Despite being relatively unknown, Broadridge (NYSE:BR) is one of the most important financial service companies in the world. We wrote about it in April 2020. At that time, the company was trading at a discount to the S&P 500. Nowadays, valuations are less attractive and the company is trading with a premium valuation above its historical average, that is why we downgrade the stock to “hold”.

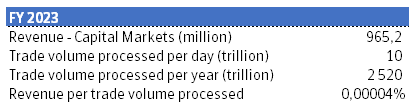

Broadridge operates two different businesses under the same roof (more details below) and serves 3100+ public companies, of which 343 among the S&P 500. Both businesses provide mission-critical services, and the cost of these services account for a tiny part of clients’ overall costs. For instance, trade processing is critical to close a trade and these fees are approximately equal to 0.00004% of the trade volume. In other words, Broadridge needs to process one million of trade volume in equities or fixed income to earn $ ~0.40 of revenue.

(Source: Company reports and Author)

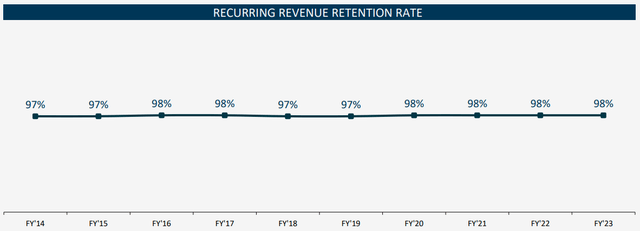

Delivering proxy materials is also a legal obligation, and it accounts for a tiny portion of net income. For instance, McDonald’s (MCD) had 4.5 million beneficial owners at the end of 2023, which represents $ ~4.5 million in proxy delivery fees or 0.05% of the $8.47B McDonald’s net income. As a result, Broadridge enjoys high switching costs, as highlighted by the 98% client retention rate.

(Source: Company investor day)

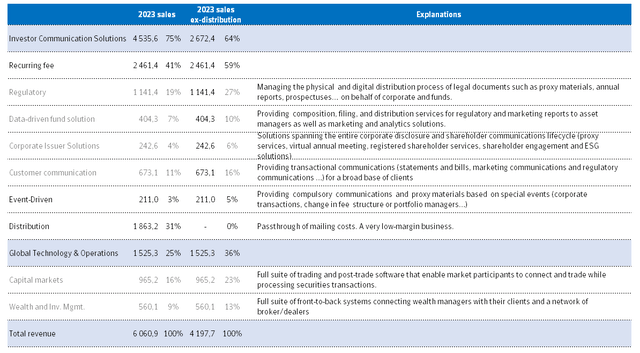

Investor Communication Solutions (64% of sales ex-distribution revenue and ~80% pre-tax income)

Broadridge mainly provides communication solutions to banks, brokers and asset managers while also servicing a variety of clients active in different sectors (utilities, health care, telecom…). It connects >1k banks and brokers, >30k mutual funds and ETFs, >10k corporate issuers with >150k institutional investors and >200m retail shareholders to make sure that information is sent, and client instructions are perfectly executed.

Given distribution revenue is a passthrough of mailing costs, we prefer to remove it from the business split. From our understanding, it is a very low-margin business because Broadridge is able to charge retail rates while it pays the wholesale rate for mailings in its regulatory business. However, in the more competitive customer communication business, it is simply a pass-through of mailing costs.

(Source: Company annual report and Author)

Regulatory solutions (27% of sales ex-distribution revenue) are Broadridge’s crown jewel and the largest segments within ICS. Corporate issuers and mutual funds must provide proxy voting and shareholder reports (prospectuses, annual and semi-annual reports…) to beneficiary owners (shareholders and fund investors). While most shares (roughly 70/80% of all US stocks) are held in street name, the participating banks/brokers are required to ensure delivery of proxy materials to individual beneficial owners. By law, issuers (corporate) must reimburse brokers for the costs of forwarding proxy materials, and these fees are set forth by the Proxy Voting Review Committee (overseen by the SEC). Banks and brokers generally outsource this service to Broadridge while corporate pay for this service. Thus, Broadridge handles the entire proxy materials distribution, via both physical and electronic delivery (e.g.: Proxy Edge is an electronic proxy delivery and voting solution), as well as the entire voting process (paper, phone, online) for bank/brokers and fund clients.

Broadridge essentially has a legal monopoly providing this service, processing 70%/80% of all US shares (processing almost 100% of shares held in street name), with no material competition. This business is resilient, as it is a regulatory obligation for brokers and advisors to distribute proxy materials and legal documents.

Event-driven (5% of sales ex-distribution revenue). Revenues from event-driven activities are driven by the volume of special events and corporate transactions that Broadridge handles. It includes corporate transactions such as proxy battles, acquisitions, mergers and spin-offs… as well as extraordinary events related to mutual funds such as a change in directors, fee structures, investment restrictions, and mergers of funds…

Event-driven activity tends to be often highly repeatable, though they might not necessarily happen every year. We view this business like the regulatory solutions, even though slightly more volatile. In short, one third of group sales are derived from the highly attractive regulatory franchise.

The investor communication segment is not only about voting. It also includes services that help their clients better communicate with investors, such as the distribution of marketing, regulatory and transaction information.

Customer Communications Solutions (16% of sales ex-distribution revenue). Broadridge provides solutions that support the sending of transactional (statements and bills), marketing and regulatory communications (trade confirmations and explanation of benefits) across several channels (print, digital, email, SMS…) of a broad base of clients, including financial services, healthcare, insurance, consumer finance, telecommunications, utilities… It also offers analytics, enabling clients to improve communications and client engagement.

Data-driven fund solutions (10% of sales ex-distribution revenue) allow asset managers to efficiently and reliably communicate with investors by consolidating all investor communications into one single platform. These services include the creation, printing, filing, and distribution of regulatory reports and prospectuses while being fully compliant with existing regulations (MIFID II, Solvency II…). In addition, it provides marketing communication solutions along with data and analytics tools, including fund distribution data and research reports, to help asset management firms optimize their fund distribution. Finally, it also provides custody services for retirement plans.

Corporate Issuer Solutions (6% of sales ex-distribution revenue) provide corporate solutions spanning the entire corporate disclosure and shareholder communications lifecycle such as virtual shareholder meeting (including shareholder voting services and management/shareholder interactions…), shareholder engagement solutions (data and analytics, shareholder delivery preferences, voting trends…) and ESG consulting (control, develop and promote ESG strategies). It also provides compliance and transactional reporting services for public companies (SEC filing services for both regulatory reporting and capital markets transactions) and services for registered shareholders (dividend payments, sending documentations…)

Global Technology and Operations (36% of sales ex-distribution revenue and ~20% pre-tax income)

Broadridge provides a scalable and customizable software solution that automates the entire front-to-back transaction lifecycle for equities, mutual funds, fixed income, foreign exchange, and exchange-traded derivatives. This includes everything from order capture and execution to trade confirmation, cash management, clearing and settlement, reconciliations, compliance and portfolio accounting.

Capital markets (23% of sales ex-distribution revenue)

Broadridge offers a suite of trading and post-trade systems that enable market participants to trade and process securities. The company processes $10 trillion per day in equity and fixed income trades and works with 20 out of 24 US fixed income primary dealers and 7 out of the 10 largest global IB trading equity securities.

Wealth and Investment managements (13% of sales ex-distribution revenue)

Broadridge offers front-to-back systems that facilitate trade execution, as well as post-trade matching and confirmation. It also offers portfolio and order management solutions such as account management, trading, compliance, portfolio construction, risk and analytics. Besides, Broadridge collaborates with Accenture to offer business process outsourcing services. These services combine Broadridge’s technology with Accenture’s operational expertise and global presence to support the entire trade lifecycle, encompassing securities settlement, reconciliations, accounting and billing… The company counts 14 out of the 15 largest US wealth managers as clients.

Growth opportunities

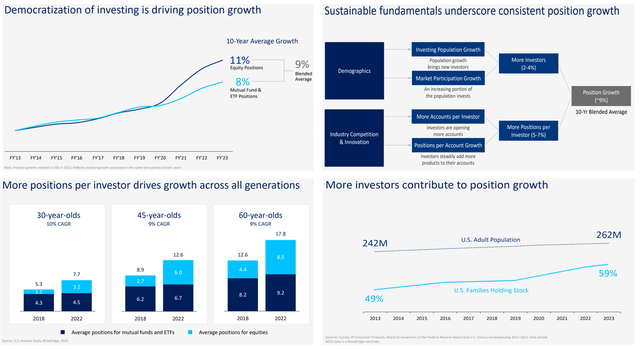

Roughly half of the Investor Communication Solutions segment is driven by the growth in the number of equity, mutual fund and ETF positions, which is the result of the growth in the number of investors and the number of holdings per investor.

The latter benefits from an aging population as investors tend to own more positions as they get older, as well as product innovation and the rise of passive indexing strategies. The former benefits from population growth and an increasing market participation rate. Market participation has increased over the last decade in the US, as highlighted by the percentage of US families holding stocks, increasing from 49% in 2013 to 59% in 2023. Such evolution is supported by the democratization of investing, which is driven by lower fees, a broader access to financial markets (especially thanks to mobile apps, no-commission brokerage accounts…) and product innovations (fractional shares…).

(Source: Company Capital Market Day)

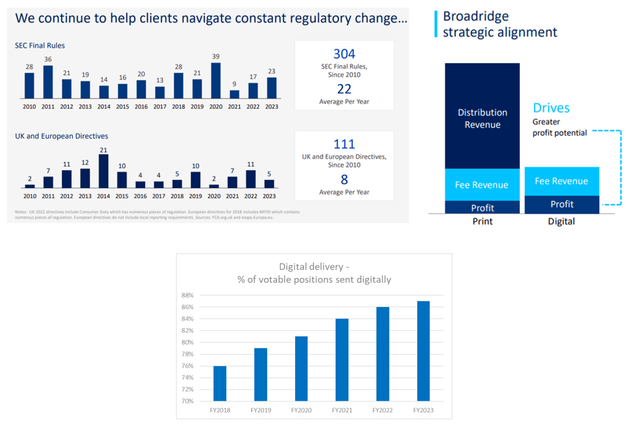

The remaining of the ICS segment will benefit from regulatory changes as well as an increasing focus on transparency and additional disclosures. Indeed, Broadridge will be able to help corporate to constantly comply with new regulations while communicating with clients.

(Source: Company Capital Market day)

Finally, the higher share of digital communications will continue to support margin improvement and profit growth. Whereas 85%/90% of regulated communications (proxies and interims) are digital, there are still tremendous opportunities among bills and statements because most of them are still delivered under paper format.

The GTO business will benefit from the need of financial institutions to simplify and automate complex and manual operations, as well as their willingness to consolidate software providers. Besides, additional regulatory changes such as T+1 settlement further complicate operations and can push companies to outsource (vs implementing modifications in their own systems).

Back in 2018, Broadridge signed an agreement with UBS to develop a fully integrated front-to back wealth management platform. The idea is to share the costs of services such regulatory compliance to all users, making the platform cheaper as more companies connect to it. The platform is now live at UBS (first revenue have been recognized since Q1 FY24), enabling Broadridge to fully focus on bringing this transformational solution to new clients with a goal of driving $20/$30 million of annualized sales. As a reminder, UBS should bring about $75 million of revenue per year.

Financials

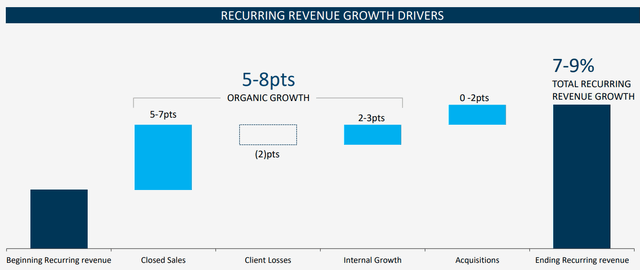

Recurring revenue, equivalent to total revenue less event-driven and distribution revenue, is expected to grow by 5%-8% organically between FY24 and FY26. Total recurring revenue growth at constant currency is expected to reach 7%/9% thanks to acquisitions.

(Source: Company Capital Market Day)

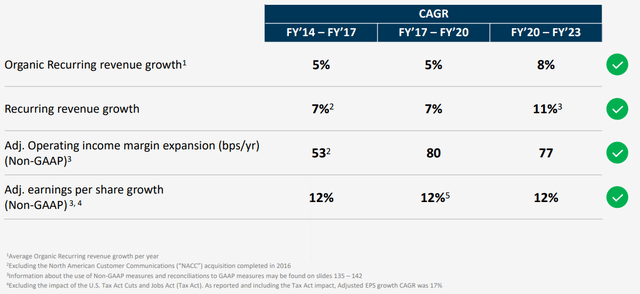

Given the previously mentioned growth drivers, a 6% average recurring revenue growth rate over the last decade, customer stickiness and a solid track-record, we are highly confident in the company’s ability to at least meet the low-end of its target.

(Source: Company Capital Market Day)

Given the company delivered an average of 80 bps annual margin expansion over the last decade, we are also confident that it can reach its target of an annual adj. EBIT margin improvement of 50+ bps going forward. Such improvement is mainly the result of positive operating leverage, a better product mix (more digital distribution) and some efficiency programs. As a result, operating income can grow ~8%/9%.

(Source: Company Capital Market Day)

Broadridge should generate $1+bn FCF, of which~ 50% should be returned to shareholders over time. The company will return more to shareholders if they do not find attractive M&A targets. For instance, it aims to give back $700/800 million to shareholders in FY24 (including $350/450 million of share repurchases). Given that dividends should represent $350 million, share repurchases should reach $150+ million in a normalized year, adding 2/3 percentage points to EPS growth. Therefore, EPS growth can reach 10%/12% annually over the next few years.

Valuation

The stock is trading at 24.5x its EPS, whereas the broad equity index is trading at 20.4x. This is equivalent to a 20% valuation premium, above its 10% long-term average. Broadridge is a high-quality compounder with a resilient and asset-light business model that deserves to trade at premium valuations. However, we consider this valuation level as not attractive. While we like the company and its 10% EPS growth profile, we prefer to hold the stock for the moment.

Risks

Regulatory changes, especially changes related to the pricing of services, could negatively impact the business.

Sector consolidation could lead to the loss of clients. The E-trade acquisition by Morgan Stanley is a good example. E-Trade was a client of Broadridge’s, but Morgan Stanley was not. MS decided to transition E-Trade to its in-house platform.

Client concentration: The largest client accounts for 7% of consolidated revenues.

Data breach: Broadridge has access to sensitive information and could potentially be the victim of a cyber-attack.

A reduction in the number of companies listed and/or in the number of stocks owned by investors would negatively impact the business performance

Read the full article here