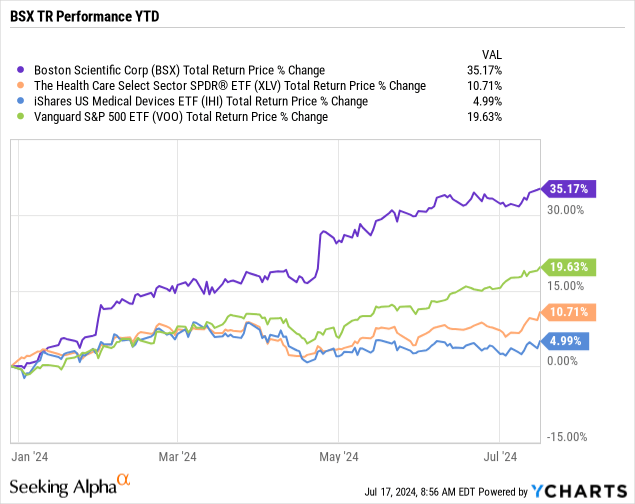

Boston Scientific (NYSE:BSX) is set to report its second-quarter earnings on July 24. Expectations are high for this medical technologies giant following what has been an impressive share price rally in the first half of 2024. The stock is up 35% year-to-date, well ahead of healthcare sector benchmarks.

We last covered BSX ahead of its first quarter report back in April highlighting the company’s financial momentum, with new product launches driving a growth resurgence. On the other hand, we also noted the stock’s pricey valuation as warranting some caution for investors watching the stock make a series of all-time highs.

With no signs of letting up, can the rally continue? Our update today focuses on the themes to watch into the second half of the year.

BSX Q2 Earnings Preview

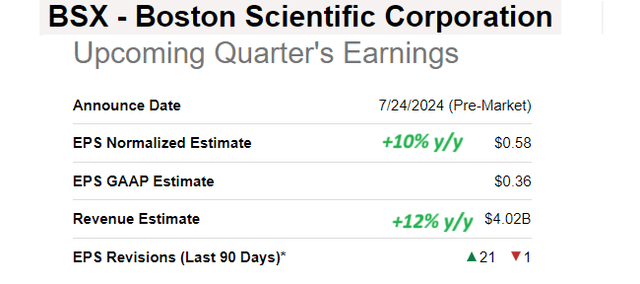

According to consensus, Boston Scientific is expected to report fiscal second-quarter EPS of $0.58, for the period ended June 30. If confirmed, this result will represent a 10% year-over-year increase, which is within the company’s Q2 guidance for adjusted EPS between $0.57 to $0.59 announced with the Q1 report. The forecasted Q2 revenue of $4.02 billion is an increase of 12% from the period last year.

Notably, the company beat Q1 estimates with the big headline last quarter being management’s updated full-year guidance coming in well ahead of market estimates. That dynamic is evident as BSX has seen 21 revisions higher to the Q2 EPS estimate over the last 90 days, which helps explain the continued bullish sentiment towards the stock.

Seeking Alpha

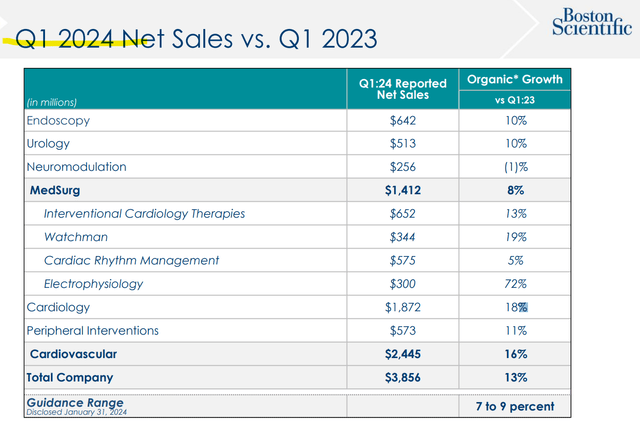

The market will look for a continuation of Q1 trends where the Cardiovascular segment stood out with a 16% organic revenue growth over Q1 2023. In this case, the “Watchman FLX Pro Left Atrial Appendage Closure” device and “POLARx” FDA approved in 2023 have received a strong market response, driving new orders for Boston Scientific into 2024.

For Q2, its expected initial sales of the “FARAPULSE Pulsed Field Ablation System”, which was FDA approved in January, ramp up as an incremental growth driver.

The other major theme has been the ongoing international expansion. While sales outside the United States still represent approximately 41% of the business overall, the company is gaining traction in regions like Asia-Pacific, where Q1 operational growth climbed by 26% y/y and 28% in the broader emerging markets group. This is important as it indicates Boston Scientific is becoming more diversified as a runway, supporting its positive long-term outlook.

source: company IR

In terms of financials, the trend in margins has been mixed based on the shifting sales profile and inventory changes. The Q1 adjusted gross margin at 69.8% was down from 70.4% in the period last year even as the adjusted operating margin climbed by 70bps to 26.2% based on the top-line momentum.

Still, management has reiterated a goal of improving the gross margin profile, which is good news for further earnings upside into next year and beyond. This has been discussed by management. From the Q1 earnings conference call:

So, gross margin at that 69.8%, I didn’t love that this quarter, but I’m optimistic that that improves through the year. But absolutely, in ’25 and ’26, I think gross margin can contribute. Recall, we used to be at 72.4% gross margin back in 2019. We’re maniacally focused on getting back and improving that from where it is today and have the plans to do that.

What’s Next for Boston Scientific?

Shares of Boston Scientific have rallied by more than 12% since the Q1 results were released a bit less than three months ago. We’ll admit that the earnings strength and stock price performance to start the year surpassed our expectations, leaving us on the sidelines during this last leg higher.

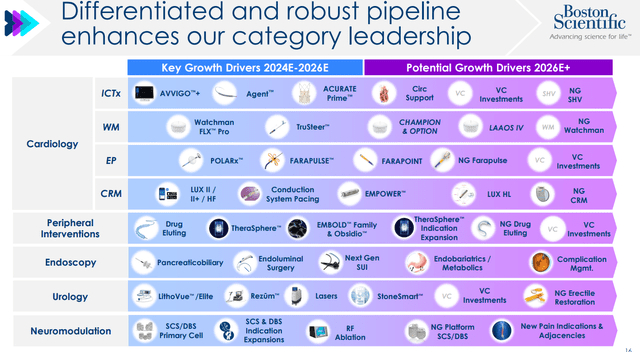

It’s clear to us now that the operating and financial tailwinds are part of a bigger story, which is the company’s ability to gain and consolidate its market share and leadership position in key areas of medical technologies. The attraction here is the extensive product pipeline representing significant growth opportunities in various categories over the next several years.

The company’s record of innovation includes several strategic acquisitions, including the $3.7 billion deal for Axonics, Inc. (AXNX) earlier this year and Silk Road Medical (SILK) for $1.2 billion just last month.

Ultimately, Boston Scientific’s ability to leverage its expanding medtech ecosystem into higher profitability should keep the stock supported.

source: company IR

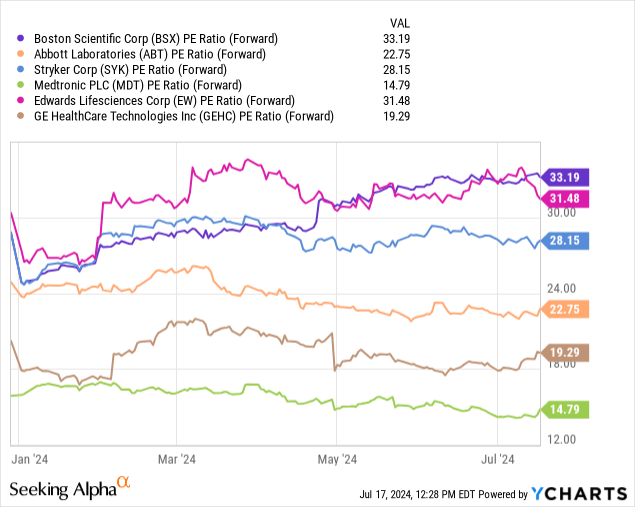

All that being said, we come back to the main knock on BSX which is its pricey valuation, trading at a premium to a peer group of large-cap and high-profile medtech stocks.

BSX is trading at 33 times its consensus full-year EPS of $2.33, which is well above the average for companies within medical devices such as Abbott Laboratories (ABT), Stryker Corp (SYK), and Edwards Lifesciences Corp (EW) with an average forward P/E closer to 27.5x.

One interpretation here is that BSX may be slightly overvalued, with its growth story hardly a secret in the market. While that doesn’t mean shares need to sell or crash lower from here, it does raise the risk for renewed volatility in a scenario where results over the next few quarters disappoint.

Simply put, the higher shares of BSX and the corresponding earnings multiple climbs, the challenge becomes greater for the company to keep beating market expectations. A bearish view would question whether much of the positives have already been priced in.

Final Thoughts

We reaffirm a hold rating on shares of BSX, implying a neutral view on the stock price over the next year. Investors lucky enough to get in low and early should stay the course, while investors just eyeing the stock may likely find more attractive opportunities with better value elsewhere in the market.

We predict that Q2 earnings will just match previously issued management guidance and the market consensus, resulting in an otherwise muted reaction. Sales trends from the Cardiovascular segment as well as the evolution in margins will be key monitoring points.

Read the full article here