Introduction

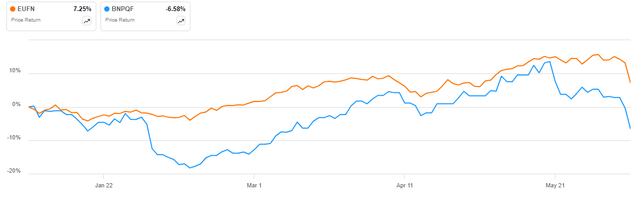

BNP Paribas (OTCQX:BNPQF) has underperformed the iShares MSCI Europe Financials ETF (EUFN) so far in 2024, with the shares delivering a mid-single-digit loss against a mid-single-digit gain for the benchmark ETF:

BNPQF vs EUFN in 2024 (Seeking Alpha)

The culprit as you may guess is the upcoming parliamentary election in France, with the first round of voting set for June 30, with a second round on July 7. This has caused a significant decline in French financial assets across the board, and in my opinion, creates a buying opportunity in light of the valuation the bank trades at.

Company Overview

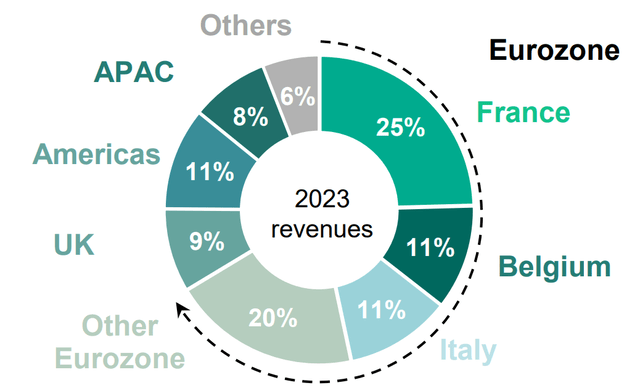

You can access all company results here. BNP Paribas is a French bank with significant European and global exposure, with the French market contributing just 25% of BNP’s revenue. The Eurozone as a whole has a 67% share in the company’s top line:

Revenue breakdown by region (BNP Paribas June 2024 Investor Presentation)

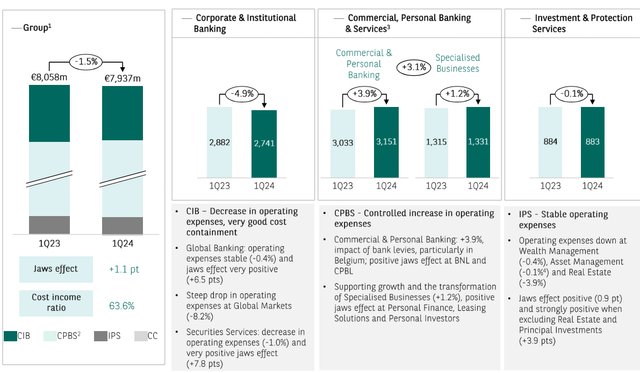

From a segment perspective, the bank derives some 55% of its revenue from the Commercial, Personal Banking & Services segment (CPBS), followed by Corporate & Institutional Banking (CIB) with a 34% contribution, and Investment & Protection Services (IP) at around 11%:

Segment results overview (BNP Paribas Q1 2024 Results Presentation)

Operational Overview

Commercial, Personal Banking & Services pre-tax income was 13.5% lower Y/Y, driven by higher expenses and larger credit loss provisions. Revenue increased 0.4% Y/Y driven by higher fees in Commercial & Personal Banking.

Corporate & Institutional Banking delivered 2.4% Y/Y higher pre-tax income Y/Y boosted by provision releases, while topline revenue was 4% lower Y/Y on weakness in Global Markets.

Investment & Protection Services was the best-performing segment, with a 5.6% Y/Y increase in pre-tax income driven by 4.2% Y/Y revenue growth, which was broad-based across all segments.

For the bank as a whole, the return on tangible equity, or ROTE, stood at 12.4% in Q1 2024, the tangible book value per share was €93.4/share, up 3.5% Q/Q, while EPS was €2.51/share. Revenues were 0.4% lower Y/Y while operating expenses decreased 1.5%.

2024 Outlook

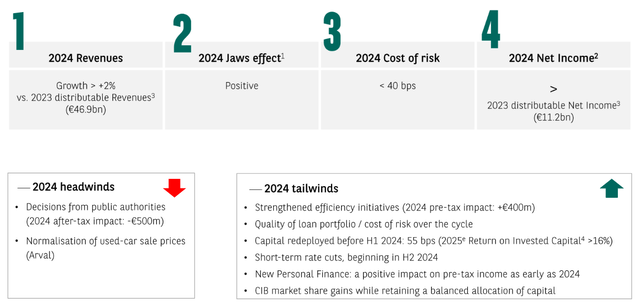

Following the positive start to the year, the bank expects revenue growth to accelerate going into the second part of the year, with 2% higher revenues and net income on par, or even larger, compared to 2023:

2024 Guidance (BNP Paribas Q1 2024 Results Presentation)

As a result, I expect the bank to reach a ROTE of about 12% in 2024 (ROTE averaged 12.8% in 2023, although we should note it was decreasing throughout the year, starting at 14.1% in Q1 2023 and ending at 10.7% in Q4 2024), with expectations for 2025 marginally below 12% before a recovery going into 2026.

Capital Position

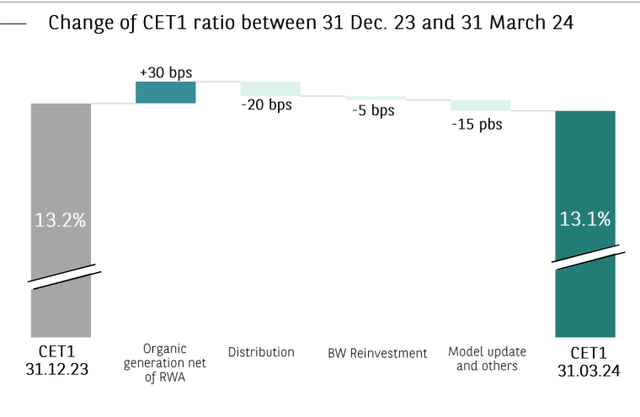

BNP Paribas ended Q1 2024 with a CET1 ratio of 13.1%, down 0.1% Q/Q on model updates and distributions, partially offset by organic capital generation:

CET1 capital bridge (BNP Paribas Q1 2024 Results Presentation)

The current regulatory requirement is for a CET1 ratio of 10.2%, implying that BNP Paribas has a 2.9% capital buffer.

Comparison with ING

I think ING (ING) is a good comparison for BNP Paribas because:

- Both banks have stable operations and are arguably at the peak of their profitability (no turnaround story).

- They have a similar size and business model, notwithstanding some differences.

- They derive a majority of their revenue from the Eurozone.

- They have a similar long-term ROTE target of about 12%.

- The Netherlands is close to forming a right-wing government, which has been the most pressing concern for French investors in the past week.

Of course, you may argue that due to election specifics (the parliamentary vote in France is held in two rounds, with contenders with over 12.5% continuing to the second round) the far right may win more seats compared to the Netherlands. In any case, my base case is that even if the far-right wins in France, the government formed will be a watered-down version of the initial far-right promises, as what happened in the Netherlands.

Here is how BNP Paribas compares with ING:

| IndicatorBank | BNP | ING |

| ROTE, Q1 2024 | 12.4% | 13% |

| Price/Tangible book value, June 2024 | 0.65 | 1.01 |

| CET1, Q1 2024 | 13.1% | 14.8% |

| Earnings yield on tangible equity | 19% | 12.9% |

Source: Author calculations based on company disclosures

The last indicator, the earnings yield on tangible equity, takes into account the first two indicators, ROTE and Price/Tangible book. In essence, it not only looks at how much the bank makes but also its valuation in terms of tangible book value. Long-term, I think this is the most persistent indicator you can use, since it looks at both profitability and valuation.

We observe that BNP offers a circa 6% earnings yield to tangible equity premium relative to ING. For BNP to trade at a similar valuation to ING, the stock would have to rise to about €90/share, or almost 50% higher than the current share price.

We should note ING currently has a stronger capital position, but it is actively watered down by buybacks, which at no discount to tangible book value are not very value-accretive in my view.

Risks

The main risk facing BNP Paribas is obviously a significant deterioration of the business environment following the parliamentary elections in France. With the result highly uncertain, new bank levies may be introduced, reducing banks’ profitability. However, as shown in the previous paragraph, some negative developments are already priced in.

The other key risk is that the European Central Bank is only getting started with interest rate cuts. As such, you should be very selective when entering new bank positions, given the industry-wide headwind faced by lower rates. I think that the current valuation of BNP Paribas compensates for the lower net interest income risk.

Conclusion

BNP Paribas shares have fallen recently after a snap parliamentary election was called by President Macron. With the bank delivering robust results and trading at a significant discount to peers such as ING, I think the opportunities outweigh the risks; hence, I rank the shares as a buy. I believe any re-rating of the shares will only be gradual as the new French government and its policies gradually take shape.

Thank you for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here