Pet Valu Holdings Ltd. (OTCPK:PTVLF, TSX:PET:CA, “PET”) is Canada’s largest operator of pet stores, with a large and profitable footprint throughout the country. The company has a dominant position, allowing for significant benefits from scale and allows strong operating margins. Pet ownership is at record levels, and millennials are spending significantly more than past generations on them.

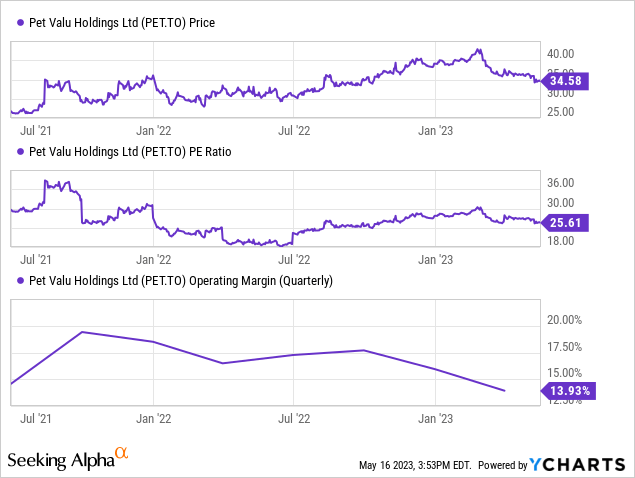

PET stock has come off its highs recently, making the shares worth another look as the company continues to execute at a high level. Also, all indications are Canadians continue to be willing to spend on their furry friends, especially compared to other discretionary items. The company should be a solid dividend grower over time, with good margins and sales expansion providing cash flow to pay more over time. The first quarter results released this week continued this trend of good performance without a positive share reaction.

| Q1 2022 | Q2 2022 | Q3 2022 | Q4 2022 | Q1 2023 | |

| Quarterly Revenue | $213.3 M | $227.7 M | $244.7 M | $266.0 M | $250.3 M |

| Same Store Sales (%) | 22.8% | 21.2% | 14.7% | 11.8% | 9.4% |

First quarter margins compressed

The first quarter results showed continued strength, especially when considering the company lapped an extremely strong same store sales (SSS) in Q1 of 2022. That was the period right after pandemic reopening in Canada where sales growth peaked with 9.4% increase over that being quite strong. Revenue growth was 16.1% without the impact of acquisitions as the company continues to add stores at a good pace as well, with 751 stores up from 705 in 2022 Q1. While this is down significantly over the past year, the growth is still solid for a company trading at 24x trailing earnings. The company continues to pay a solid dividend of $0.40 per year or 1.1% yield, giving you a bit of a bonus while you wait for growth to materialize.

Over the past 7 years the company has managed an impressive 12% of same store sales growth showing even with a slower cadence of openings the stock can grow a mid-teens CAGR. Margins have been hurt issues in the supply chain and by the strength in the U.S. dollar against last year. At 34.8% it has been a drag on net income, but with a long term 36/37% average margins should rebound once the short term issues subside. The U.S. dollar is continuing to perform well against the Canadian dollar, which is a headwind to margin expansion short term but will even out over time from here.

Also, the company greatly expanded the store network early last year by 66 when it acquired Chico to expand in Quebec. That has been a small drag on margins as well, but over time as PET adds its house brands it will improve the margins from those stores. This led to an adjusted net income $23m of 9.2% for Q1 against a larger 11.6% in 2022 – with expenses like interest expense increases also pressuring that number in 2023. Over time these are issues that will solve themselves with reductions in interest rates and improvements in efficiency Outside of continuing strong results and a lower price recently, the defensive characteristics make it interesting to add for the next few years.

May Presentation Pet Valu (Pet Valu IR)

Valuation and Defensive

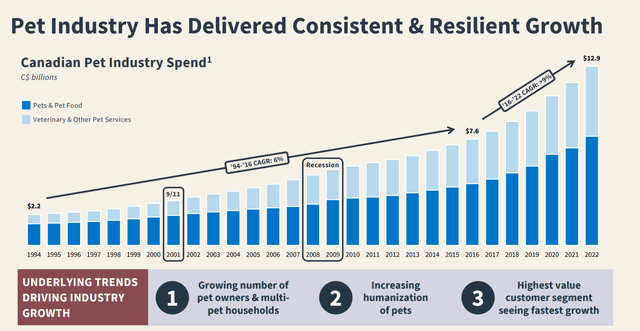

PET has seen its valuation come down from 30x earnings at points in late 2021 and early 2023 to a more reasonable trading range in the low 20s in May 2023. The stock rebounded strongly from this valuation in 2022, as the market has come to appreciate that animal spending is more staple in nature to many people than discretionary. Pet food is non-negotiable, and many people are going to choose pet items over their own luxuries. In previous recessionary periods such as 2008, the pet industry actually grew by over 5% in sales bucking the wider trend. It also significantly outperformed during the Covid-19 period with people spending more on animal products than would be expected.

As you can see above, even ignoring the recent explosion in money supply, the industry has grown more than 6% per year including through recessions. The past 7 years the growth has been even greater and shown no signs of abating, as millennials make up a larger portion of pet consumers. That demographic is more likely to spend significantly on pet care and many people are choosing pets over children for cost reasons. This also means people are more likely than ever to own multiple pets and services catering to pets have greatly increased in popularity. These tailwinds should continue for the next 10-20 years while this generation grows into middle age.

Buy rated

Like many who are looking for a combination of defensive characteristics and growth, Pet Valu Holdings Ltd. is a solid buy in this environment. The stock has performed well overall since January 2022, with only a small drawdown as a growth name. The recent 21% pullback from 43 to 34 gives long term investors a chance to buy at 25x Trailing earnings and just 21x forward earnings. While this multiple is still higher than the 19x of the wider U.S. market, the company has a good runway of expansion potential just in Canada, with the U.S. a possibility longer term. That being a completely different market isn’t in the cards for now, but Pet Valu Holdings Ltd. should continue to win share in Canada and make investors a solid return for years to come.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here