Brookfield Corporation (NYSE:BN)(TSX:BN:CA) and Brookfield Asset Management (NYSE:BAM)(TSX:BAM:CA) are two of the best ways to invest in the Brookfield financial empire. Brookfield is a 75% owner of BAM, and a major financial holding company. Brookfield Asset Management is a pure-play asset management company, active in infrastructure, private equity and credit.

There’s a lot of overlap between BN and BAM. There’s Brookfield’s 75% ownership interest in BAM, of course. On top of that, Brookfield is invested in BAM’s real estate funds, while having several wholly owned subsidiaries in financial services. So, there are many similarities between the two Brookfields.

There are differences, too. A big one would be the use of leverage. Brookfield has $210.46 billion in non-recourse borrowings, vs $146 billion in shareholder equity. This gives us a debt-to-equity ratio of 1.43, which is fairly high, suggesting a very levered company. BAM on the other hand has $6 billion in debt, compared with $11.6 billion in equity, giving a 0.517 debt to equity ratio. This is a function of BAM’s asset light business model: the company manages other peoples’ money rather than its own, and as a consequence has few assets or liabilities.

If you look at Brookfield and Brookfield Asset Management without thinking about their valuations, you might be inclined to think that the latter is the better business. It has a stronger balance sheet than BN does, and its margins are far higher. Indeed, I do think that BAM is a better business than BN, but the flipside is that BN has the cheaper valuation of the two.

In this article, I will explore Brookfield and Brookfield Asset Management side by side, to help readers determine which, between the two, is the better investment. I will explore each company’s balance sheet, quarterly results, competitive position and valuation side by side, to see which of the two stocks is the better buy. In the end, I conclude that both stocks have their advantages, but that one is better than the other from a valuation perspective.

Balance Sheet

Between Brookfield and Brookfield Asset Management, there is no question:

BAM has the better balance sheet.

According to Seeking Alpha Quant, Brookfield boasts the following balance sheet metrics:

-

$456.7 billion in assets.

-

$308.8 billion in liabilities.

-

$52.2 billion in current assets.

-

$84.7 billion in current liabilities.

-

$146.9 billion in common equity.

-

$173.5 billion in long term debt.

This gives BN a 0.61 current ratio and a 1.18 debt to equity ratio. Usually a current ratio above one and a debt to equity ratio below one are considered ideal, so BN’s balance sheet shows signs of heavy leverage.

Now let’s look at Brookfield Asset Management:

-

$18.8 billion in assets.

-

$3.3 billion in liabilities.

-

$15.57 billion in common equity.

-

$7.9 billion in current assets.

-

$3.15 billion in current liabilities.

-

$125.7 million in long term debt.

This gives us a 2.5 current ratio and a 0.008 debt/equity ratio–both far better than the same ratios for Brookfield.

Quarterly Results

Next, we can compare Brookfield and BAM in terms of their quarterly results.

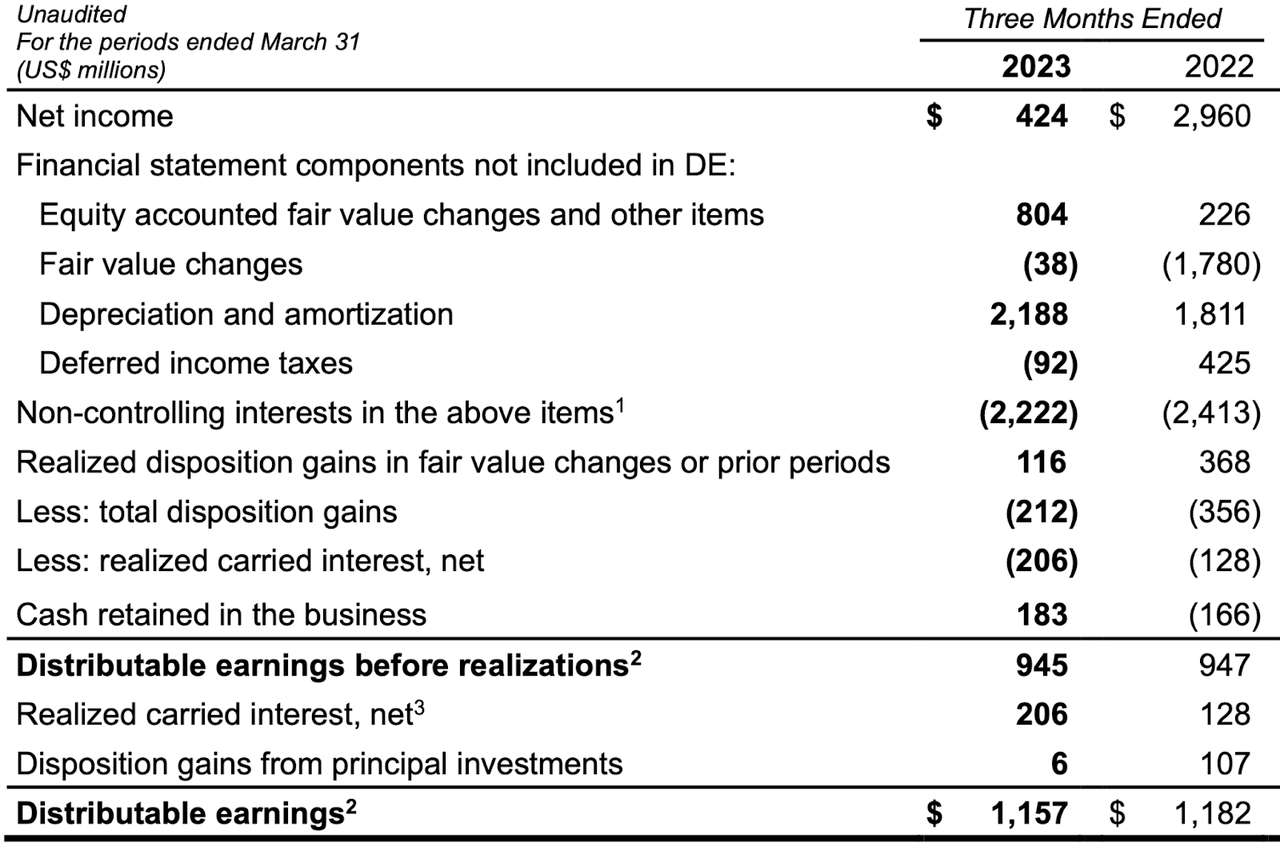

In Brookfield’s most recent quarter, the company delivered:

-

$23.29 billion in revenue, up 6.4%.

-

$424 million in net income, down 85%.

-

$.05 in diluted EPS, down 93%.

-

$945 million in distributable earnings, down 0.2%.

The large decline in net income might look bad but it’s important to note that it was largely due to non-cash factors like fair value changes and an increase in depreciation. Distributable earnings were nearly flat year over year. According to Seeking Alpha Quant, Brookfield beat on revenue but missed on earnings in its most recent quarter.

Brookfield Earnings (Brookfield)

Next up, we have BAM’s earnings. In its most recent quarter, BAM delivered:

-

$1.054 billion in revenue, up 39.6%.

-

$59 million in investment income, up from a $1 million loss.

-

$609 million in income before taxes, down 29%.

-

$516 million in net income attributable to common shareholders, up 48.2%.

As you can see, growth at Brookfield Asset Management is much faster than at Brookfield. This shouldn’t be surprising, as BAM doesn’t have anywhere near as much debt as BN, and therefore isn’t taking on as much cost from interest rate hikes. Seeking Alpha Quant reports that BAM’s most recent quarter was a beat on FFO. Overall, BAM’s most recent quarter was more impressive than BN’s.

Competitive Position

Next up, we need to look at Brookfield and BAM’s competitive positions. This part of the analysis is complex because Brookfield owns the majority of BAM, and both companies are essentially investment management firms. The big difference is that Brookfield invests its own balance sheet assets. So, Brookfield and BAM compete against the same companies.

A big competitor to Brookfield and BAM is KKR & Co (KKR). Like Brookfield and BAM, it both runs funds and invests its own balance sheet. There is potential for Brookfield and BAM to compete with KKR when bidding on an asset, although KKR’s asset mix is much more eclectic than that of the two Brookfields. It owns a lot of tech and pharmaceutical assets, which Brookfield and BAM don’t compete on them with.

Next up we have the Carlyle Group (CG). Like Brookfield, it is heavily invested in infrastructure, including renewables. It has a global credit business that competes with Brookfield Oaktree Wealth solutions.

There is some competition in Brookfield’s industry. Asset management has a lot of players in it, though specialized funds like Brookfield’s face less “race to the bottom” fee competition than index ETF vendors do. Brookfield, therefore, is in a relatively good niche within asset management.

The real question here is whether Brookfield or BAM is better situated to deal with competitive threats. I’m inclined to think that Brookfield is, mainly because it doesn’t face the issue of redemption requests–at least not directly. Brookfield owns 75% of BAM and large stakes in several Brookfield funds. It is exposed to the same risks BAM and the other Brookfield companies/funds are, but it also invests its own balance sheet assets. In this part of its business Brookfield does not face the risk of clients withdrawing funds and having to sell off holdings in order to meet the obligations. BAM does, so the larger Brookfield has an advantage in being able to buy and hold.

Valuation

Next up, we have valuation. This factor clearly favors Brookfield. At today’s prices, Brookfield trades at:

-

11.11 times forward earnings.

-

80 times GAAP earnings.

-

0.55 times sales.

-

1.31 times book value.

-

5.85 times operating cash flow.

Meanwhile, Brookfield Asset Management trades at:

-

23.92 times forward earnings.

-

6.26 times GAAP earnings.

-

3.32 times sales.

-

1.37 times book value.

Apart from the trailing earnings multiple, Brookfield is cheaper. BAM’s smaller trailing P/E ratio might make it look cheap, but remember that Brookfield’s earnings were affected by a large increase in non-cash expenses and asset value changes last quarter. These non-cash charges don’t affect free cash flow.

Insider Buying

Last but not least, we have the matter of insider buying. Insiders buying stock in a company is thought to signal good things ahead, as it shows that the company’s most informed investors think it’s a buy.

Brookfield has been seeing a lot of insider buying lately. According to Canada’s Globe and Mail, Bruce Flatt bought 1.17 million shares last month, Brian Lawson bought 52,425 shares, and Jack Crockwell bought 1.2 million shares. BN stock cost about $42 when these buys were made, so collectively we have over $100 million in BN stock being bought by insiders in May.

The insider signals are less positive for BAM. Bruce Flatt has mostly been selling that stock this year, with multiple sales of over 100,000 shares. Given the simultaneous selling of BAM and buying of BN, it looks like Flatt thinks that Brookfield is the better value today. On the whole, the ‘insider buying’ factor favors Brookfield.

The Bottom Line

Having compared Brookfield and Brookfield Asset Management side by side, I’ve concluded that Brookfield has more potential upside. It’s cheaper, it’s just barely above book value, and it has upside if it just reaches a valuation commensurate with the sum of all its holdings. In a recent Seeking Alpha Article, Alexander Steinberg showed that Brookfield was at a 27.3% discount to the sum of its parts. So, there’s potential for gains here even if there is no growth.

Brookfield Asset Management is not as cheap as Brookfield. However, it is less risky. With a much stronger balance sheet and barely any debt, it is unlikely to suffer from credit-related issues or a deteriorating financial position. It appears to be the ‘safer’ of the two stocks, taking everything into account.

Read the full article here