Investment Outlook

Blend Labs, Inc. (NYSE:BLND) reported financial results for the first quarter of 2024, beating revenue and earnings estimates.

I previously wrote about Blend in November 2023 with a Sell outlook due to declining revenue and heavy operating losses.

The company is changing its focus to smaller clients, which may increase operating costs while shortening sales cycles.

The stock has increased in value significantly recently, but interest rates and home prices remain high, restraining activity and the potential for revenue growth.

I’m now Neutral on BLND, given the likely improved earnings from its Haveli investment and the potential for improvement.

Blend Labs’ Market And Approach

Blend Labs provides mortgage origination and related software and services to mortgage and other loan companies.

It also provides title search technologies and escrow and other closing settlement systems.

Per a 2023 market research report by Mordor Intelligence, the global financial services application market was approximately $130 billion in size in 2023 and is expected to exceed $240 billion by 2028.

If achieved, this growth would represent a CAGR (Compound Annual Growth Rate) of 13.13% from 2020 to 2025.

The main drivers for this forecasted growth is the continued demand by financial institutions to improve efficiencies and increase the ease of use and availability of their offerings for all user demographics.

Competitors and other industry players include:

-

MeridianLink (MLNK)

-

Tavant Technologies

-

LenderLogix

-

RealKey

-

Neofin

-

Roostify

-

Kiavi

-

Truework

-

SimpleNexus

-

Major consulting firms

-

Systems integrators

-

Institutional financial software companies.

Recent Financial Trends

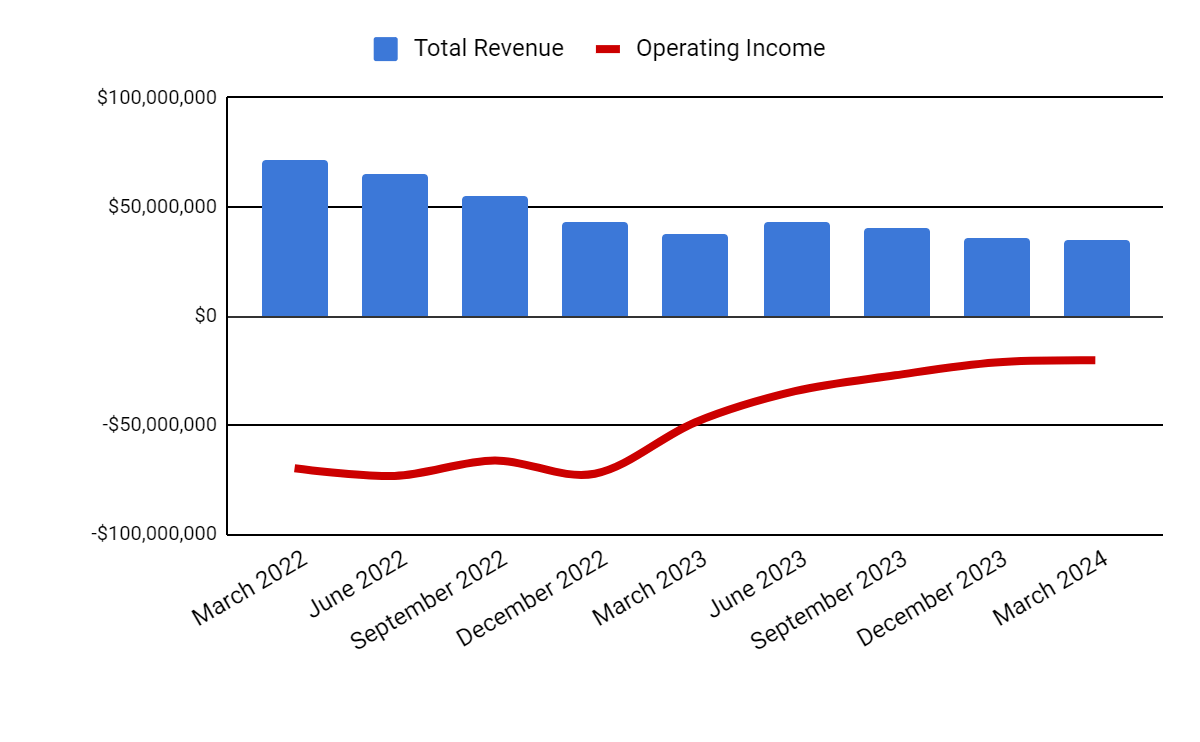

Total revenue by quarter (columns) has continued its decline year-over-year, although the rate of decline has been reduced more recently. Operating losses by quarter (line) have stabilized at around $20 million per quarter, which is still quite high.

Seeking Alpha

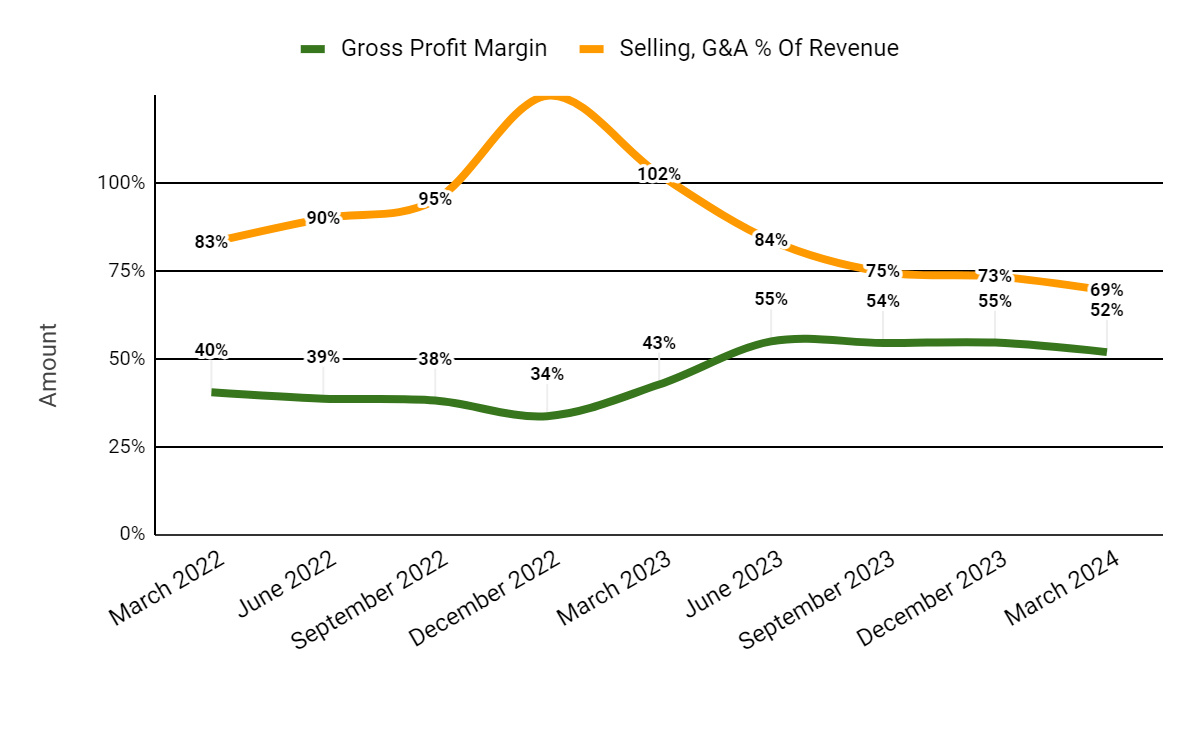

Gross profit margin by quarter (green line) has plateaued and begun to decline in recent quarters as a result of stable expenses against reduced revenue; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have continued to drop as the firm improves its cost controls.

Seeking Alpha

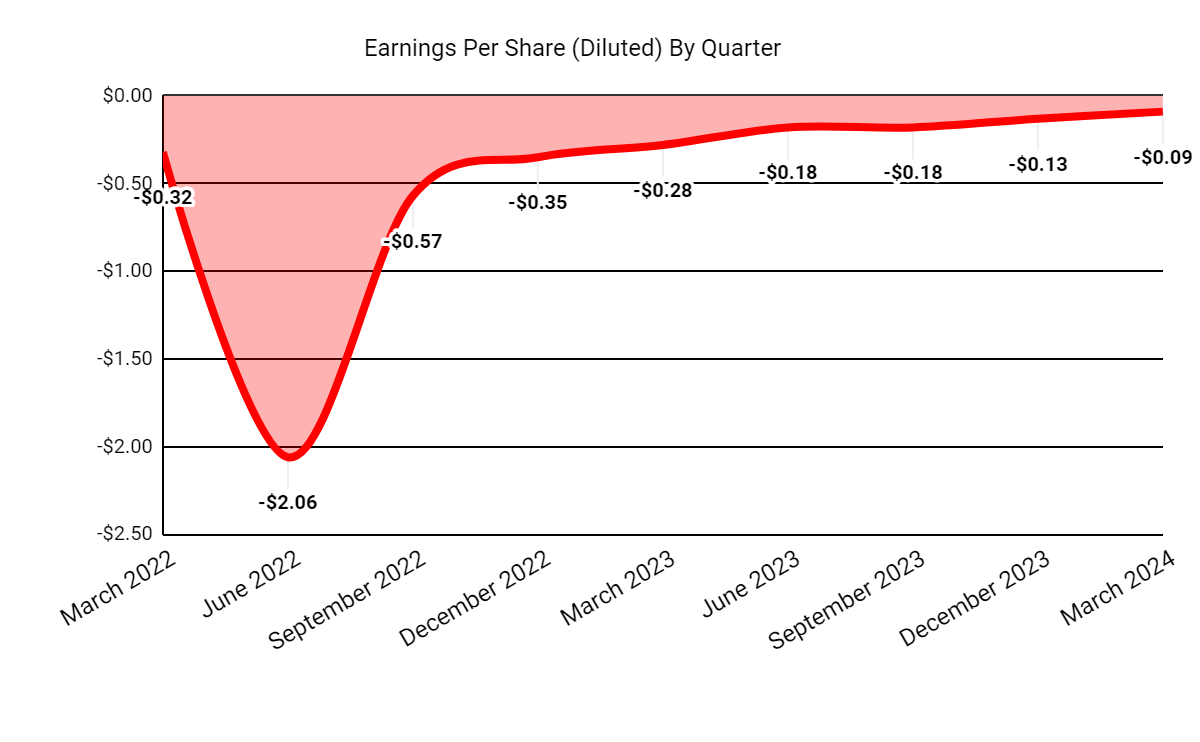

Earnings per share (Diluted) have produced improving results, although the company is still a ways away from earnings breakeven.

Seeking Alpha

(All data in the above charts is GAAP.)

For balance sheet results, BLND ended the quarter with $128 million in cash, equivalents and short-term investments and $138.9 million in total debt, all of which was long-term.

Over the trailing twelve months, free cash used was $87.0 million and capital expenditures were $2.2 million. The company paid a substantial $37.7 million in stock-based compensation in the last four quarters.

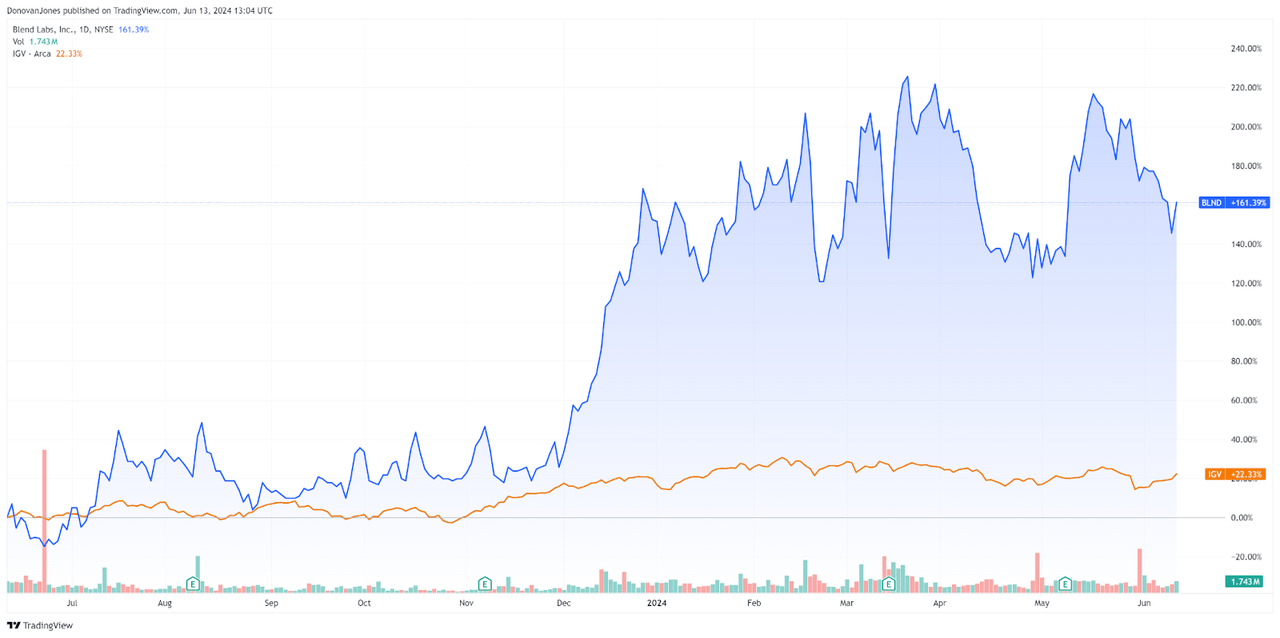

In the past 12 months, BLND’s stock price has risen by 161.4% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) gain of 22.3%, as the chart shows here.

TradingView

Below is a major financial and operating metrics table derived from the company’s financials and estimates:

|

Metric |

Amount |

|

EV/Sales (“FWD”) |

4.3 |

|

EV/EBITDA (“FWD”) |

NM |

|

Price/Sales (“TTM”) |

4.0 |

|

Revenue Growth (“YoY”) |

-23.2% |

|

Net Income Margin |

-86.7% |

|

EBITDA Margin |

-65.0% |

|

Market Capitalization |

$625,900,000 |

|

Enterprise Value |

$695,350,000 |

|

Operating Cash Flow |

-$84,840,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.58 |

|

2024 FWD EPS Estimate |

-$0.14 |

|

Rev. Growth Estimate (“FWD”) |

-3.6% |

|

Free Cash Flow/Share (“TTM”) |

-$0.35 |

|

Seeking Alpha Quant Score |

Hold – 3.42 |

(Source: Seeking Alpha Data.)

Blend’s Rule of 40 performance has improved but remains poor and far from acceptable:

|

Rule of 40 Performance (Unadjusted) |

Q3 2023 |

Q1 2024 |

|

Revenue Growth % |

-40.2% |

-23.2% |

|

Operating Margin |

-66.7% |

-57.9% |

|

Total |

-106.9% |

-81.0% |

(Source: Seeking Alpha Data.)

Why I’m Neutral On Blend Labs

Blend has recently received a $150 million equity investment from Haveli, an Austin, Texas-based private equity firm that focuses on technology companies.

The investment will eliminate the firm’s debt load and related interest expense while providing for increased investment in its technical roadmap.

Management has said its pipeline for new mortgage customers increased sequentially from 30 in the previous quarter to 35, so this could be considered an early signal of a potential upturn or at least stabilization in the quarters ahead.

After a sharp revenue decline in 2023, consensus estimates are expecting a 3% revenue growth but negative earnings of ($0.14) for 2024.

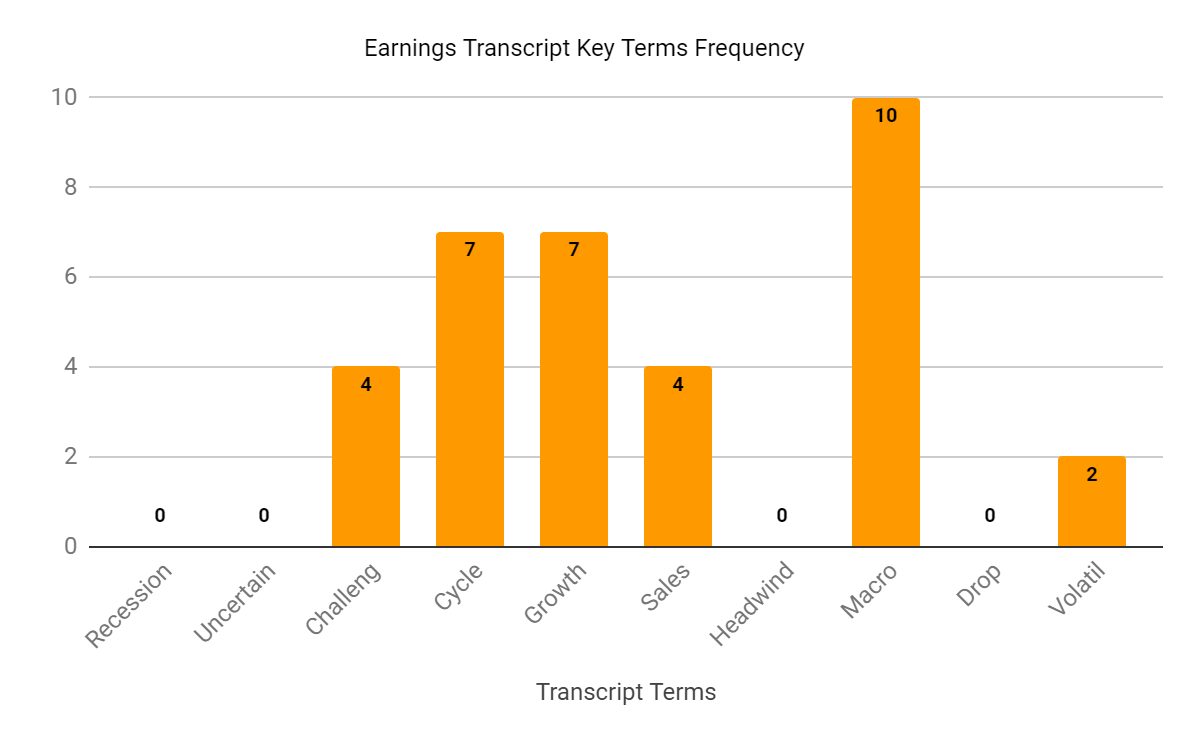

Below is a chart showing the frequency of various keywords and terms in the most recent analyst conference call with management.

Seeking Alpha

I’m interested in the frequency of negative-oriented terms. Blend is experiencing potential stabilization regarding what it is seeing on the macroeconomic front.

Also, the firm continues to see a challenging industry environment, which may only slowly improve as interest rates and home prices remain stubbornly high, reducing activity.

As a result, the company’s current approach is to try to expand its platform offerings to a broader market base, such as smaller community banks and credit unions.

However, the sales & marketing and implementation cost elements of this shift are likely to be higher, requiring a larger number of representatives, even though sales cycles may be reduced on smaller deals.

With reduced interest expense as a result of the Haveli investment, Blend Labs, Inc.’s earnings and cash flow should improve in the quarters ahead, so that’s a positive.

However, management will need to reignite revenue growth while improving operating expenses at the same time, given its market focus shift, and that won’t be easy to do.

So, I’m Neutral (Hold) on Blend Labs, Inc. for the near term on an improved earnings and cash flow outlook but still cautious about its growth prospects ahead.

Read the full article here