Investment Thesis

Build-A-Bear Workshop (NYSE:BBW), the specialty retail company that offers a unique experience allowing customers to create their own customized stuffed animals, last week delivered an unappetizing outlook for its all-important holiday season.

The bearish argument here is that BBW witnessed some unexpected softness that forced it to reduce its revenue growth rates for fiscal 2023.

On a more positive matter, I argue that not only the stock is cheaply valued, but also that the business has no debt and has a history of returning excess cash to shareholders.

In fact I postulate that BBW could end up announcing a special dividend early in fiscal 2024, given that it has more cash on its balance sheet than necessary.

On balance, I’m bullish on BBW.

Rapid Recap

Back in September, I wrote a bullish analysis on BBW where I said,

BBW’s financials aren’t the most alluring, particularly for investors who are looking for something somewhat more racy. However, oftentimes, the most attractive investments are not necessarily the ones with the best story.

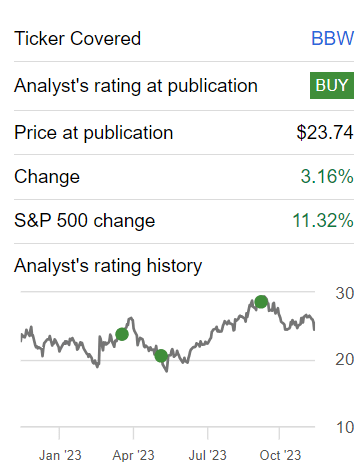

In fact, it should be noted that I’ve been bullish on BBW during 2023, as you can see below.

Michael Wiggins De Oliveira on BBW

And yet, as you can see despite the stock being cheaply valued it has underperformed the S&P500 (SPY). Nonetheless, I remain resolute, that the stock is an attractive investment for investors who don’t want to have to chase ”yet another AI story stock”.

Build-A-Bear Workshop’s Near-Term Prospects

Build-A-Bear’s near-term prospects appear promising despite some recent challenges. The company has demonstrated resilience and adaptability, reporting strong results for the third quarter of 2023 and showcasing record-breaking revenues.

During the earnings call, BBW highlighted the effectiveness of its strategic initiatives. These include the evolution and expansion of their footprint, and a comprehensive digital transformation.

Furthermore, BBW’s digital transformation is a key driver of its near-term prospects. The company has strategically invested in upgrading its business systems, integrating its website, CRM, and loyalty programs, and rolling out a new Point of Sale system. This digital evolution aims to enhance business efficiency, increase consumer engagement, and create incremental opportunities for gifting and personalization, ultimately boosting lifetime customer value.

Additionally, Build-A-Bear’s foray into content and product innovation, tapping into trends like “kidulting,” and initiatives such as launching an animated theatrical film, “Glisten and the Merry Mission,” contribute to expanding consumer engagement.

However, despite these positive prospects, Build-A-Bear faces some challenges in the near term. The company experienced some softness impacting its guidance for the fiscal year (more on this soon).

The disruption caused by a new platform implementation affected its web business, challenging the company’s digital operations. While the overall trend has shown signs of improvement as the company enters December, mitigating these challenges and regaining momentum in a competitive landscape remain crucial.

Revenue Growth Rates Are Moderate

BBW revenue growth rates

Now, let me get to the crux of the bearish argument. BBW reduced its fiscal 2023 revenue growth rate outlook by 2%. Needless to say, the market didn’t look upon this negative revision too kindly, and the stock retraced some of the gains it had made in 2023.

Simply put, this is categorically a slow-growth business. That being said, it’s important to consider this in the context of the comparables with the prior year.

Last year’s comparables were strong, therefore, naturally, this year’s growth rates were always going to be less impressive in comparison.

That being said, this doesn’t detract from the fact that previously BBW’s management was guiding to deliver about 7% CAGR at the high end in fiscal 2023 and now this figure has been downwards revised to 5% CAGR.

This difference may not seem significant, but if we think about the fact that BBW is a highly seasonal business with Q4 typically being a strong period, the fact that BBW downwards revised its guidance for its upcoming all important holiday period, has weighed on investors’ sentiment for this stock.

And whilst I recognize that element, I argue that BBW’s stock is cheap enough to compensate investors for its lackluster growth prospects already.

BBW Stock Valuation — 5x This Year’s Operating Income, Plus +10% Combined Return

If we take the midpoint of BBW’s fiscal 2023 pretax income guidance of 7% y/y growth, this would see BBW deliver about $67 million of pretax income.

On the surface, this leaves the stock priced at 5x this operating income. That’s undoubtedly a very attractive valuation.

But the bull case doesn’t end there. Why? Because BBW is eager to return excess cash to shareholders. Case in point, throughout the first 9 months of fiscal 2023, BBW returned to shareholders $37 million via share repurchases and dividends.

On this matter, note what I previously said about BBW,

[…] over the past seven quarters, BBW has distributed special dividends and repurchased more than one million shares, amounting to $81 million returned to shareholders, or just over 20% of its market cap. It’s not unimaginable that BBW could embrace a similar strategy over the next 7 quarters.

I stand by that assertion, once BBW has gotten over the holiday season, I wouldn’t be at all surprised to see BBW announce yet another ”special dividend” early in fiscal 2024. After all, BBW will probably end fiscal 2023 with more than $30 million of cash on its balance sheet and no debt.

The Bottom Line

In summary, despite recent challenges and a revised revenue growth outlook for fiscal 2023, my bullish stance on Build-A-Bear Workshop remains steadfast. The company has showcased resilience and adaptability, reporting strong third-quarter results and record-breaking revenues. Strategic initiatives, such as a comprehensive digital transformation and expansion into content and product innovation, position BBW for promising near-term prospects.

A key factor bolstering my positive outlook is the compelling valuation of BBW’s stock, currently priced at 5x this year’s operating income. This attractive valuation, coupled with the company’s history of returning excess cash to shareholders, including the possibility of a special dividend in fiscal 2024, adds to its investment appeal. Despite challenges in the digital space and a moderated growth outlook, BBW’s low valuation and strategic initiatives contribute to its attractiveness as an investment opportunity.

Read the full article here