Investment Thesis

It’s been almost a month since Blue Bird (NASDAQ:BLBD), a school bus supplier, reported results for its third quarter of the year and the share price has not moved at all, despite increasing guidance and widely beating analyst expectations. Therefore, I have decided to maintain my buy rating provided in my last coverage, and I even think that now is even more of an opportunity than a few months ago.

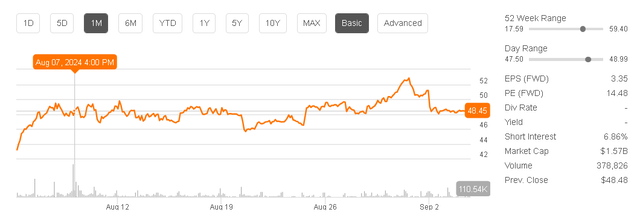

Stock price (Seeking Alpha)

Q3 2024 Earnings Report

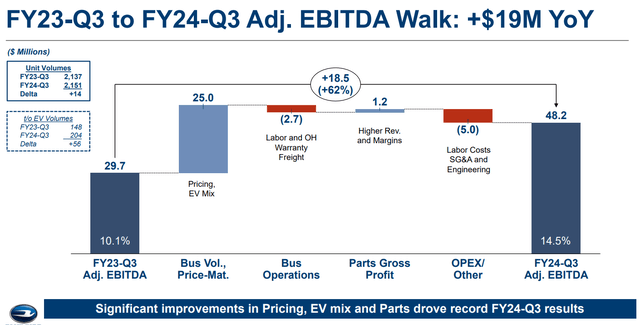

On August 7, Blue Bird presented its Q3 2024 report, in which it largely beat analysts’ expectations in terms of profitability.

Reported $333M in revenue, representing a growth of 13% YoY, very in line with expectations. The surprising numbers came from the EPS side, which was $0.85 compared to the expected $0.51. This represented a net margin of 8.61% and in the first three quarters this would be 8% (this will be important in the valuation).

| Expected | Actual | Beat/Miss | |

| Revenue | $327M | $333M | 2% |

| Adj EBIT | $24.8M | $39.7M | 69% |

| EPS | $0.51 | $0.85 | 66% |

Prior to 2020, the net margin averaged 2%, which can bypass the question of what’s causing this notable increase in profitability and how sustainable it is. The answer comes from two factors:

- Price increase: During the last year, the company has increased the price of its buses by 13% YoY, going from an average price of $127,000 to $143,000. This price increase flows directly to net income because no extra investment is required to raise prices, of course. However, I wouldn’t expect prices to increase this way every year, so I don’t consider it sustainable and rather think that the margins will stay that way until there are new price increases.

- Revenue mix: On the other hand, we have the revenue mix since the sale of bus parts increased in the last year, which has considerably higher margins (on average gross profit of between 40-50% vs 8-10% of the sale of buses). This could be a source of sustainable margin increase over time and seems very positive to me to see it happening.

Blue Bird Q3 2024 Presentation

The Political Affect

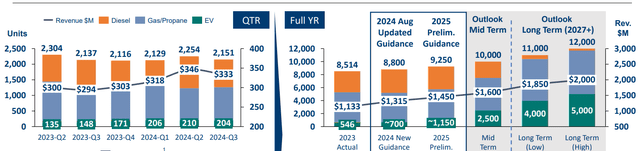

An important part of Blue Bird’s thesis is that it’s expected to play a relevant role in the electrification of school buses. In fact, in the company’s expectations we can notice how 546 electric buses were delivered in FY2023, by FY2024 they expect there to be close to 700 buses (28% YoY growth) and by FY2025 there should be 1,100 buses delivered.

Of course, that’s a lot of growth, but it must be considered that it’s largely supported by the current U.S. government programs, such as the “2024 Clean Heavy-Duty Vehicles Program”, which expects to allocate ~$650M for electric school buses.

Blue Bird Q3 2024 Presentation

Why is this important?

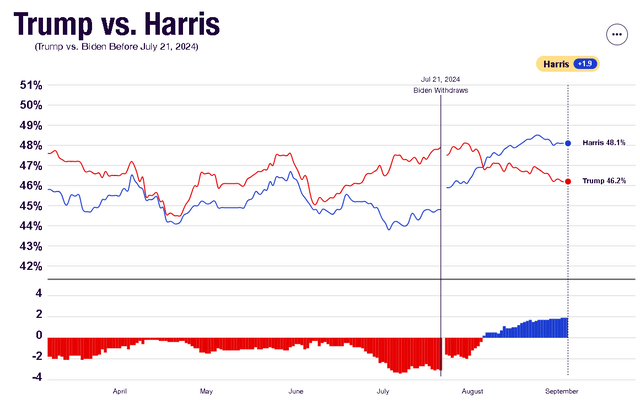

Currently in the presidential race is Donald Trump, who on many occasions has spoken against supporting the electrification of vehicles and that these should only be sold if the project is viable and the companies can survive on their own. This would imply a halt to electrification support programs, therefore affecting Blue Bird’s income to a certain extent.

However, in recent weeks it seems that having the support of Elon Musk, owner of the flagship electric vehicle (EV) company, has made him rethink his ideas. In addition, some of the EV support programs have been bipartisan, so there is a high probability that it will remain that way, regardless of whether Trump or Harris wins. This is what management said in the Q3 earnings call:

Remember, that (The Clean School Bus Act program) was a bipartisan agreement in ’21. Both parties, there was no objection to it. So, I think it’d be very difficult for that to be reversed. There’s so much support for it, and it’s doing so much good for the environment for our children.

CEO Phil Horlock during Q3 2024 Earnings Call.

2024 General Election: Trump vs Harris (Real clear politics)

Valuation

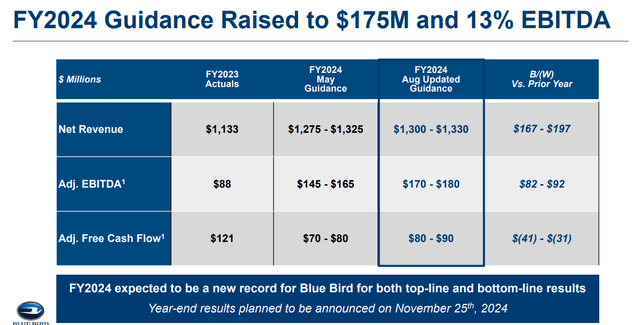

During this quarter, the company increased the guidance again with respect to what was provided in May. Now they expect to earn between $1,300 and $1,330M in FY2024, I consider that they will reach the high range because it would represent making $333M in revenue during Q4 2024, considering they have been making $335M per quarter, it seems more than realistic.

Additionally, they have already given clues about what they expect for FY2025. This would be $1,450 in revenue midpoint during the year, that is, a growth of 10% compared to the previous year. Considering that management gives conservative guidance, I wouldn’t be surprised if growth was higher.

Blue Bird Q3 2024 Presentation

So, having all this information, my assumptions are that this year they will reach $1,350M in revenue and next year will reach $1,450 in sales (midpoint of guidance), just to remain conservative. The net margin would remain at 8% as the bus parts continue to be representative in the revenue mix and assuming that there’s some price increase in the next 5 years that maintains these margins.

Dividing the market cap by the $32.7M of shares outstanding would result in a price per share of $64 for this year (upside of 32%) and almost $100 in five years (doubling the current price). This strikes me as an attractive entry price and sufficient return for a typically stable company.

Valuation model (Author’s compilation)

The multiple of 20 times earnings may seem controversial, but according to Seeking Alpha, it’s around the average of what this sector usually trades and seems reasonable to me considering that it’s an industry with few relevant players, supported by government programs and surrounded by a macrotrend of renewing school buses.

In the end, we’re talking about the means of transportation for America’s children; therefore, it seems difficult for schools and governments to want to cut costs on this.

Valuation (Seeking Alpha)

The Bottom Line

During the quarter, the company confirmed the trend toward growth and improved margins. It beat all expectations, bus parts sales continue to be relevant, and it’s trading at 15x earnings; however, the price action was somewhat disappointing, and the shares have remained flat since the day of the report.

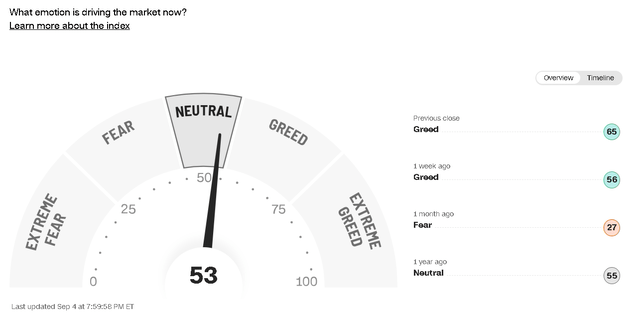

So far, I haven’t found what the market didn’t like, but it seems like a lack of action because we are in a neutral/fearful market. Therefore, I think it’s a buy and I maintain my rating from the previous analysis.

Fear and greed index (CNN)

Read the full article here