Thesis

I am positive on Blade Air Mobility, Inc.’s (NASDAQ:BLDE) advantageous position as a first mover in the Urban Air Mobility (UAM) industry. Blade is experiencing robust growth momentum, which is expected to accelerate as brand awareness increases and more people utilize its innovative on-demand and scheduled helicopter services. Blade’s asset-light approach allows for flexibility in adapting to different use cases. The company is focused on achieving profitability by expanding its customer base, developing infrastructure, and forming global partnerships with operators. Blade’s established brand, software platform, and infrastructure provide a competitive advantage that could pose a risk to new entrants. I am positive on the stock and have an end-of-year price target of $6.5 is derived by using a forward EV/ Revenue multiple of 1.5x applied to the 2024 revenue estimate of $270 million.

Company Description

Blade is a technology-enabled air mobility platform. The company offers a price-competitive and time-efficient alternative to ground-based transportation in congested routes primarily in the Northeast US, with plans to expand to the West Coast and other locations over time. Catering mainly to business or affluent travelers currently, Blade operates exclusive passenger terminals in key markets, and offers by-the-seat service between city centers and airports using helicopters and seaplanes provided by third-party operators. The firm’s technology platform includes a mobile application that enables Blade to aggregate customer demand and optimize passenger volumes in the firm’s network. Blade looks to incorporate EVAs (eVTOLs) into the fleet in 2025, expanding the network into additional locations owing to the low-noise, zero-carbon characteristics of these vehicles.

Q1 Review & Outlook

Blade’s revenue for the first quarter of 2023 exceeded market expectations due to strong growth in its organ transplant business, MediMobility. This performance aligns with previous quarters where Blade consistently surpassed estimates. The Short Distance business of Blade also benefited from the inclusion of Blade Europe, a recovery in the Canadian market, and growth in the Airport business through a gradual increase. Blade’s MediMobility division achieved a new hospital contract, with some benefits expected to carry over to the second quarter, along with increased flight time with existing hospitals. Looking ahead, I view Blade’s MediMobility business as a significant growth driver and an undervalued asset as the volume of organ transplants continues to rise and the customer base expands. The recent acquisitions of European companies by Blade will have a notable impact this year, contributing to revenue for the entire year and improving cost management.

Blade has a competitive advantage over its peers in terms of fleet diversity, including different types of aircraft and a wider geographic reach after acquiring Trinity. This advantage allows Blade to ensure timely and accessible organ transport as needed. As a result, Blade has experienced significant triple-digit growth in this sector and currently holds an estimated high 20% market share for heart, liver, and lung transportation, with potential expansion into kidney transportation. Additionally, the industry itself is expected to experience substantial growth due to advancements in perfusion technology, enabling longer flights with larger aircraft and driving further revenue growth.

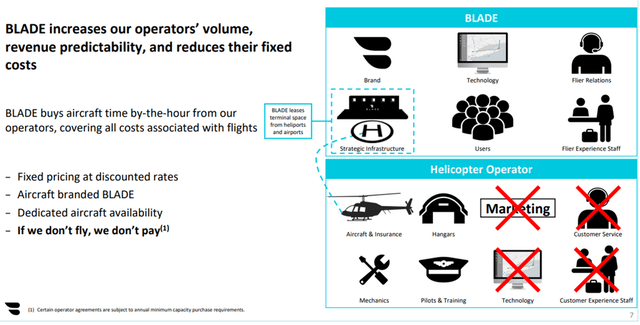

Flexible Business Model

Blade follows a capital-efficient and flexible business model that is adaptable to various use cases. While the company believes in the future potential of electric vertical takeoff and landing eVTOL aircraft, its current focus is on achieving profitability by expanding its passenger and customer base, developing essential infrastructure, enhancing user experience, and establishing global partnerships with operators. Under Blade’s contracts, operators are responsible for insurance, pilots, and fuel costs, while they can reduce fixed expenses like customer service by partnering with Blade. This partnership allows operators to increase flight time and distribute costs over more hours. Furthermore, Blade is confident in maintaining its competitive advantage even after eVTOL introduction, thanks to its established brand, robust software platform, and existing infrastructure, which often take years to build. This could pose an underestimated risk for new entrants in the market.

Company Presentation

Offering a Strong Value Proposition

Ground-based traffic congestion is a widespread issue in densely populated urban areas across the world. Blade currently offers a competitive short-distance aviation service using helicopters and seaplanes, which is priced similarly to private ground transportation options like Uber-X. This service significantly reduces travel time for commuters traveling to and from airports as well as city centers. It can be implemented with moderate investment in infrastructure. Moreover, the concept of air taxi services has gained overwhelmingly positive public sentiment. In 2025, Blade plans to expand its service by introducing Electric Vertical Aircrafts (EVAs), which are low-noise and low-carbon air vehicles. This addition will enable Blade to operate in even more convenient locations.

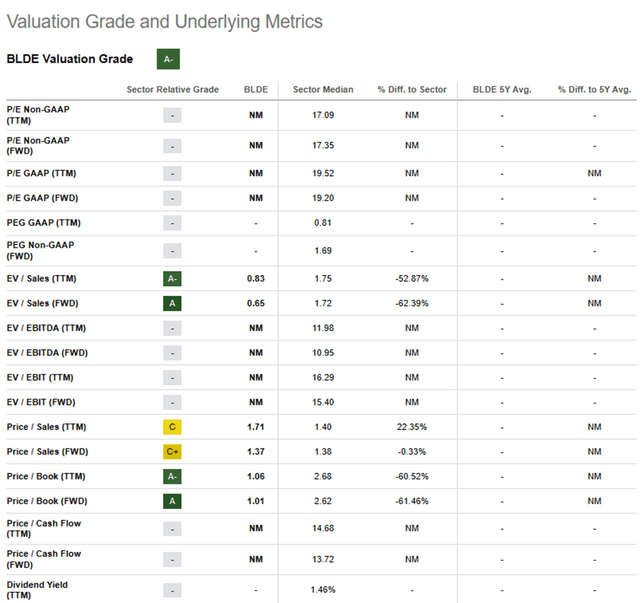

Valuation

I evaluate the value of BLDE based on the company’s business model when it reaches a large-scale operation on its desired network and starts generating profits from deploying eVTOLs around 2025-2026. However, it’s important to acknowledge that there are significant risks associated with executing these plans, including potential changes in the competitive landscape, aviation regulations, and the ability of the electric vertical aircraft industry to deliver eVTOLs that meet safety, noise and cost specifications. My end-of-year price target of $6.5 is derived by using a forward EV/ Revenue multiple of 1.5x applied to the 2024 revenue estimate of $270 million.

Seeking Alpha

Risks

The main risk to my price target is the possibility of slower-than-anticipated adoption of the company’s business model and services. If the rate of adoption is slower than expected, it will result in lower revenues compared to consensus estimates. The company provides high-end, premium services that are discretionary in nature. Any economic downturn or weakness would adversely affect discretionary spending, which in turn would have a negative impact on Blade’s financial performance. Moreover, considering that Blade operates in the air transportation sector, there are stringent regulations in place concerning safety. The introduction of additional regulations that are challenging or costly to implement could pose a risk to Blade’s operations and financial outcomes.

Conclusion

Blade is a pioneer in Urban Air Mobility, experiencing strong growth and is expected to further accelerate its momentum. The company’s growth will be fueled by increasing brand awareness and the growing popularity of its innovative on-demand and scheduled flight services. Blade’s asset-light approach allows them to be flexible and adapt to various use cases. With an established brand, software platform, and infrastructure, Blade has a competitive advantage that poses challenges for new entrants in the market. I view the stock as a long-term buy and have an end-of-year price target of $6.5 on the stock.

Read the full article here