Most investors by now can appreciate the opportunity that AI represents for society and the economy, and stocks like Nvidia (NVDA), Super Micro Computer (SMCI) and Dell Technologies (DELL) that are leading this revolution have been rewarded with rich valuations.

With so many investor eyeballs and fingers on the buy button whenever there are dips in those names, it’s hard not to wonder if we are in another sort of bubble. This reminds of the tech bubble in 2000, during which Cisco (CSCO) surpassed Microsoft (MSFT) to briefly become the world’s most valuable company, only to crash afterwards. To this day, CSCO still has not reached its all-time high price of $79 reached in 2000.

That’s why I remain bullish on value stocks that are beaten down in price for one reason or another, giving investors excellent opportunities to pick up yields that are well in excess of Treasury rates currently offer.

This brings me to the following 2 picks, both of which are trading far below the 52-week highs and below what I believe to be their intrinsic value. They operate in diverse industries from one another, thereby reducing concentration risk for investors, so let’s get started!

#1: W.P. Carey

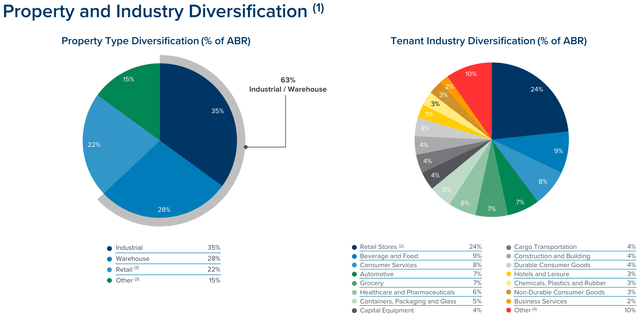

W.P. Carey (WPC) is a triple net lease REIT that gives investors exposure to properties both in the U.S. (63% of annual base rent) and Europe (37% of ABR). At present, it has 1,282 properties spread across 335 different tenants with a long weighted average lease term of 12 years.

WPC made headlines last year for spinning off Net Lease Office Properties (NLOP), its property portfolio Industrial/Warehouse, Retail, and Self Storage Properties. As shown below, WPC’s tenant base is well-diversified across a wide swath of the durable goods and services economy, with retail, beverage and food, consumer services, automotive, and grocery making up the top 5 segments comprising 55% of total ABR.

Investor Presentation

WPC’s AFFO per share was down by 13% YoY to $1.14 during Q1 2024, but this was due to the dilutive effects of the NLOP spin-off and continuing office sale program. At the same time, WPC saw an encouraging 3.1% contractual same-store rent growth on its continuing property portfolio and occupancy on the net lease portfolio sits at a high 99.1%.

What sets WPC apart is its aforementioned exposure to Europe, where pricing on property acquisitions have become more favorable over the past 12 months, creating more opportunities on the continent. Thus far in 2014, 70% of WPC’s investment volume has been in Europe compared to just 10-20% last year.

Another advantage to investing in Europe is the ability to raise debt there as well, where it was able to issue a 4.25% bond this year, sitting 150 basis points lower than what it could get in the U.S. This results in a favorable investment spread of 3.2% when compared against the 7.4% weighted average cap rate on acquisitions so far in 2024, with management expecting the yield on cost to rise to 9% after rental increases over the life of the leases.

Management is guiding for $1.5 to $2 billion worth of deal volume this year, and 54% of WPC’s leases are tied to inflation or CPI-based increases, thereby supporting the expectation for 3% in same-store rent growth this year.

Potential risks to WPC include recent tenant restructurings including re-leasing of some Hellweg properties (a German retailer and WPC’s 4th largest tenant), resulting in a 14.6% rent reduction starting in Q2. Nonetheless, WPC saw an encouraging 107% rent recapture rate so far this year excluding the Hellweg leases, and this is something I’d recommend monitoring over the next few quarters.

Importantly, WPC saw credit ratings upgrades to BBB+/Baa1 by S&P and Moody’s over the past 12 months. It also carried $2.8 billion of liquidity at the end of Q1, including $1.1 billion worth of cash on hand, and the recent bond offering of $400 million at a 5.375% rate due in 2034 adds fuel to WPC’s purchasing power.

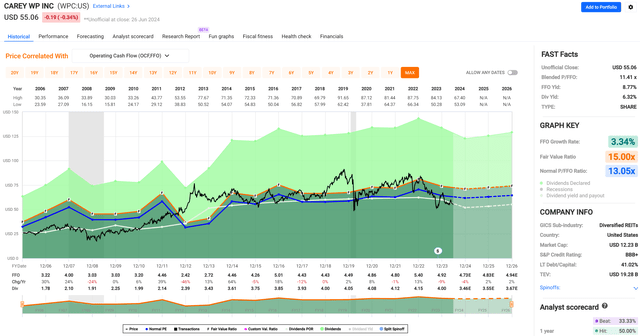

WPC’s recent drop in price from $60 in May to $55.06 results in an appealing 6.3% dividend yield, and it’s worth noting that WPC’s dividend has grown its dividend for 2 quarters in a row since the NLOP spin-off at $0.005 increments. The current dividend rate is covered by a 76% payout ratio based on Q1 AFFO per share of $1.14.

I find WPC to be attractive at the current price of $55.06 with a forward P/FFO of 11.6, sitting below its historical P/FFO of 13.1, as shown below. It also compares favorably to the sector median of 12.4, including peers like Realty Income (O), NNN REIT (NNN), and Agree Realty, which carry P/FFO valuations in the 12.6x (O and NNN) to 15x (ADC) range.

FAST Graphs

With a +6% dividend yield and my conservative expectations for long-term FFO/share growth of 4% annually, driven by rent escalators and external growth, WPC could realistically produce market level returns similar to the long-term average of the S&P 500 (SPY), all with a far higher yield and potential kicker with a reversion to its mean valuation.

#2: Bristol Myers Squibb

Bristol Myers Squibb (BMY) has been one of the most unloved stocks in the pharmaceutical industry over the past year. As shown below, BMY’s 34% decline over the trailing 12 months puts it well under the 27% rise in the S&P 500, the 1.4% decline of the SPDR Pharmaceuticals ETF (XPH), and even the 26% decline of Pfizer (PFE), another unloved pharmaceutical company.

BMY 1-Yr Price Return (Seeking Alpha)

One of the reasons for why BMY has fallen by so much may be due to market concerns around generic competition for its blockbuster drug, not least of which includes Revlimid, BMY’s blood cancer drug that treats MDS. Despite sales declines in Revlimid and Opdivo, BMY still managed to grow its revenue by 6% YoY on a currency neutral basis during Q1 2024, with drivers being newer drugs like Reblozyl and Eliquis.

Moreover, it has a strong pipeline that includes Breyanzi, Opdualag, and Camzyos, which treats disorders of the Lymphoma, Melanoma, and Cardiomyopathy, respectively. BMY is also positioned to see benefits from its recent acquisition of KarXT, which catalyzes clinical programs such as the one for Alzheimer’s.

According to Alzheimer’s Disease International, this affliction affects 55 million people worldwide, and is expected to double every 20 years, reaching 78 million by the end of this decade. This represents a big incremental market opportunity for BMY as management noted this as being a big unmet need at a recent Bank of America (BAC) global healthcare conference.

Importantly, BMY maintains a healthy balance sheet and has a credit rating of ‘A’ from S&P. This is supported by a safe net debt to EBITDA ratio of 1.6x and $10 billion in cash and equivalents on the balance sheets. This gives BMY plenty of dry powder with which to make bolt-on acquisitions, which may not be fully priced into the stock. BMY is also aggressively paying down debt, with $3 billion repaid during Q1 alone and $10 billion paid down over the past 2 years.

BMY currently yields 5.6% and the dividend is well-protected by a 33% payout ratio based on adjusted EPS guidance of $7.25 for 2024. BMY also has a 5-year dividend CAGR of 7.6% and 15 years of consecutive raises.

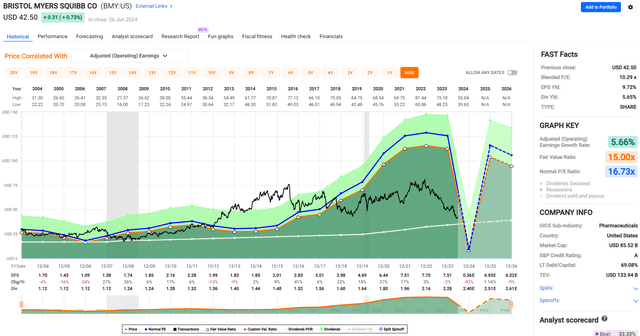

I find BMY to be highly appealing at the current price of $42.50 with a forward PE of just 5.9, sitting far below its historical PE of 16.7, as shown below.

FAST Graphs

At the current valuation, the market has priced in plenty of risks including generic competition, while seemingly ignoring the potential upside from aforementioned catalysts from newer drugs, KarXT, and potential future M&A opportunities for BMY in the pharmaceutical space. With a near-6% yield and my expectations for at least mid-single digit annual EPS growth over the long run, BMY has the potential to deliver market beating returns even without a reversion to historical valuation.

Investor Takeaway

Both W.P. Carey and Bristol Myers Squibb present great ‘buy the drop’ investment opportunities due to their attractive valuations, strong fundamentals, and high dividend yields. WPC, a diversified triple net lease REIT, offers a robust 6.3% dividend yield and potential for growth through its European property acquisitions and favorable debt conditions.

Similarly, BMY provides a 5.6% yield and prospects for long-term growth driven by a strong drug pipeline and strategic acquisitions. Both companies, with their respective strengths, undervaluation, and market positions, offer investors high yields and the potential for market-beating returns, making them appealing choices for value-focused investors.

Read the full article here