The stock market generally delivers 10 to 12% average annualized total returns over the long term. The high-yield sector (DIV) delivers a little bit less, as investors in these stocks tend to settle for slightly lower total returns due to lower growth in exchange for reduced sequence-of-return risk that comes from generating a high percentage of returns from dividends. That said, for investors who are willing to take a value investing approach and combine it with opportunistic capital recycling, the high-yield space is arguably one of the best places to generate long-term total return outperformance. This is because these stocks, by virtue of their low and predictable growth rates, are some of the easiest to value. Therefore, it is arguably the easiest space to take advantage of Mr. Market’s occasional mispricing of securities.

One sector where this has been very evident, especially in the years coming out of the COVID-19 outbreak, is the midstream space (AMLP). It is filled with blue-chip, investment-grade businesses that have very strong balance sheets, fully funded growth investment programs, and sky-high, very well-covered distributions/dividends that have been growing and appear poised to continue growing moving forward. Some companies in the sector are even buying back equity on top of paying out generous and growing cash to investors, while also investing in significant growth. In this article, I am going to discuss why I think the sector remains a compelling opportunity, but why it is unlikely to last much longer.

The Most Compelling High-Yield Sector Opportunity Remaining

As my regular readers know, my dream high-yield stock contains the following four qualities: It has a durable and defensive business model that can generate fairly stable cash flows through all kinds of economic cycles and does not face any near-term risk of being disrupted by technological innovation. It has a very strong balance sheet that, again, never forces management to choose between sustaining the distribution or protecting its balance sheet strength. It also has a well-covered distribution that is growing at a pace on par with or faster than inflation over the long term. Finally, its distribution yield is high enough such that the company does not need to generate more than mid-single-digit (and preferably low-single-digit) annualized growth in order to deliver market-level or market-beating total returns, without having to depend on valuation multiple expansion.

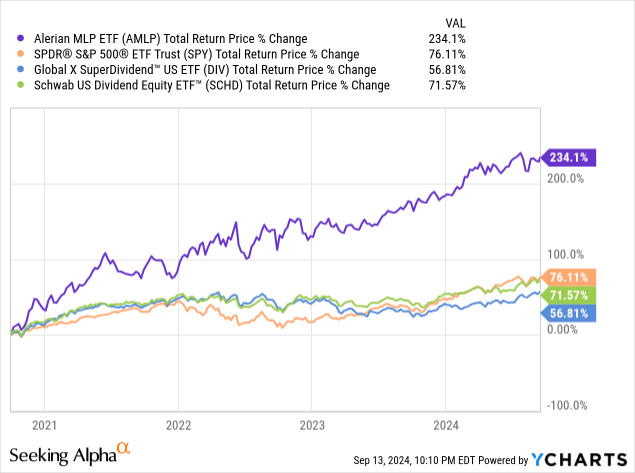

Right now, one of the best sectors for finding these sorts of stocks is the midstream space. Despite crushing the broader market (SPY) in the years coming out of COVID-19, and especially the broader high-yield space (SCHD), midstream still provides a compelling risk-reward today.

This is because the space has arguably never had stronger balance sheets, with the likes of Enterprise Products Partners (EPD), MPLX (MPLX), Enbridge (ENB), TC Energy (TRP), Williams Companies (WMB), Kinder Morgan (KMI), Energy Transfer (ET), and Plains All American Pipeline (PAA)(PAGP) all possessing some of the lowest leverage ratios in their history. These companies have very strong investment-grade credit ratings with significant liquidity and free cash flow generation. As a result, they are fully funding their internal growth programs and easily covering their payouts to investors. Some are even buying back equity, and all of them are growing their payouts at a pace that matches or beats the current rate of inflation.

On top of that, companies like Enbridge and TC Energy have highly regulated assets that should withstand all sorts of macroeconomic cycles and are at very low risk of technological disruption. Even the companies with less regulated exposure, like EPD, ET, and MPLX, have long-dated contract profiles, strategic asset positioning, and the AI boom as assurances that their assets should retain long-term economic value. This is because the demand for energy, of all types, is increasing rapidly between the AI boom’s projected demand for energy and the ongoing global energy needs driven by the war in Eastern Europe and growing tensions in the Middle East. These events pose a threat to the global energy supply. As a result, countries like the United States and Canada will need to continue producing fossil fuel energy for decades to come because there is simply not enough capacity or capability to build out renewables at a fast enough pace to meet the demand for energy.

Given these tailwinds for energy needs in Western economies, midstream businesses—with their contracted and regulated cash flows, strong demand visibility for decades to come, and durable, defensive nature—are well-positioned. We’ve already talked about how strong their balance sheets are, and we have also discussed how their distributions are very well covered, in most cases by 1.5x or greater, and growing at a minimum of 3% per year (but in many cases, 5% or even higher). For example, PAA has grown its distribution by double digits recently. Last but not least, the distributions in the sector remain very high. While some, like WMB and ONEOK (OKE), have dividend yields in the mid-single digits, many others have high single-digit or even double-digit yields. EPD, ET, and MPLX, in particular, all sport yields well over 7%, which are exceptionally well covered and likely to grow for years to come.

Investor Takeaway

When you combine all of these factors, it seems highly likely that there will also be valuation multiple expansion, especially with Federal Reserve interest rate cuts on the horizon. These cuts are likely to raise the net present value of highly contracted and regulated cash flows generated from infrastructure assets like midstream companies possess. As a result, when you combine the mid-single-digit annualized growth rates projected for years to come, the high single-digit cash flow yields, and valuation multiple expansion, there is a clear path to mid-teens annualized total returns for many stocks in the sector.

That said, if interest rate cuts come quickly and investors grow increasingly concerned about a slowing economy, there may be a flight within the energy sector towards midstream infrastructure as a more stable cash flow profile. This could serve as a hedge against potential weakness in energy prices. There may also be a rush towards utility-like infrastructure in general, as investors prize stable, attractive cash flow yields over more growth-oriented, speculative names that are more impacted by an economic slowdown.

As a result, it would not be shocking at all to see the midstream sector soar higher from here, potentially removing the compelling opportunity that still remains before investors to buy midstream stocks before it is too late.

Read the full article here