Blue Apron Holdings, Inc. (NASDAQ:APRN) surged by over 130% on the announcement that the company would be acquired by Wonder Group, a New York-based mobile restaurant service.

The deal pricing Blue Apron at $13.00 per share, or around $103 million, marks a bittersweet conclusion to what has been a challenging last couple of years. Recent investors have hit a proverbial home run on the news and congratulations are in order. On the other hand, for long-time shareholders, the deal is simply a consolation prize considering the company’s troubled history.

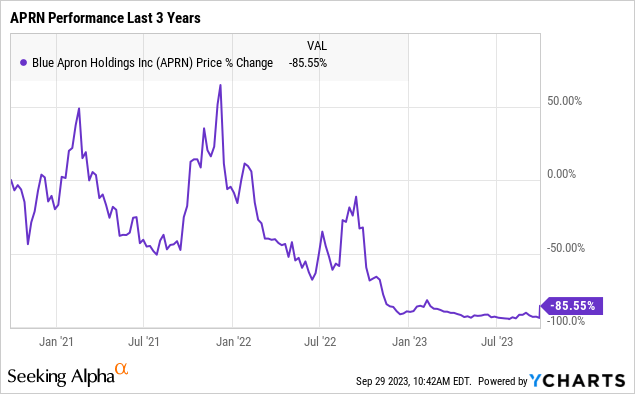

Even with today’s stock price rally, shares are still down more than 80% over the past year and a shell compared to its peak valuation above $2 billion following its 2017 IPO.

Our take is that shareholders should be content with this transaction as a favorable outcome with the path for the stock to reach this price level on its own appearing unlikely. All indications are that the deal will close smoothly with APRN shares tendered for $13.00 sometime in Q4 still this year.

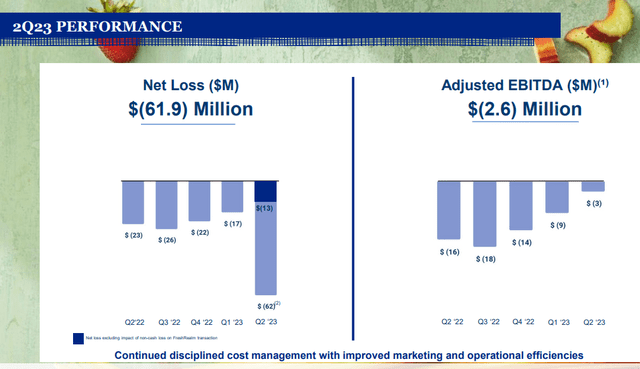

We’ve covered APRN this year highlighting its struggle to reclaim operating momentum with a decline in active customers ever since it captured the pandemic-era demand boom for meal kits. For context, Blue Apron’s 267k customers in the last reported Q2 are down from 349k in the period last year.

The company was making some progress in stemming underlying losses with an effort at cost controls, although an ongoing cash bleed made liquidity and long-term solvency a real concern. The volatile macro backdrop amid pressuring consumer spending wasn’t doing the outlook any favors. The acquisition by Wonder means Blue Apron will survive.

Source: Company IR

As it relates to Wonder, the company has been making a name for itself with its innovative concept where customers order food from premium restaurants with the meals prepared and finished at the delivery site in specialized vans with a trained chef. Recent developments include the launch of a food-hall-style outlet serving selections from multiple partner restaurants.

The idea here is to supplement Wonder’s delivery service and restaurant locations with the flexibility and convenience of Blue Apron’s meal kits as a more complete meal solution for the whole week.

We believe this merger makes sense as Wonder can onboard an established brand name recognized for delivering premium ingredients with a core of loyal customers. The expectation is that Blue Apron operations continue uninterrupted during this transition while Wonder leverages that national network to capture synergies on the marketing side and expand into new cities down the line.

Final Thoughts

The buyout of Blue Apron warrants attention with implications for the broader food-delivery and meal-kits segment of the market. Various players from DoorDash Inc (DASH), HelloFresh SE (OTCPK:HLFFF), Just Eat Takeaway.com N.V. (OTCPK:JTKWY), and tiny ASAP Inc (OTCQB:ASAP) among others are all attempting to make their model work. Larger names like Uber Inc (UBER) and even Amazon.com Inc (AMZN) also have their hand in what remains a growing global opportunity.

We expect that we will see there is room for further consolidation including with restaurant stocks and grocery chains in the mix with the ability to scale being a major advantage. On this point, we’ll keep an eye on Wonder as a future IPO candidate down the line.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here