British American Tobacco (NYSE:BTI) is a leading producer of tobacco and smokeless products. It owns well-known brands that are marketed globally which include, Dunhill, Lucky Strike, Rothmans, Kent, Pall Mall. It has brands that are popular in the United States which include Camel, Natural American Spirit and Newport. It is also selling vapor products such as Vuse, and heated tobacco with Glo being a top brand. The share price of this company appears very undervalued and I believe it has bottomed out. There are a number of reasons why I am planning to accumulate this stock on pullbacks. In the past few days there has actually been a small pullback and that has prompted me to start buying more shares. Let’s take a look below at the pros and cons and why this appears to be a good time to buy this very high-yielding stock.

The Chart

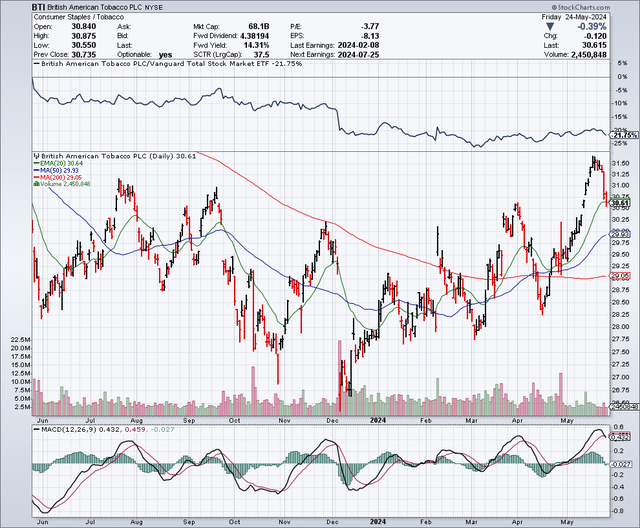

As shown below, this stock plunged and bottomed out in December 2023. The sharp drop in that month was due to an announcement from BTI that it would take a $31.5 billion impairment charge for the brands it owns in the United States. The stock has since been able to rally from that level and it has been in a bit of an uptrend. The 50-day moving average is $29.93 and the 200-day moving average is $29.05.

StockCharts.com

Earnings Estimates And The Balance Sheet

Analysts expect this company to earn $4.71 in 2024, on revenues of $34.22 billion. For 2025, estimates are at $4.98 per share, with revenues coming in at $35.37 billion. Results for 2026 are expected to rise further with earnings estimates at $5.23 per share, with revenues totaling $36.44 billion. These estimates do not show a business that is declining, but rather one that has some growth which can easily support the dividend which is very well covered by earnings. I think this stock is extremely undervalued as it currently trades for just about 6.5 times earnings estimates for 2024, and for less than 6 times earnings estimates for 2026. I like investing in companies that are expected to earn an amount that is equivalent to the current share price in just about 6 years. As the saying goes, “good things happen to undervalued assets”. I expected that between a very generous dividend and potential share price appreciation, this stock will provide strong total returns.

As for the balance sheet, BTI has $50.89 billion in debt and around $6.71 billion in cash. In March 2024, Fitch upgraded BTI’s credit rating to “BBB+”. This upgrade was driven by a number of factors, including “improved leverage metrics”, and the expectation of further deleveraging driven by “improved profitability and strong free cash flow”. If these trends continue, I expect BTI to see more credit rating upgrades in the future which could further boost investor confidence and reduce interest expenses.

The Dividend And Share Buybacks

BTI pays a quarterly dividend of about $0.74, and this provides a yield of just over 9.5%. This yield is very generous and yet it is very well-covered by the earnings estimates, which suggests it is secure.

Another way this company is being shareholder-friendly is through major share buybacks. For example, in March 2024, BTI announced it had sold part of the stake it has in an Indian tobacco company named “ITC” and that it would use these proceeds to buy $2 billion worth of stock.

Industry Outlook And Valuation

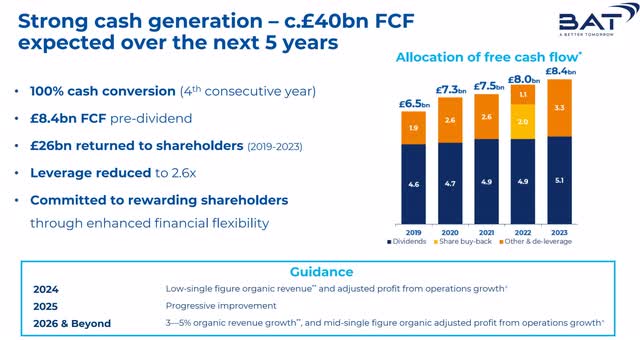

Smoking cigarettes is declining by about 3% annually and that would seem to be a problem, except for the fact that price increases of about 4% per year, more than offset this decline. As shown below, BTI is guiding for 3% to 5% in organic revenue growth for 2026 and beyond:

Bat.com

The barriers to entry for new competitors are extremely high because of regulations and other factors. Advertising tobacco products is not allowed in many countries and that also makes it hard for a new competitor to emerge and it also keeps the advertising budget low for BTI.

In terms of valuation when compared to peers, BTI looks very undervalued. For example, Altria (MO) is expected to earn just over $5 per share for 2024, and it trades for about $45. This implies a price to earnings ratio of about 9 times earnings. Analysts expect Philip Morris to earn about $6.30 per share and it trades for around $100 per share. This implies a price to earnings ratio of about 15. That is more than double the price to earnings ratio that BTI currently holds. Part of this is due to the belief that Philip Morris is ahead in the smokeless product market, but I still think this shows that BTI is undervalued and it could get re-rated higher in the future.

Why The Window To Lock In This Yield Could Be Closing

There are two big reasons why the opportunity to lock in a yield of about 9.5% might not last much longer. The first reason is obviously because BTI shares trade at a discount to Altria and Philip Morris. Much of this discount was created when BTI took the big $31.5 billion write-down, which I believe was an overreaction.

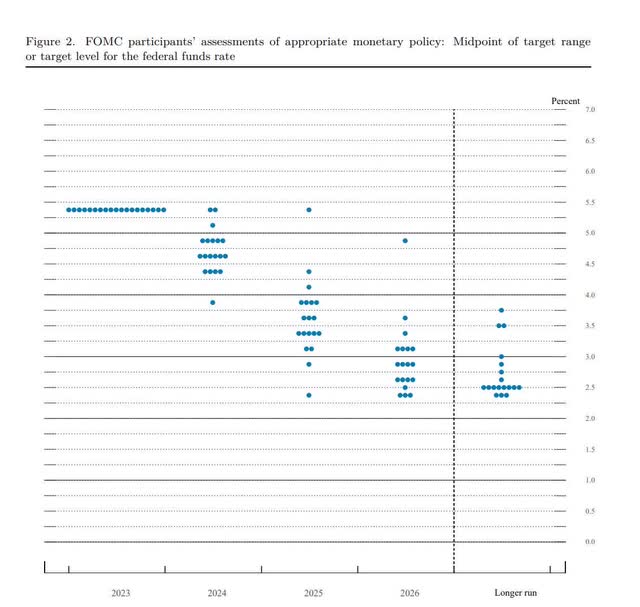

The other even bigger reason in my view is going to be a big drop in interest rates over the next couple of years. The “dot plot” projections for the Fed Funds Rate from the FOMC, suggests that interest rates could go from what is currently over 5%, and plunge down to as low as around 2.25% by 2026.

FederalReserve.gov

This means we could see the yield on money market funds drop by 50% between now and 2026. When money market fund rates are down to this level of 2.5%, it makes sense that investors will sell their money market funds and pay higher prices for dividend stocks. I believe this will be a major upside catalyst for BTI shares. The market is currently willing to price BTI with a yield of about 9.5% when money market rates are yielding just over 5%. However, I don’t see the market offering BTI with a 9.5% yield, if money market rates are around 2.25% in 2026. That means BTI shares could move much higher. If money market rates drop to about 2.25% in 2026, I could see BTI trading at $50 per share because the current dividend payout of nearly $3 per share would still provide a yield of about 6%. This could still triple the projected yield of 2.25% for money market funds.

Other Upside Catalysts

Marijuana could be legalized in the U.S. and other countries in the future. This could create an entirely new market for tobacco companies like BTI and create industry growth. If this occurs, I believe that price to earnings multiples will expand significantly.

BTI still owns a big stake in ITC, and that stake is currently worth about $16.5 billion. This is a very significant “hidden asset” that BTI owns and selling more or all of this could give the company the opportunity to buy back more stock, reduce debt and even pursue new growth opportunities; for example, the marijuana market potentially, in the future.

BTI And The Rule Of 72

When investing in dividend stocks, it is worth considering the “Rule of 72”. This enables you to calculate how long it will take to double your money. It works by dividing 72 by the yield. With British American Tobacco currently yielding about 9.5%, by dividing 72 by 9.5, it shows it will take around 7.6 years to double your money with the dividend. However, this stock could take even less time than that because of potential share price appreciation. I expect this stock to rise when interest rates decline over the next couple of years.

Potential Downside Risks

Since this company is based in England, and because it derives most of its revenues from many other countries, it does have some currency risks, in particular if the British pound rises in value.

If governments make an outright ban on the sale of tobacco products, this would be a major downside risk. I don’t see that happening because politicians know that many retirees rely on income stocks like BTI and this industry provides significant tax revenues to the government. If smoking rates decline at a more rapid pace in the future, this would also make it challenging for this company to meet earnings estimates.

A global recession is another potential downside risk to consider. In a tough economic environment it could cause some consumers to cut back on discretionary spending. However, it is worth noting that the tobacco industry is recession-resistant relative to other businesses.

In Summary

I see BTI shares as mispriced in part due to the headline grabbing write-down earlier this year, and deeply undervalued. This stock is showing signs of having bottomed out, and the yield is extremely generous now. It will be even more rewarding for investors who lock in this yield now before the Fed Funds Rate and money market rates potentially fall to around 2.25% between now and 2026. I also see BTI’s multi-billion dollar stake in ITC as something more investors should be focused on, especially since the company has started to sell this stake, which could fund more share buybacks.

There could be a very lucrative new growth opportunity for tobacco companies, if marijuana is legalized on a national level in the United States. It seems to be going towards legalization and this is a major potential upside catalyst for the future.

The dividend is too attractive to pass up now, and it appears very secure as the payout is way below earnings estimates for this year and beyond. I see this stock trading back up towards $50 when rates plunge as the Federal Reserve expects between now and 2026.

Read the full article here