Caleres, Inc. (NYSE:CAL) is a footwear retailer and manufacturer. The company owns the Famous Footwear retail chain and a portfolio of footwear brands, such as Sam Edelman, Naturalizer, Allen Edmonds, and Vionic.

This article covers the company’s 1Q24 results, reported today, and the 1Q24 earnings call. The company posted a slight miss in the top line of $5.6 million, with EPS in line with expectations at $0.88. The stock was down 2% in the afternoon. Overall, I believe the results show some end-market challenges, particularly in the branded portfolio. In terms of margins, the company is sustaining margins thanks to more DTC revenue and lower freight costs, but promotions are increasing, also indicating market challenges.

I started covering Caleres in March 2024 with a Hold rating. I liked the fact that the company owns a brand portfolio from where to build intangible brand value. Particularly, this brand portfolio focuses on higher-end segments of the market, where brand equity is easier to build than in more value-conscious segments. However, my rating was based on the company’s valuation, which was reasonable considering the maintenance of margins, but it would be high if we forecast a return to pre-pandemic margins. Since March, the company’s valuation has not changed meaningfully, so I maintain my Hold rating.

Q1 2024 results

Caleres 1Q24 results were not very good. Sales were down 0.6% on an absolute basis, and operating margins decreased by one percentage point to 6.5%, compared to 7.5% in 1Q23.

Famous Footwear, the company’s retail chain, saw revenues decline 2.3% on a comparable basis. According to management, the chain saw soft demand for seasonals such as boots and sandals. The chain’s gross margins increased 50 basis points to 46.1%, but management mentioned on the call that this was caused by higher e-commerce sales (which carry a higher gross margin) and a reduction in freight costs, offset by higher promotions.

The branded portfolio, which includes both DTC (store, e-commerce) and wholesale revenues, was flat on a comparable basis but down 2.5% on an absolute basis. The segment’s margins gained 200 basis points to 46.6%. Again, in this case, management mentioned on the call that the margin gain was driven by mix (more sales DTC than wholesale).

The aggregate results were gross margins up 120 basis points, to 46.9% at the consolidated level. This was more than offset by higher SG&A expenses, probably from 6 more stores in the branded segment. The net result was lower operating margins of 6.5% compared to 7.5% last year.

Intangibles investment

I believe one of Caleres’ most interesting aspects is its brand portfolio. The brands (explained in detail in my previous article) generally target premium and fashion segments. Companies can build intangible brand equity in premium and fashion segments because customers are more concerned with quality and intangible values like status than price alone. Further, footwear retailers have a hard time not discounting if their competitors do because the same assortment (say, a pair of Nike sneakers) can be found at the competitor’s stores, too. By having its own brands, Caleres can protect itself from this dynamic.

In this respect, management commented on the earnings call that most of the flagship brands are performing better. Naturalizer reached the 11th position in the Circana Women’s Fashion Footwear ranking. Allen Edmonds saw its 13th consecutive quarter of revenue growth and opened a wholesale account with the premium retailer Nordstrom. Vionic also saw revenue growth, and Dr. Scholl’s (a licensed brand) saw two models (the Time Off and the Madison Lace) sell off thanks to viral reactions on TikTok. Sam Edelman was the only challenged brand. This is a sandals brand, and management commented on the weakness in the sandals category for the retail segment, which might explain Sam Edelman’s performance.

Caleres invested in the brands in the quarter, launching a campaign centered around successful women entrepreneurs for Naturalizer and participating in a Nordstrom campaign promoting shoes.

Intangible investments are essential to build brand value, potentially translating into higher pricing, sales, and margins.

Margin challenges

As mentioned in my previous article, one of my main concerns for footwear retailers is their promotional activity, which can quickly erode margins.

Management’s mention of more promotional activity in Famous Footwear is not good in this respect. The reading is more difficult in the branded segment because higher DTC sales (at higher margins) might offset the promotional activity.

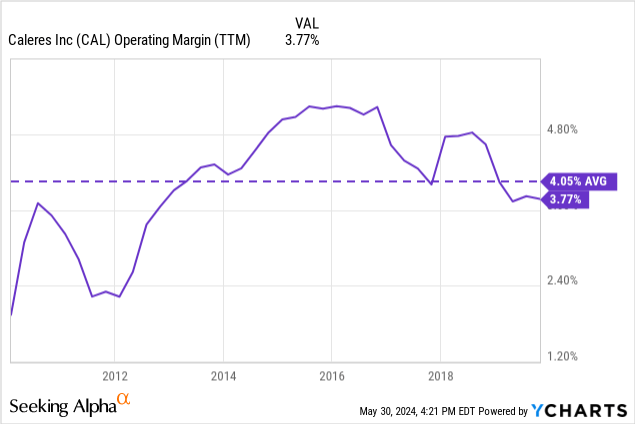

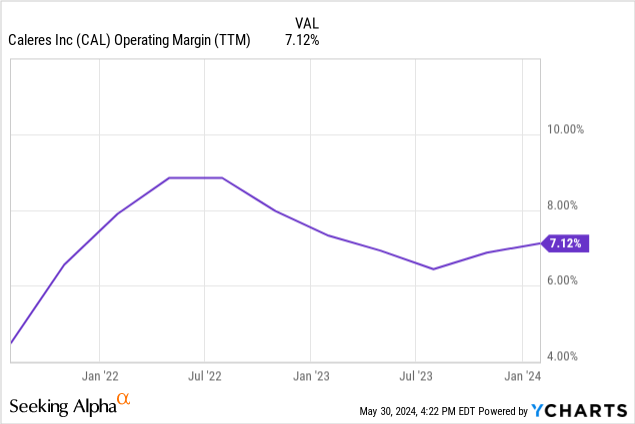

Overall, though, Caleres continues to show a consistent trend of lower YoY operating margins, which, I believe, will eventually return to a mean closer to its pre-pandemic average.

The company’s management reaffirmed FY24 guidance in the 1Q24 call. Caleres expects sales to rise 1% in the middle of the range and operating margins to be 7.5%. This would imply an operating income of $211 million, basically flat compared to FY23’s $207 million. Using a tax rate of 25% leads to NOPAT of $158 million.

However, I also consider that the company’s expected margins are high compared to its pre-pandemic average, generally below 5%. Further, operating margins have been decreasing, so the company’s expectation of 7.5% operating margins for the year is not very conservative (the second YChart below does not include 1Q24 data with margins down one percentage point YoY). If we forecasted Caleres’ long-term profitability with a 5% operating margin at the current level of sales, it would result in an operating income of $140 million or NOPAT of $105 million.

Valuation

Caleres has a market cap of $1.3 billion. Adding net debt of $160 million ($191 million in a revolving facility and about $31 million in cash) leads to an EV of $1.46 billion.

This results in an EV/NOPAT multiple of 9.2x compared to management’s guidance and 14x if we assume a return to 5% operating margins. I believe it is conservative to consider a mid-point of the two, given that Caleres margins are decreasing. The result is an average of 11.6x.

I believe this multiple is reasonable, but not opportunistic for a company like Caleres. Footwear retailing, which comprises half of the business, is a highly competitive market, where promotions driven by competitors can quickly erode a company’s sales or margins. The branded segment is better positioned, but Caleres is still building these brands, none of which are top-tier brands that can command significant pricing power yet.

Also important, Caleres average lease life is six years (according to their FY23 10-K), providing very little flexibility in terms of store fleet if the economy turned sour. In addition to this, Caleres has $190 million in debt and $31 million in cash, something I consider a leveraged position for a retailer. Retailers already have operational leverage (from fixed costs like stores and sales employees). Adding financial leverage makes them even more risky.

I would reconsider Caleres at a lower multiple, probably below 10x under a conservative scenario, like 5% operating margins or lower.

Conclusions

Caleres, Inc. 1Q24 earnings were not very good, showing growth challenges and some signs of higher promotions. The operating margin erosion continues, leading me to give more weight to the scenario of a return to mean pre-pandemic operating margins.

In terms of business quality, Caleres mixes a competitive footwear retailing business with a more branded (and potentially more protected) footwear design business. The recent investments in intangibles for the branded business are a good point.

Considering two margin scenarios, Caleres, Inc.’s multiple comes to an EV/NOPAT of 11.6x. I believe this is fair but not opportunistic for a company of Calere’s characteristic. For that reason, I think Caleres stock does not present an opportunity at these price levels.

Read the full article here