The Main Buywrite ETF (BATS:BUYW) is an actively-managed covered call ETF. As per the fund itself, BUYW invests in a portfolio of ETFs selected through fundamental reversion to the mean analysis, and sells covered calls on a portion of its holdings.

Although the fund has some benefits, its 1.31% expensive ratio is much higher than average, and its strategy has had mixed results since inception. Other covered call ETFs seem stronger as well, so I would not invest in BUYW.

BUYW – Basics

- Investment Manager: Main Management Fund Advisors

- Expense Ratio: 1.31%

- Dividend Yield: 4.97%

- Total Returns CAGR 5Y: 8.95%

BUYW – Overview and Analysis

Strategy and Holdings

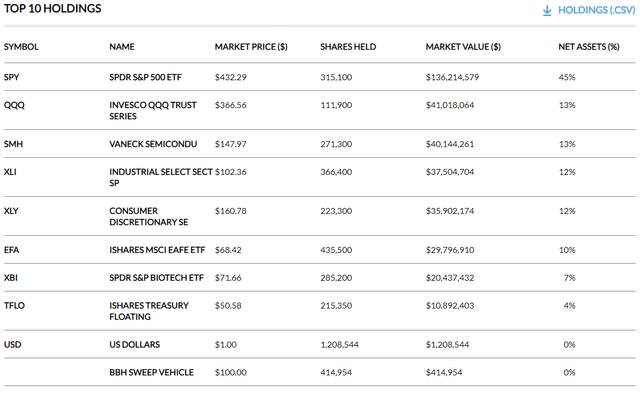

BUYW is an actively-managed ETF investing in a portfolio of ETFs. ETFs are selected through a fundamental reversion to the mean analysis, meaning it focuses on funds which recently experienced losses. At the same time, and from what I’ve seen, the fund consistently invests a significant portion of its assets in the SPDR S&P 500 ETF Trust (SPY). Current holdings are as follows:

BUYW

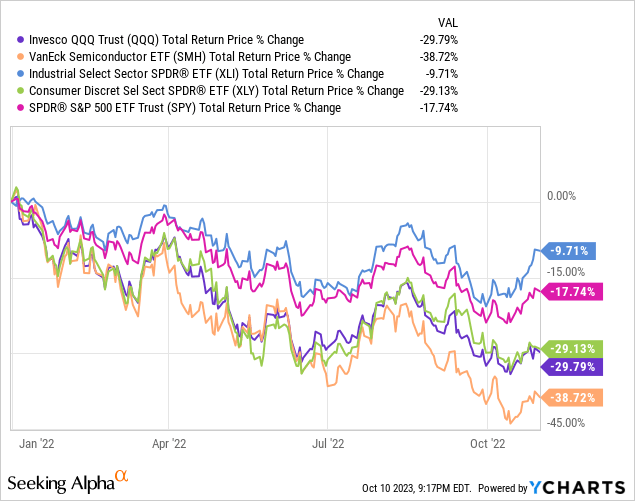

Holdings seem consistent with the fund’s strategy. Specifically, most of the fund’s larger holdings (excluding the S&P 500) underperformed during 2022. The Industrial Select Sector SPDR Fund ETF (XLI) is the only major exception.

Data by YCharts

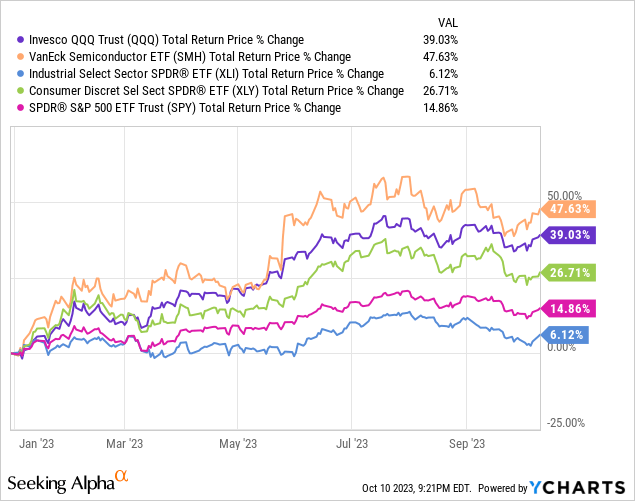

BUYW invested in the funds above expecting to profit from a (potential) recovery or mean reversion. In other words, the funds above were down in 2022 but would, hopefully, be up in 2023, leading to strong, above-average gains for BUYW. This was mostly the case, with the exception of XLI.

Data by YCharts

BUYW’s strategy seems reasonable enough, although I don’t really have any strong theoretical or practical reasons to believe that it will be successful moving forward. Stocks tend to experience momentum, so losses tend to be followed by more losses, and vice versa. Momentum means that the fund’s strategy is likely to be ineffective moving forward, but much will depend on the specifics of the strategy, including selected funds, as well as broader market conditions. The strategy does seem to have worked YTD.

BUYW also sells covered calls on some of its holdings. Specifics and percentages vary. In the past, the fund overwrote upwards of 95% of its holdings. Right now, the figure is closer to 80%.

Selling covered calls means lower capital gains but higher dividends. This generally results in underperformance during bull markets, but outperformance during flat and bear markets. Stocks tend to go up, so the impact is generally negative.

BUYW changed from a mutual fund to an ETF in 2022, which makes it difficult for me to check some of its past performance. Due to this, it is not really possible for me to show investors how the fund’s covered call strategy impacts its returns. Nevertheless, I’m quite confident in the description above, and do believe that the fund will perform as expected moving forward.

In general terms, BUYW does not significantly differ from most of its covered call peers. Selling covered calls have more or less the same impact regardless of the fund doing so, although obviously specifics vary. BUYW’s reversion to the mean strategy does impact performance, but the fund does tend to invest quite heavily in a simple S&P 500 index fund. There is some active management, but there is quite a bit of index investing as well.

Dividend Comparison

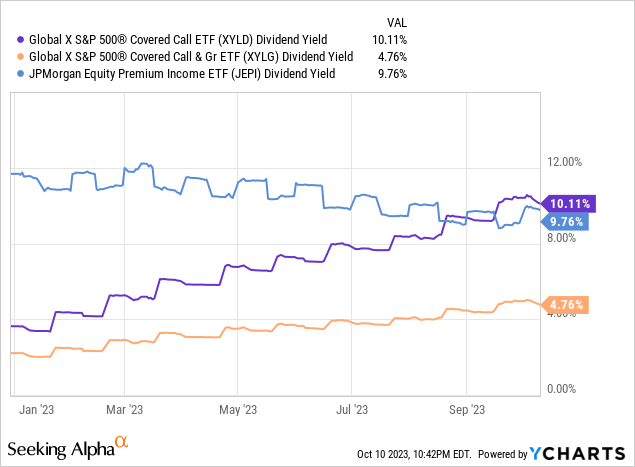

BUYW’s covered call strategy generates a good amount of option premiums, resulting in higher dividends and yields. The fund itself currently yields 5.9%, quite a bit higher than the S&P 500’s 1.5% yield. On the other hand, the fund’s dividends are lower than average for a covered call ETF. Quick look at some of the most relevant of these.

Data by YCharts

BUYW’s 5.9% dividend yield is obviously a positive, and advantage relative to the S&P 500 and most other broad-based equity indexes. On the other hand, it compares unfavorably to the dividends of some of its peers. Investors in covered call ETFs might prefer these other funds, for obvious reasons.

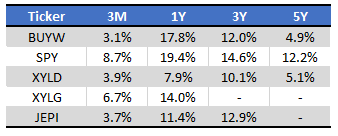

Performance Comparison

BUYW’s performance track-record is quite similar to those of its covered call peers. Long-term performance is quite weak, as BUYW experienced few of the capital gains of 2020 and 2021. Recent performance has been much stronger, as increased volatility led to higher option prices.

BUYW and Seeking Alpha – Chart by Author

In my opinion, BUYW is evenly matched on a performance basis relative to peers. No reason to pick one over the other from the figures above.

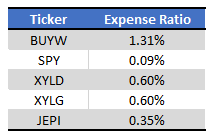

Expenses Comparison

BUYW is a relatively expensive fund, with a 1.31% expense ratio. Expenses are significantly higher than those of most equity ETFs, including most covered call ETFs.

Seeking Alpha – Chart by Author

Higher expenses directly reduce total shareholder returns and dividends, straightforward negatives. Higher expenses are also an almost certain negative: risks sometimes fail to materialize, lower capital gains might not impact a fund during bear markets, but higher expenses effectively always mean lower returns.

In my opinion, cheaper funds are generally better than expensive ones. Exceptions can be made for funds with particularly attractive yields, expected total returns, or those focusing on niche asset classes. BUYW is neither of these, with the fund holding few advantages relative to its peers.

Conclusion

BUYW invests in a portfolio of ETFs selected through fundamental reversion to the mean analysis, and sells covered calls on a portion of its holdings. BUYW compares unfavorably to most of its peers, and is much more expensive than average. As such, I would not invest in BUYW.

Read the full article here