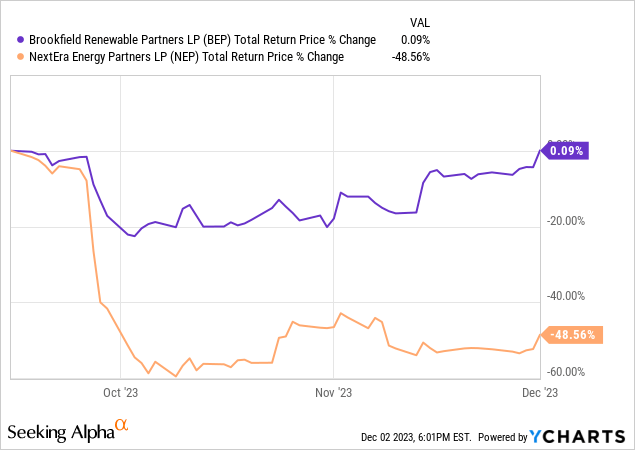

On our last coverage of Brookfield Renewable Partners L.P. (NYSE:BEP)(NYSE:BEPC), we suggested that BEP was the superior choice relative to NextEra Energy Partners, LP (NEP) and investors would do well to look to it versus NEP in trying to seek yield.

If you want to chase the 12-15% distribution growth dream, we really cannot stop you. But we think that distribution growth is not going to come. If 12-15% growth rates alongside paying out every last cent of CAFD as distributions was easy to do, even the parent NextEra Energy (NEE) would be doing it. BEP is the better and safer option and this is the first time, since we started its coverage, that we are actually slapping a buy rating on it.

Source: NextEra Energy Partners & 3 Reasons We Prefer Brookfield Renewable

While it has not been fun being an investor in either of these two, we can get a modicum of happiness in the end result since that article came out.

BEP remains a solid option for income-seeking investors and the valuation multiple has compressed over time, giving you an edge in making money. This is still not a very easy setup (though arguably it got there at the lows where we added a little). We estimate that you could get about 9% total returns from here and possibly 10%-11% using covered calls. But today we are about to talk about another opportunity from BEP, one that involves one of its preferred shares. Do note that this is primarily for Canadians or at least those comfortable trading on TSX.

Credit Watch

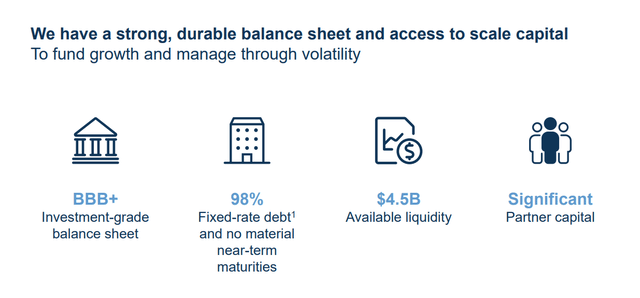

BEP has a strong balance sheet with investment grade ratings from multiple agencies.

BEP Presentation

Fitch was the latest to affirm the credit rating with the latest report coming out on December 1, 2023. Key points for us were as follows.

BEP’s proportionate long-term average generation has become more diversified, shifting from 82% hydro in 2017 to 65% hydro as of Sept. 30, 2023, with wind, solar, distributed generation and storage comprising the balance. The company’s recently completed acquisition of WEC will add additional diversity, albeit modest, in the form of infrastructure services for nuclear power generation – a carbon free source of electricity.

Approximately 90% of the company’s debt is non-recourse, long-duration fixed-rate project debt with an average remaining maturity of over 12 years. Over the last several years, holdco-only FFO leverage has exceeded 4x primarily due to partial-year contribution from acquisitions and new projects. If calculated on an annual run-rate basis, holdco-only FFO leverage would have been below 4x for the same period. Fitch estimates that BEP’s holdco-only FFO leverage will average 3.9x in the next four years.

Source: Fitch

The very high levels of non-recourse debt are what makes this extra special from a credit standpoint. It creates a unique setup where the company is officially rated as BBB+, but the real risk is far lower than even that.

Preferred Shares On TSX

BEP has three types of preferred shares listed on the TSX.

1) Perpetual preferred shares which pay a fixed rate on par.

2) 5-year reset preferred shares, which reset every 5 years based on Government of Canada bond yields

3) 5-year reset preferred shares, which reset every 5 years based on Government of Canada bond yields but also have a minimum rate feature.

Over the past few months, we have highlighted several opportunities in these types of preferred shares from different Canadian companies. For example, we recently highlighted Pembina Pipeline’s (PBA), Pembina Pipeline Corporation PFD 5 YR CL A 1 (TSX:PPL.PR.A:CA). Those fell in the second category above. From BEP’s preferred share suite, there is one that really stands out on the TSX and it comes from the first category.

Brookfield Renewable Partners L.P. Class A Preferred Limited Partnership Units Series 18 (TSX:BEP.PR.R:CA)

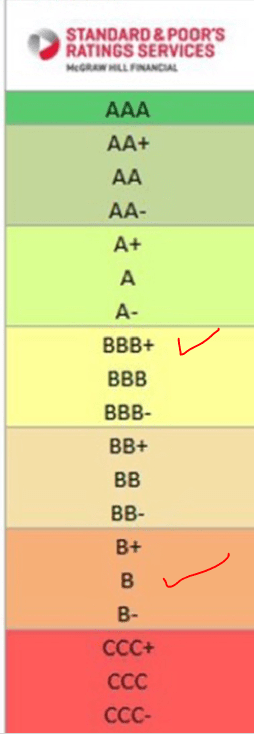

There are quite a lot of ways to look at this fixed rate preferred share setting. The first being that you are getting a stripped yield of 8.36% at the current price of CAD16.60. This comes from the 5.5% coupon on par and that translates into the current stripped yield, after accounting for the accumulated dividends from the last payment. On the Canadian side, for fixed rate preferreds, there is only one that has a higher yield on TSX. Bombardier Inc. 6.25% Series 4 Cumulative Redeemable Preferred Shares (BBD.PR.C:CA). That one yields 8.92%. Of course, Bombardier is rated B on S&P scale and BEP is rated BBB+. You can see the gap below.

S&P

So what is a good comparative on the Canadian side? Well, in our view, Enbridge Inc. (ENB) (ENB:CA) fits the bill. ENB has a BBB+ credit rating and a similar low-risk profile. Enbridge Inc. PFD SER A 5.5% (ENB.PR.A:CA) is the only perpetual preferred from ENB and that has a current yield of 6.82%. Another comparative would be Emera Incorporated Cumulative Redeemable First Preferred Shares Series L (EMA.PR.L:CA). This is a perpetual preferred from Emera Inc. (OTCPK:EMRAF). While it is a utility, it has been struggling with its credit metrics. It is currently rated BBB (none below BEP) by S&P with the negative watch. The perpetual preferreds listed above yield 6.85%. So BEP.PR.R’s advantage here is clear.

BEP.PR.R also comes ahead of the other two TSX-listed perpetual preferreds from BEP. Both Brookfield Renewable Power Preferred Equity Inc. Class A Preference Shares Series 5 (BRF.PR.E:CA) and Brookfield Renewable Power Preferred Equity Inc. Class A Preference Shares Series 6 (BRF.PR.F:CA) yield under 8%.

Verdict

There is a reason we are stressing BEP.PR.R’s yield, rather than focusing on the US-listed preferreds and subordinated debt. While there are some perks on the US side, BEP.PR.R’s yield is really high relative to Canadian comparatives and the risk-free rates there. We also think that whatever the outcome for interest rates in this cycle, Canada is likely to peak rates at a shallower level relative to the US. The reason is that while the bulk of US mortgages are at fixed rates for 30 years, most of Canada is tied to mortgages that reset every 5 years. That, coupled with a far larger housing bubble, means that Canadian tolerance for higher rates will be definitely lower than what we will see in the US. We like BEP.PR.R and have accumulated a large position recently.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here