On Seeking Alpha’s free site, I’ve written two pieces on BuzzFeed, Inc. (NASDAQ:BZFD).

Picking back up on the research trail, lo and behold, just as I forecasted, within the July 29, 2024 piece, BuzzFeed provided its best Q3 guidance ever, when they reported Q2 FY 2024 results (August 12, 2024).

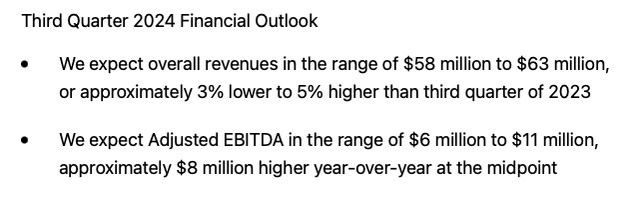

BuzzFeed, Inc.’s Q2 FY 2024 Earnings Press Release (August 12, 2024)

Given my high conviction level, as you might expect, I’ve done a fair amount of work on BuzzFeed.

For perspective, at the mid-point of its Q3 FY 2024 guidance, this would mark the highest ‘Q3’ Adj. EBITDA, as a publicly traded company.

BuzzFeed’s Historical Adj. Quarterly EBITDA

Adj. EBITDA FY 2024: TBD

- Q4 FY 2024: TBD

- Q3 FY 2024: $8.5 million (mid-point of guidance)

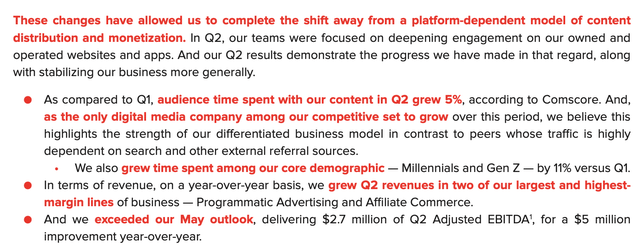

- Q2 FY 2024: $2.7 million

- Q1 FY 2024: -$11.4 million

Adj. EBITDA FY 2023: (-$4.7 million)

- Q4 FY 2023: $15.1 million

- Q3 FY 2023: $3.1 million

- Q2 FY 2023: -$.137 million

- Q1 FY 2023: -$20.2 million

Adj. EBITDA FY 2022: (500K)

- Q4 FY 2022: $17.6 million

- Q3 FY 2022: -$2.4 million

- Q2 FY 2022: $2.1 million

- Q1 FY 2022: -$16.8 million

Adj. EBITDA FY 2021: $41.5 million

- Q4 FY 2021: $34.2 million

- Q3 FY 2021: $6 million

- Q2 FY 2021: $5.6 million

- Q1 FY 2021: -$4.3 million

(Author’s Chart)

In addition to the strong Q3 FY 2024 guidance, the press release and conference call were full of ‘green shoots’ and compelling evidence of a business turnaround.

The Q2 FY 2024 Earnings Press Release Highlights

1) Per commentary on the August 12, 2024 conference call, there is no material ‘direct political ad spend’ baked into/ assumed into Q3 FY 2024 guidance.

See below:

In terms of content revenues, we do expect to see an improvement in the year-of-year revenue trends versus what we saw in Q2. It’s also worth noting that although historically we have seen a lift in direct sold revenues ahead of the US Presidential election, the majority of this spend typically occurs in the fourth quarter. As such, our Q3 guidance does not assume any material lift from political sales.

(BuzzFeed, Inc.’s Q2 FY 2024 Conference Call (August 12, 2024))

Jonah’s Q2 FY 2024 Investor Letter Reads Great

Check out these qualitative highlights that clearly showcase a real business turnaround / tangible inflection points in the business.

Exhibit A: AI Generators Drive Enhanced Engagement

BuzzFeed, Inc.’s Q2 FY 2024 Investor Letter (August 12, 2024)

Examples:

Exhibit A: Minions “AI” Celebrity Generator (August 1, 2024)

BuzzFeed, Inc.

Exhibit B: Shrek “AI” Celebrities (May 9, 2024)

BuzzFeed, Inc.

Exhibit C: Create Your Own AI Emoji (February 28, 2024)

BuzzFeed, Inc.

2) According to Comscore, BuzzFeed was the only digital media, in its peer group, that saw audience time spent grew (by 5%), from Q1 to Q2 2024.

BuzzFeed, Inc.’s Q2 FY 2024 Investor Letter (August 12, 2024)

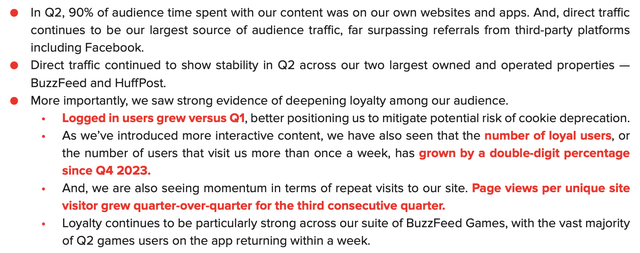

3) As I’ve discussed many times, 90% of BuzzFeed’s traffic and engagement is directly from its owned and operated sites. They have now lapped the major Meta Platforms (META) changes.

Additionally, there are clear ‘green shoots’ when it comes to engagement trends. These are all tailwinds that should drive future and stronger advertising revenues.

BuzzFeed, Inc.’s Q2 FY 2024 Investor Letter (August 12, 2024)

4): Q2 Programmatic advertising revenue grew 3% YoY. This was the first quarter of YoY growth since Q1 2022!!

BuzzFeed, Inc.’s Q2 FY 2024 Investor Letter (August 12, 2024)

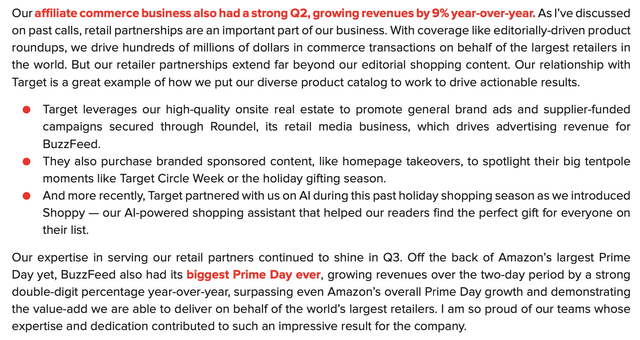

5): A Strong Affiliate 9% YoY revenue growth – driven by a record Amazon Prime Day and continued strong partnership with Target

BuzzFeed, Inc.’s Q2 FY 2024 Investor Letter (August 12, 2024)

The Elephant In the Room – The December 3, 2024 $120 million 8.5% Convertible Debt Put Option, two years ahead of its official maturity date

Although BuzzFeed’s stock price recovered, post Q2 FY 2024 earnings, with share rebounding, back to the $2.80s and $2.90s (August 13th – August 20th), and it briefly traded up to $3.005, on August 21st, low conviction/ fast money traders took their profits and subsequently, BuzzFeed share have drifted back down to a lower band, hovering between the $2.20s to $2.40s per share.

For a company that is clearly inflecting, as of last night’s closing price, of $2.41 per share, its market capitalization was only $92 million. Moreover, if you spend the time to closely evaluate its balance sheet, you will note, as of June 30, 2024, $45.5 million of cash, and they did a nice job of reducing the company’s accounts payable balance. This means they are not hiding/ don’t have any shadow debt per se, in the form of stretched payables, which points to balance sheet strength. In fact, BZFD’s accounts payable balance is now in great shape.

The elephant in the room is the $120 million of 8.5% 12/3/2026 convertible debt that has a lender ‘put option’ of 12/3/2024.

Given this persistent overhang, with a lot of fear priced into the current equity price, enclosed below are how I would resolve it and gracefully negotiate the elephant to pirouette out the ballroom.

1) Sell First We Feast For At Least $60 million

In case you haven’t closely read my two prior pieces, BuzzFeed, Inc. owns its namesake brand, BuzzFeed.com, HuffPost.com, and First We Feast/ Tasty. First We Feast owns the very valuable and highly popular show, Hot Ones. Hot Ones just wrapped up its 24th season and there have many dozens of ‘A’ list celebrities, music stars, and athletes on the show. In May 2024, Entertainment Weekly ranked the top 20 best Hot Ones episodes, since inception. Incidentally, as I’m really in the weeds here, Seasons 2 – Season 20 are available for viewing on Amazon Prime (AMZN). The more recent seasons, 21 – 24, are only available on YouTube. As an aside, on Amazon Prime, this past weekend, I watched the Dave Grohl episode, which I loved.

Recently, the show hosted Ariana Grande. Get this, Ariana Grande asked Hot Ones to be on the show. In addition, to give you a sense of how popular a show this is, ahead of the launch of its blockbuster movie, Deadpool & Wolverine, in July 2024, both Hugh Jackman and Ryan Reynolds appeared on Hot Ones. So far, on Google’s (GOOGL) YouTube, there have been north of 28 million views.

If you are really paying attention, you will also note that Hot Ones has major brand sponsors for a series of shows. For example, the Ariana Grande show, as well as the recent David Beckham shows, were sponsored by the beer brand Stella Artois, which is owned by Anheuser-Busch InBev (BUD).

Although First We Feast is a great asset, in one fell swoop, if BuzzFeed sold the business for at least $60 million, the company could defuse the ticking time bomb, its 12/3/2024 debt put option.

2) Refinance The Debt Or Give The Lenders Some Warrants For A One Year Extension

The second option is to recut the convertible deal, perhaps with a new $5 strike price, if the lenders would be amenable. It is hard to know, though, as I don’t move in those circles. Also, the terms would really matter given the size of the debt relative to the current market capitalization. Alternatively, given the clear signs of a business turnaround, Jonah, its CEO, as he controls the super voting shares, could elect to raise secured term loan debt. Perhaps, BuzzFeed could find a new $100 million 8% to 10% term loan option with additional small revolver, maybe $25 million, for seasonal working capital swings. Thirdly, and relatedly, I would argue it is possible for BuzzFeed’s management team to offer the current lender group warrants. For example, perhaps 3.8 million warrants, or 10% dilution, at a $2.5o or $3 strike price in exchange for a one year put option extension, from 12/3/2024 to 12/3/2025.

If they elected to the agree to the one year extension, this could shift the power dynamics within the First We Feast sale negotiation process, as per the June 2024 Bloomberg article, BuzzFeed hired investment bank, UBS, to shop First We Feast.

In other words, given how strongly the First We Feast business is performing, as Hot Ones continues to crush it, arguably the strength of its Direct Advertising Partners, on Hot Ones, are a good example of the valuable currency the show holds, given how many celebrities ask to go on. Relatedly, it is one the ‘go to shows’, akin to going on Larry King, of decades past, to promote your latest venture (a new book, a new music tour, a new movie, a new podcast, etc.).

Arguably, given additional time, it is possible that BuzzFeed might be able to spark a bidding war, for First We Feast, as the company would no longer be viewed as a distressed seller. This would benefit the current convertible lenders as contractually entitled, via covenants, to 95% of any asset sale proceeds. So, getting the best price for First We Feast would mean getting more debt principal, paid back at par, for a bigger slug of the remaining outstanding debt. Plus, as I mentioned, they would get to participate in any equity upside, via an option to perhaps buy up to 10% of the equity, via warrants, at an in the money to modestly above the money strike price. For example, if the lenders could make $2 points, on 3.8 million shares, that is a nice kicker in exchange for giving a one year extension on the debt.

This would be win-win thinking.

3) Further, given that the 2024 Presidential Election could be the highest ever political ad spending window, which really heats up from mid September 2024 and right down to the wire, through early November 2024, BuzzFeed is well positioned to benefit, perhaps directly via ad spending and most likely indirectly via elevated HuffPost readership engagement. Moreover, as a lot of ad dollars find their way into programmatic spending, at least in the short term, this should enhance CPM rates, during Q4, for many programmatic advertisers, including BuzzFeed’s core site.

Moreover, Since Kamala Harris has taken the baton from Joe Biden, engagement within the democrat party has surged. I don’t think it takes a rocket scientist to work out this a net positive for HuffPost, in both Q3, and especially Q4 2024.

If you go back to my history quarterly Adj. EBITDA data, I would very conservatively argue, in Q4 FY 2024, BuzzFeed could easily generate $30 million of Adj. EBITDA.

Conservatively, the Q3 FY 2024 guidance, at the mid-point of $8.5 million, plus another $30 million, in Q4 FY 2024, less the semi-annual cash interest expense, on December 3, 2024, could mean that BuzzFeed should be able to generate meaningful second half FY 2024 free cash flow. I would argue upwards of $30 million, of 2nd half FY 2024 free cash is attainable.

The Math Behind Me Modeling $30 Million In Q4 FY 2024 EBITDA

Since May 1, 2024, BuzzFeed has taken $23 million of annualized costs out of its business. If you take this sum and dividend by four, that is a $5.75 million quarterly uplift. I’m assuming the massive political ad spending environment will lead to higher CPMs, industry wide, on the programmatic side of the business and this could create a $3 million to $5 million tailwind. Next, strong momentum in BuzzFeed’s affiliate business, where they get a 10% revenue share on merchandise purchase via its owned websites, could be a $3 million uplift, given the strength we saw in Q2 FY 2024, with its Amazon partnership. Moreover, BuzzFeed has a strong relationship with Target (TGT). Lastly, I’m assuming a $5 million to $10 million uplift, in Q4 FY 2024 tied to a small amount of direct political spending, on HuffPost as well as higher user engagement directly tied to the Presidential election, more so on HuffPost, but also on BuzzFeed.

In FY 2022 and FY 2023, BuzzFeed’s Adj. EBITDA was $15.1 million and $17.6 million, respectively, yet currently, BuzzFeed’s core business has a lot more turnaround momentum and enhanced user engagement.

Therefore:

- $16 million baseline (using a historical blend of Q4 FY 2022 and Q4 FY 2023)

- Plus $5.75 million in quarterly cost savings

- Plus $3 million to $5 million from higher CPMs on the programmatic side driven by a surge in programmatic advertising that lifts all boats

- Plus $3 million from higher affiliate engagement (Amazon and Target)

- Plus $5 million to $10 million from higher political ad spending (some very modest direct ad spending and higher engagement that will drive more clicks)

If you add all of these up, you quickly arrive at $33.75 million (low end) to $40.75 million (high end). However, to be conservative, I’m only modeling $30 million of Q4 FY 2024 EBITDA.

So, on a pro-forma basis, with $45.5 million of June 30, 2024 existing cash, upwards of $30 million of second half 2024 free cash flow, and the possibility of selling First We Feast for a net $60 million, that is more than enough money to easily handle the $120 million debt and /or getting a new $50 million revolver for working capital, depending on whether they elect to sell First We Feast.

That said, I don’t want to jinx it, but I don’t think BuzzFeed’s management team has to hit all green lights coming here for this equity to work well. The key is management has to evaluate my list, or one similar, which I’m sure (or at least I sure hope), that they have options A, B, and C lined up, so there are no December 3, 2024 surprises that would adversely ding common shareholders.

Adj. EBITDA FY 2024: TBD

- Q4 FY 2024: TBD

- Q3 FY 2024: $8.5 million (mid-point of guidance)

- Q2 FY 2024: $2.7 million

- Q1 FY 2024: -$11.4 million

Adj. EBITDA FY 2023: (-$4.7 million)

- Q4 FY 2023: $15.1 million

- Q3 FY 2023: $3.1 million

- Q2 FY 2023: -$.137 million

- Q1 FY 2023: -$20.2 million

Adj. EBITDA FY 2022: (500K)

- Q4 FY 2022: $17.6 million

- Q3 FY 2022: -$2.4 million

- Q2 FY 2022: $2.1 million

- Q1 FY 2022: -$16.8 million

Adj. EBITDA FY 2021: $41.5 million

- Q4 FY 2021: $34.2 million

- Q3 FY 2021: $6 million

- Q2 FY 2021: $5.6 million

- Q1 FY 2021: -$4.3 million

The Activists

Currently, Vivek Ramaswamy owns a 8.8% stake in the business. He has filed a 13D, has a lot of direct and indirect resources and he has asked management to make major, major changes to the business. Given Jonah’s super voting shares, it is unclear how swayed he has been by Vivek’s arguments/ letter/ strategic direction. It seems like Vivek has been spending the vast majority of his time on the campaign trail, on behalf of Donald Trump, as perhaps he simply lacks the bandwidth for a big activist fight. Unless Vivek is able to buy up a big portion of the $120 8.5% convertible debt, ahead of December 3, 2024, and he would have to file this ownership stake, within 48 hours, it is hard to speculate on his intentions.

Outside of Vivek, who is definitely formidable, there have been various media reports that William J Pulte took an activist stake. The Pulte family is extraordinarily wealth, with a net worth well into the many billions, however, this seem like a small side project, at best. Additionally, in late July 2024, it was reported that Edge One Capital, a buy side outfit, operating in North Carolina, also took a stake. Incidentally, I have read William Pulte’s letter as well as both of Edge One’s letters and found none of them to be compelling.

Unless and until I see new SC 13D forms filed, with at least a 5% stake, respectively, as BuzzFeed’s market capitalization is just shy of $100 million, I’m both uninspired and not swayed by the activism of Pulte or Edge One.

Risks

As I already spelled out, the biggest risk is the elephant in the room, the $120 million of 8.5% debt that is puttable on December 3, 2024. Management cannot assume that its lenders will play nice. That is much too dangerous a stance and risk leaving the equity vulnerable. BuzzFeed’s management team absolutely can’t leave anything to chance. Options A, B, and C must be full evaluated, considered, and potentially lined up and ready for ‘D-Day’ scenario, on December 3, 2024. Additionally, the longer it takes for management to resolve this, BuzzFeed’s equity could be more volatile as this leads to uncertainty.

Putting It All Together

BuzzFeed, Inc.’s turnaround is well in motion, as there is compelling evidence of many ‘green shoots’. Moreover, the 2024 Presidential election cycle, and the selection of Kamala Harris, as the democratic nominee, is perfect timing to help BuzzFeed be positioned to generate material 2nd half 2024 free cash flow. BuzzFeed should benefit from some direct political ad spending as well as indirectly via a lot of engagement on HuffPost, and possibly via better programmatic CPMs, as a lot of ad dollars overwhelm the finite amount of supply, for a very short period of time, in Q4 2024.

The only reason why BuzzFeed’s stock price is trading at such an arguably low low/ pessimistic valuation, of only $2.41 per share, is because of the elephant in the room, the $120 million 8.5% 12/3/2024 debt put option. In today’s piece, I provided multiple pathways/ option for BuzzFeed’s management team to diffuse this ticking time bomb, something that threatens BZFD’s equity.

Hopefully, always a dangerous word when it comes to investing, BuzzFeed’s management is very far down the path, and is working on a cocktail of solutions, consisting of some form of options one, two, or three, that I highlighted in today’s piece. Sooner than later would be greatly preferred. At this point, it is up to BuzzFeed’s management team to ‘unlock’ a tremendous amount of equity value by diffusing the tick debt clock.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here