Dear readers/followers,

In this article, we’ll take a look at Camden Property Trust (NYSE:CPT), a REIT I’ve been looking at previously and invested in when it was comparatively very cheap. The company is a multi-family REIT with a very conservative overall leverage. The yield isn’t the greatest, but I believe it’s made up by the overall safety of the business.

It’s a roll of the dice if you want to call this REIT “Cheap”. You certainly could, if we look at the long-term valuation levels and averages. However, given the premium the company typically commands, any sort of cheapness needs to be viewed in the context of this.

In this article, we’ll look at what’s possible in terms of upside and returns for this business.

I own plenty of Essex Properties (ESS) and AvalonBay (AVB) – but Camden Property Trust (CPT) so far has had a relatively minor role in my coverage. I aim to change that, now that the company is actually getting cheaper. Becoming “cheap” is something that requires consideration here. Even at today’s price, Camden yields less than 4%, which is less than you can get risk-free from a money market fund. However, then you’re not including into consideration what you might get from the company seeing normalization.

So, let’s see what we have here.

Camden Property Trust – Plenty to like, even at a slightly higher valuation

Since I wrote about the company last, this business has seen some improvement in terms of results and upside. 1Q24 is the last quarter we have, and this was released back in early May of 2024.

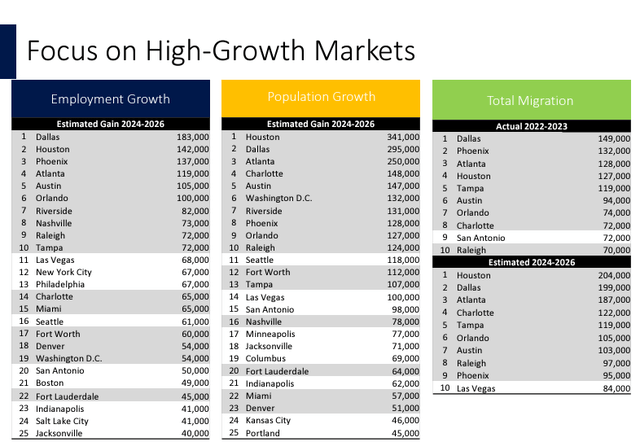

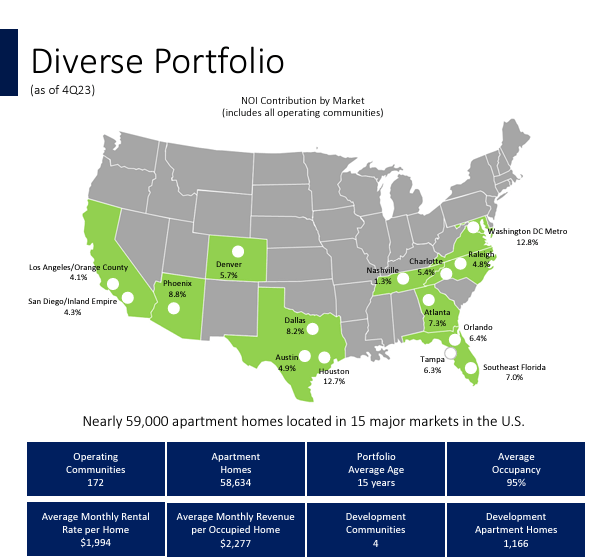

The company’s focus remains on high-growth markets from the perspective of a number of KPIs, including but not limited to employment trends, population trends, and migration trends. The goal is the delivery of consistent earnings growth, and the operation of a diverse portfolio of very high-quality assets with in turn a high-quality profile of the residents found therein.

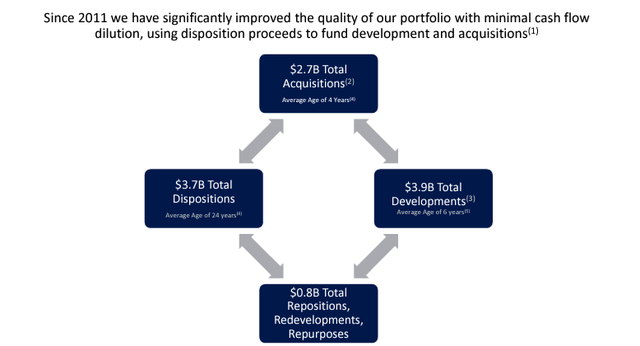

The company, like any REIT in this space and location, is also an active recycler of capital and assets, trying to create more value not only through dispositions but through development, repositioning, redevelopment, and other moves that in the situation make sense to the company.

The company tries to maintain a very strong balance sheet with low leverage, ample liquidity, and the ability to capitalize on opportunities.

In this way, the company is indeed very attractive.

Camden Property Trust IR (Camden Property Trust IR)

The company has been a very capable grower of capital and dividends over time, with good forward DGR since 2018 at the very least, and is expected to at the very least maintain current levels of earnings and dividend growth, while maintaining a very diversified portfolio, that with the exception of some of the Californian exposure, can be said to be very solid.

CPT IR (CPT IR)

The average person who decides on a CPT home is 31 years of age with an average household income of $122k per year and a rent-to-income ratio of under 20% for the new move-ins in 4Q of last year. In short, the company maintains a very strict profile and credit checks to make sure that the tenants coming to their objects are able to financially support them – but at an average number of occupants of 1.7, the company also focuses on singles or young couples – families with children seem far rarer in this set of assets.

The company also maintains a very active repositioning of capital.

Camden IR (Camden IR)

Camden also has a very good track record of value creation for these objects. Out of 40 developed and renovated communities since 2011, the company has focused on over 12,000 apartment homes, at a total cost of nearly $2.9B, but with a current market value of almost $4B, meaning that there was a value creation of ~$1B – and that is not a bad track record over the course of 11-12 years.

The company’s capital structure remains iron-sold. We have ratings of A- and A3, as well as maturities not relevant above the $530M level annually until 2028, with only one over $500M until then. 80%+ of the maturities are in unsecured debts, with only $300M of secured debt of the entire capital structure, at a market capitalization of $14B.

Recent results were all but poor. The company closed over $1.2B in refinancing and transactions, meaning there are no current balances in the LoC, and only $290M of debt in all of 2024-2025 – peanuts, compared to the company’s annual revenues and NOI. Camden also increased the dividend by 3% – not that much, but still respectable for a REIT of this type, to $4.12 per share. The company also took advantage of the low valuation to buy back significant shares – over 150,000 shares in fact at under $95/share.

Disposals during the last quarter were low – only ~600 in Atlanta, while new leasing reached 98% in the new Camden NoDa in Charlotte, well ahead of the company’s original schedule.

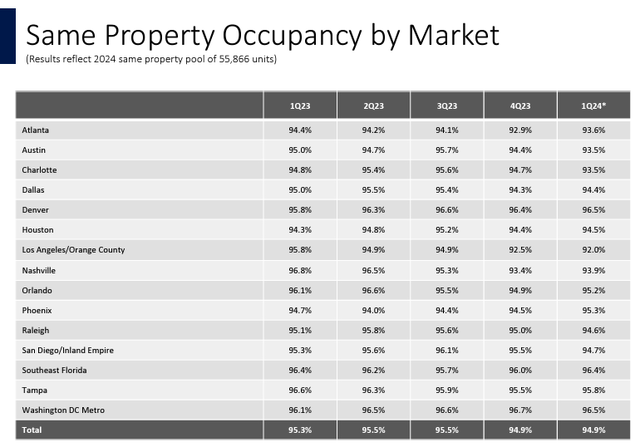

European REITs have higher occupancy – but not by much. The total is just below 95% at this time, which is a positive here.

Camden IR (Camden IR)

One of the main risks to any REIT in this space is delinquencies. Unfortunately, Camden has some of them. While the company may call these “the lowest since the pandemic”, the fact even 0.8% of net same property bad debt, with 0.4% high balance delinquencies is too much for a company like this. Still, it’s down by over 90 bps in around 1.5 years, which is an improvement, and the company reports further declines expected going forward. Some of this is also outside of Camden’s control, those being state law-oriented debt management laws and statutes.

Multifamily fundamentals are looking up, much like senior housing and other housing segments in the REIT space. This has to do with a very low number of housing starts, with a slight completion bump in the middle of this year, only to crater significantly in 2025, leading to a probable higher rate of overall demand.

CPT IR (CPT IR)

On a forward basis at least – current expectations are for demand to grow again around 2025-2027, with the pent-up demand from young adults at home, and the 67 million of these will remain a steady source of demand at this time, and going forward.

There is also a higher likelihood for these people to rent as opposed to purchase a house – and this is especially true in CPT markets, with homeownership rates currently at 66% average, but below 40% for young adults, and move-outs currently at a relatively “low” level here.

There is a case to be made here for why this will push demand for CPT up – and this is the reason not only why I am positive on CPT, but on multifamily overall, and why I am happily loading up on these companies whenever they are cheap.

CPT IR (CPT IR)

Based on this, I see the following valuation trend, even though we are at a higher valuation than before for the company, I would still say we’re at an attractive overall price – attractive enough for investing.

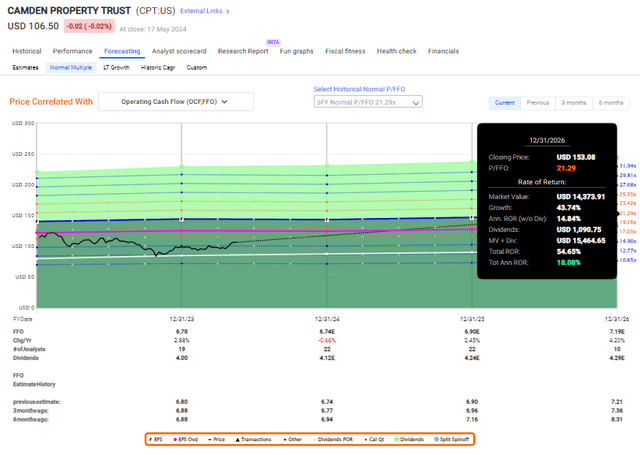

Valuation for Camden shows a 15% annualized premium here, despite an increase in price

Since my last article, we’re actually up quite a bit in valuation, and the company now trades at above 15x P/FFO. This makes us long back for the days when we could “BUY” the company at below 14x P/FFO very easily, with over 4% yield – that’s where my cost basis lies.

Now we’re at 3.87% at a multiple of 15.75x – not as attractive overall, especially not when considering that the current forecasts at a 100% accuracy rate with a 10% margin of error based on a 1-year forecast come to less than 2.5% FFO growth annually until 2026E.

That means until at least 2026, which I by the way consider likely, I would not expect all that much growth out of Camden. This REIT will have to work based on its premium and its fundamentals.

Thankfully, these are good enough to justify this. Even at just 3-5 years, we average at around 20x, which still allows for a 15%+ annualized premium with a pricing forecast of around $150/share.

F.A.S.T graphs Camden Property Trust (F.A.S.T graphs Camden Property Trust)

And again, this company is fairly used to trading at a high premium – so this wouldn’t be strange at all. Even at lower levels of 15-16x, you’re still making at the very least a decent amount of profit, which is sometimes all you can ask for if you really want the safety and income that Camden Property Trust provides.

From a peer perspective, I also consider there to be some upsides here. I would consider Camden to be qualitatively better than ESS and AVB due to the comparatively lower exposure to the West Coast.

As I’ve pointed out before, I also don’t agree with the bearish view or the risks that the tight construction market and challenging logistics will be a meaningful drag on the company’s trends in a way that influences its long-term investment appeal. I also would be careful in overstating the relevance or likelihood of a slowdown in the job market. The strongest bearish argument that I see is heightened cost challenges – but I’m taking stock of these by lowering my forward estimate to 18-19x P/FFO, as opposed to the 20x P/FFO. If we do normalize long-term at 18x P/FFO or so, that would still imply above 14% annually here – and to me, that’s no more than a somewhat annoying rounding error in the long term in such an investment. It doesn’t change my thesis, and there still is enough “punch” in the thesis here for to make it make sense for me.

Given my PT of $130/share from my last article – and I am not changing that price target here, I would consider Camden to be an attractive investment with the following upside and conservative thesis.

Thesis

-

Camden Property Trust is a solid Multifamily REIT with holdings in attractive geographies across the Sunbelt and other areas in the US. The company has an attractive 3.5%+ yield, and trades at what I would view as a compressed overall valuation, though not objectively “cheap.”

-

Still, I do see a potential upside in the company here as an investment. At 18-19x P/FFO that upside is high enough to interest me, and I say the company is a “BUY” here.

-

I give CPT a PT of $130/share, and I’m adding shares here – my position is over 1% both in my private and my commercial account.

Remember, I’m all about:

-

Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

As before, the company is not cheap but still represents a very solid “BUY” in today’s market.

Read the full article here