12 months.

BXMT Q2-2024 Presentation

You can notice in the picture above that the equity has dropped at a faster pace than the liabilities in the past 6 months. So that metric is actually slightly higher today than it was on December 31, 2023. The CECL reserves per share total up to around $906 million when you consider the shares outstanding.

BXMT Q2-2024 Presentation

That is way too little considering the leverage metrics here. The US office alone has loans of $5.3 billion. Of course, that will not be going to zero, but that exposure exceeds the total equity.

BXMT Q2-2024 Presentation

We would assume the bulk of the risk level 4s and 5s would experience significant losses in a recession. We think this would also be the case for the non-office portfolio. The current market is already in trouble, and a recession and widening credit spreads would tip it over. So while we believe BXMT will be around for a long time, we don’t see the long case for it, even after the 9% haircut today.

Verdict

Realistically speaking, BXMT should be running the same leverage metrics as Ares Commercial Real Estate Corporation (ACRE). We are talking about a sub 2.0X number for debt to equity. How do we reach there is the question. We would think that the minimum amount of further equity impairment we will see is another $1.0 billion over the next 12–24 months. This is after the CECL losses marked. On the remaining $3.0 billion of equity if BXMT runs a 2.0X leverage, it will have assets of around $9.0 billion versus the $22 billion today.

Keep in mind that it is generating 49 cents of distributable EPS on $22 billion. So whip out your calculators and estimate the run-rate for $9.0 billion. Spoiler alert: It is less than 25 cents.

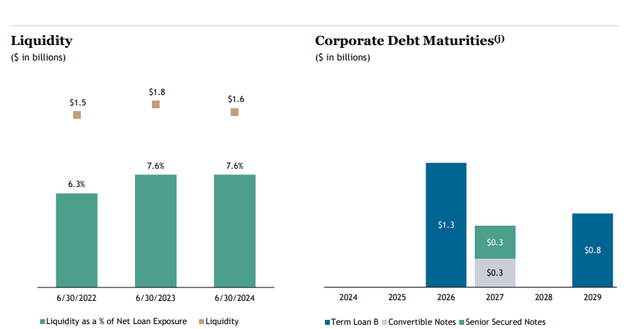

To add some extra color to this, consider the liquidity situation. There is a lot of refinancing ahead for BXMT, and a lot of that is currently at low interest rates.

BXMT Q2-2024 Presentation

The final brush strokes come from what BXMT has committed to fund for future projects.

BXMT Q2-2024 Presentation

All in, this is going to be a fairly long slog to make money. We continue to rate Blackstone Mortgage Trust, Inc. as a Sell and would get constructive under $12.00 per share.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.