Written by Nick Ackerman, co-produced by Stanford Chemist

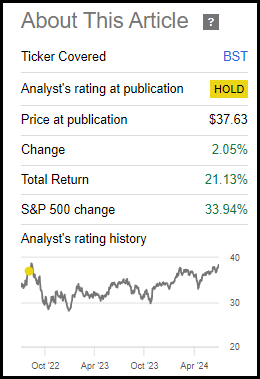

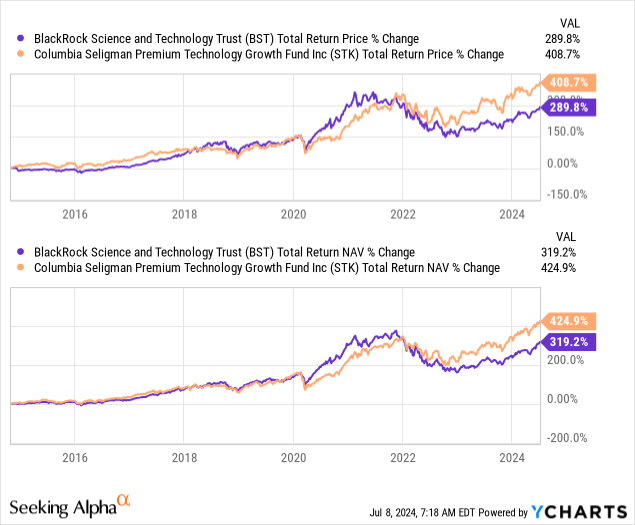

It has been quite some time since I’ve provided an update on the BlackRock Science and Technology Trust (NYSE:BST). It has been going back nearly two years now, and since that time, the fund has performed quite well. However, the fund did underperform the S&P 500 Index through this period as well on a total return basis.

BST Performance Since Prior Update (Seeking Alpha)

At that time, we were also touching on BlackRock Science and Technology Term Trust (BSTZ), its more speculative tech sister fund with a greater emphasis on smaller companies and private investments. Today, BSTZ still remains an interesting speculative position that we wrote about more recently.

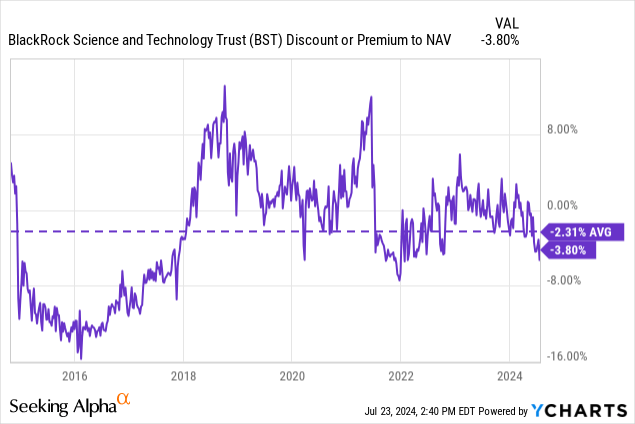

While BST’s discount has started to open up a bit more recently, I believe the fund still remains a ‘Hold,’ or alternatively, one could consider utilizing a dollar-cost average approach as a more conservative means to build up a position. I believe that seems fairly prudent, given the broader market has also been hitting new all-time highs rather regularly.

BST Basics

- 1-Year Z-score: -1.83

- Discount/Premium: -3.81%

- Distribution Yield: 8.29%

- Expense Ratio: 1.09%

- Leverage: N/A

- Managed Assets: $1.381 billion

- Structure: Perpetual

BST’s investment objective is “providing income and total return through a combination of current income, current gains and long-term capital appreciation.” They will attempt to do this through investing “at least 80% of its total assets in equity securities issued by U.S. and non-U.S. science and technology companies in any market capitalization range, selected for their rapid and sustainable growth potential from the development, advancement and use of science and/or technology, and/or potential to generate current income from advantageous dividend yields.”

Further, they will “employ a strategy of writing covered call options on a portion of the common stocks in its portfolio.” The fund’s latest overwritten percentage was at 33.52%.

Performance Comparisons

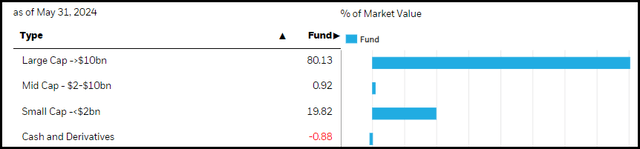

BST is a fund mostly focused on the mega-cap tech names, those that have been leading the broader equity market higher for the most part. To reflect that, we can see that the average market cap for a holding in BST is $1.319 trillion.

That can be compared to BSTZ’s average market cap holding at $404.75 billion, which is still quite massive but helps to provide some context. Companies are just much larger these days, and when you hold something like NVIDIA (NVDA), as both do as their largest holdings, that can really skew the average market cap higher.

Regardless, one of the problems that BST had was that prior to the Covid pandemic, the fund was more focused on the large-cap area, but after, they actually started shifting their portfolio more toward what BSTZ was investing in. The relatively smaller companies and private investments. As noted in their brief description of the investment policy, they aren’t restricted by market cap, so they had the flexibility to do that.

Looking back at the early 2020 holdings, BST had less than 10% of its portfolio in small-cap investments. More recently, that’s up to nearly 20% now.

BST Market Cap Allocation (BlackRock)

A further reflection of the portfolio transformation was that private investments, most recently as of the end of 2023, came in at 21.2% of the fund. At the end of 2019, private investments were less than 8% of the fund.

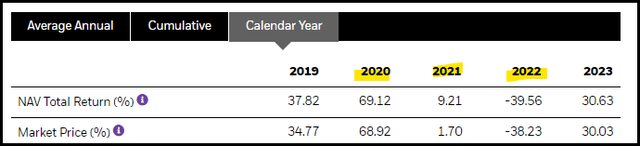

Shifting their portfolio initially worked out incredibly well; the fund was soaring through 2020 and initially put up respectable results in 2021. That said, we know in hindsight what happened with those speculative no-profit companies—just as fast as most of them rose, they dropped in 2022.

BST Annual Returns (BlackRock (highlights from author))

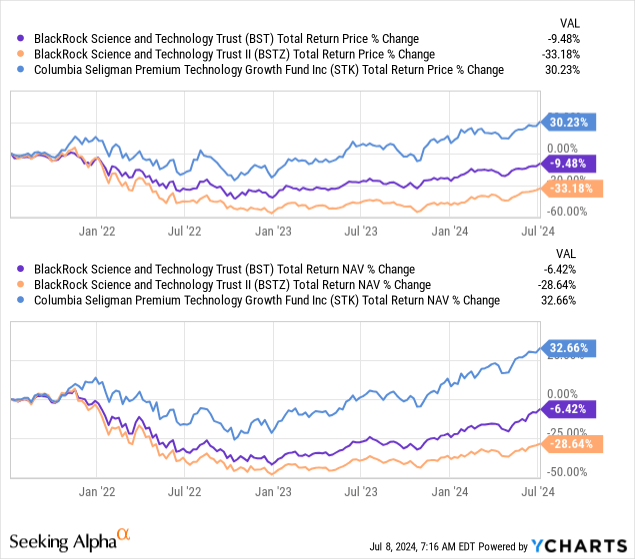

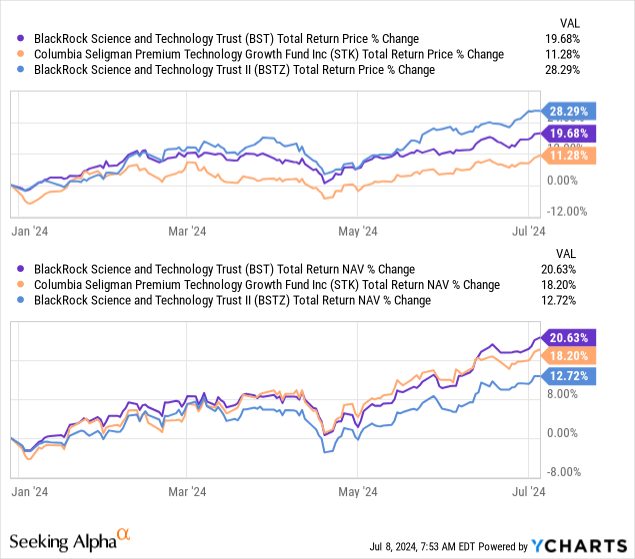

This also brings up a great comparison between the other call-writing tech-focused fund, the Columbia Seligman Premium Technology Growth Fund (STK). STK seemed to have stuck to their strategy, and it also helps that they’ve been more invested in semiconductors, too. That has seen their performance eclipse that of both BST and BSTZ over the last few years now by a massive margin.

In fact, even on a total return basis accounting for the distributions through these last three years, BSTZ has seen a massive decline and BST saw some losses as well.

Ycharts

While covered calls can cap upside potential by having positions called or way or producing losses to close out a covered call position, that certainly wasn’t too much of a problem for STK during the last three years. That fund was still able to put up attractive total return performance.

Prior to this last few years, it was BST outperforming during 2020 and 2021 thanks to its positioning. Then, even further back, prior to the Covid crash, these funds were actually pretty well correlated and could have even been used as potential swap partners.

Ycharts

I believe that BST is still worth holding here but given the only shallow discount currently, I wouldn’t be buying aggressively. That’s even though it has slipped slightly below its long-term average discount.

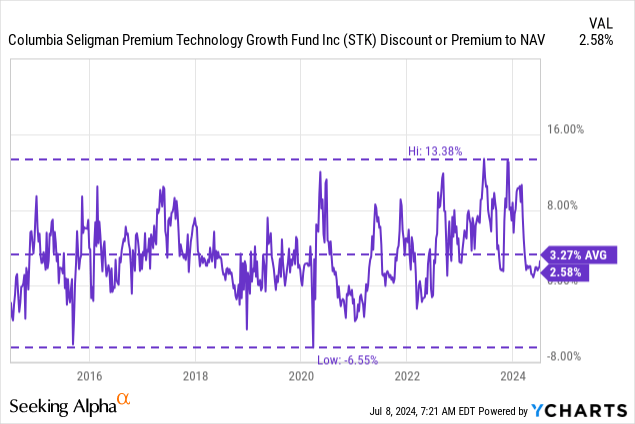

For what it’s worth, STK is also trading at a slight premium but is similarly valued on a relative basis. That would be due to that fund regularly commanding a premium or trading very near its NAV per share.

Ycharts

BST is one of a number of BlackRock funds that have adopted a “discount management program.” However, with that shallow discount, it won’t be participating in the tender offer based on the first measurement period, showing an average discount of -2.11% during the period. It would need an average discount of -7.50%, and then it would trigger a 2.5% tender offer at 98% of NAV.

Distribution – ‘Squeezing A Dividend’ From Tech

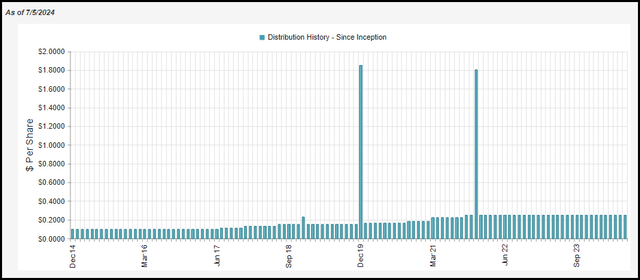

With a covered call strategy comes the potential for capping some upside; however, it also comes with being able to ‘squeeze a dividend’ out of a heavy tech portfolio. Unlike BSTZ, BST has still been able to manage a steady distribution to investors. The latest NAV distribution rate comes to what appears to be a sustainable 7.85%. Thanks to the slight discount, the distribution yield for investors is a bit better at 8.29%.

BST Distribution History (CEFConnect)

Of course, we know that what they are paying isn’t a dividend because it is coming from capital gains, as it receives very little in the way of income due to no or low-yielding underlying investments. Therefore, to use the correct terminology, we are getting a distribution.

In fact, the entire distribution will need to be funded through capital gains as the fund only produces net investment losses—meaning that after accounting for expenses from total investment income, we arrive at a negative figure. Those capital gains are going to need to be derived from the underlying portfolio or the writing options strategy.

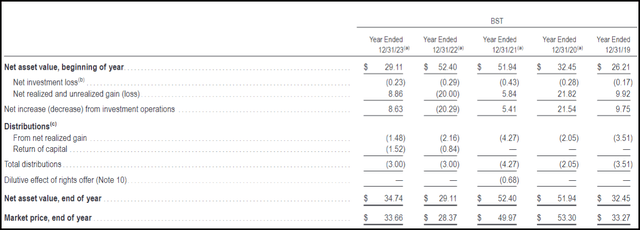

BST Financial Highlights (BlackRock)

This isn’t unusual for a tech-focused closed-end fund at all. As another example, we can look back at STK, which also only has net investment losses.

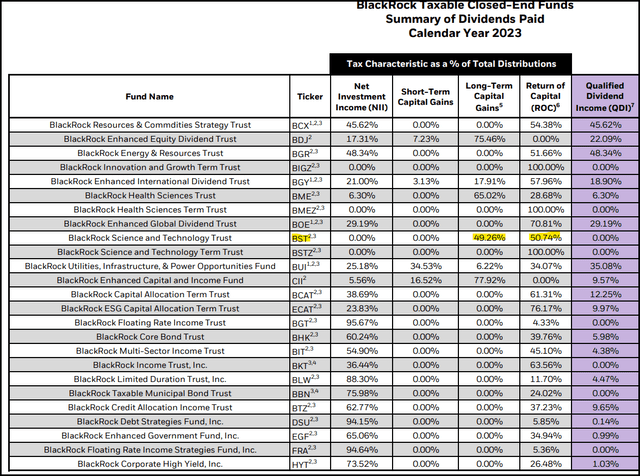

For tax purposes, in 2023, about half of the distribution was return of capital.

Distribution Tax Classifications (BlackRock (highlight from author))

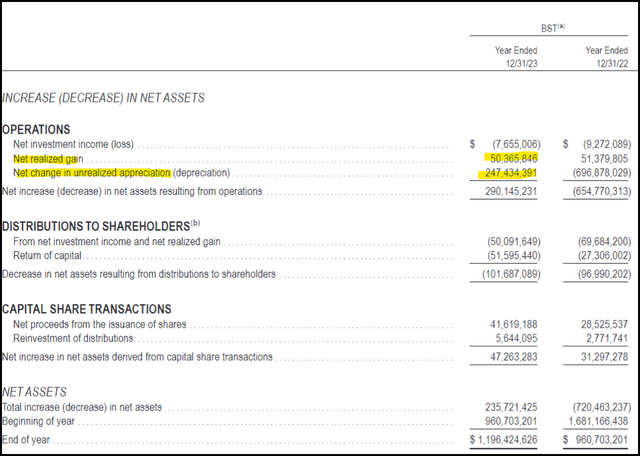

One might note that NAV actually rose in 2023 and performed quite well, meaning this wasn’t ‘destructive’ ROC. This can happen because of capital loss carryforwards in prior years or, as is the case for BST, they just left most of these gains as unrealized for the year.

BST Annual Report (BlackRock (highlights from author))

BST’s Portfolio

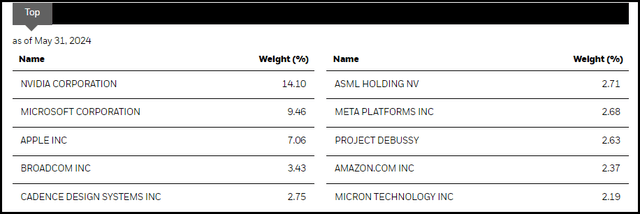

We already discussed some of the points of the fund’s portfolio above, but we can take a quick look at the fund’s latest top ten holdings. NVDA has become the fund’s largest holding by far, and I suspect a lot of that has to do with the sheer outperformance of the name.

BST Top Ten Holdings (BlackRock)

On the other hand, we also still see meaningful exposure to the other mega-cap tech names here of the Super Six. That includes Microsoft (MSFT), Apple (AAPL), Meta Platforms (META) and Amazon (AMZN).

The only name missing here would be Alphabet (GOOG)(GOOGL). However, GOOG was a position in this fund at the end of 2023 and at the end of March 2024, according to the latest N-PORT filing. I suspect it is still a holding in the fund, but it has merely stayed at a relatively smaller weight, which has meant not being able to break into the top ten.

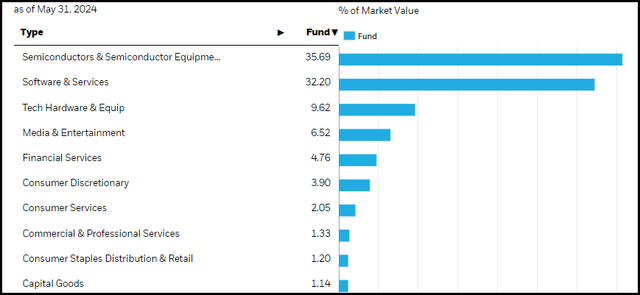

Between NVDA, Broadcom (AVGO), ASML Holding N.V. (ASML) and Micron Technology (MU), the semiconductor sector has been representing a larger portion of the fund’s portfolio these days. That’s up materially from the 28.2% weight at the end of 2023 and the 22.1% weight at the end of 2022.

BST Sector Allocation (BlackRock)

Again, I believe being underweight in the semiconductor space and shifting its portfolio more toward smaller and private investments meant a relatively weaker performance against its peer STK. At the end of 2022, STK had 36.4% of its portfolio weighted in semiconductor equipment and semiconductor companies. With closer allocations, these funds could start to perform more similarly as they had once done. At least on a YTD total NAV return basis, they’ve been much closer.

Ycharts

Still, they have notable differences that I believe could still make sense to argue one over another. Or, I’d say there is even an argument to be made that holding both funds as complements to each other can make sense.

One final note on the fund’s top holdings would be that we see Project Debussy. That’s reflecting one of the fund’s private investments, which is actually the name for Databricks. With just over 21% of the fund’s holdings listed as level 3 investments, there are more private investments under the surface of the top ten.

That also generally comes with some skepticism in terms of the valuation. It can often lead to relatively larger discounts for closed-end funds, but that hasn’t seemed to be the case for BST so much. The values are assigned by a third party on an as-needed basis, so they should be fairly accurate. However, something is only worth what someone is willing to pay for it. That is, it might make sense through a valuation technique perspective, but it is still only a best guess. Until it is actually sold or the company does an IPO and hits the public market, that’s when the true value can be determined.

With that said, that could be one of the potential upside catalysts for BST (as well as BSTZ.) If the IPO market starts heating up again, we could see a number of their private holdings hit the public market. That can sometimes result in a huge pop for the shares and a way to trim positions at a much higher valuation—even if, further down the road, the company’s shares don’t do much. However, it remains a waiting game on the IPO front, or it is always quite possible we may never see the type of IPO boom we saw in 2021 again.

Conclusion

BST remains an interesting prospect as a tech-heavy fund with a slice of private investments as well. The fund provides investors with regular monthly distributions out of an area of the market that doesn’t generally produce generous payouts. With a relatively shallow discount and markets hitting new all-time highs rather regularly, it doesn’t appear to be a screaming buy today. That said, for a long-term investor, implementing a dollar-cost average approach could be appealing.

Read the full article here