Here at the Lab, this is not the first time that we have updated our readers on Canadian Solar’s performance (NASDAQ:CSIQ). In November 2023, we anticipated short-term risks, downgrading 2023 and 2024 EBITDA estimates due to module prices and lower sales; however, we maintained a buy rating with the expectation of de-stocking activities in the US and Europe.

For new investors, Canadian Solar is a leader in the solar industry and one of the largest manufacturers of crystalline silicon solar modules. The company’s primary manufacturing operations are located in APAC (China, Thailand, and Vietnam). In addition, the company develops battery storage power plants with a critical backlog.

CSIQ is a vertically integrated player with a flexible wafer-to-module supply chain. This allows the company to adapt to the current market environment quickly. In addition, to support our buy rating recommendation, in mid-June 2023, Canadian Solar completed a carve-out listing of its manufacturing operations on the Shanghai Stock Exchange. Our team followed this with a publication called ‘IPO Catalyst To Price In.’

Canadian Solar Rating Update

Before analyzing Canadian Solar, it is vital to report a MACRO comment on the alternative energy sector. Due to the political uncertainty around the U.S. election and increased concerns about long-term elevated interest rates, the industry is still on the sidelines. On a positive note, our team expects demand for solar projects to remain solid, even considering marginal project delays. This is supported by artificial intelligence evolution with higher demand for data center growth. On the residential solar, we see this current “higher-for-longer interest rate” environment bottoming down in the next 12-18 months, and we believe we are at the bottom of the U cycle.

Why are we still Positive?

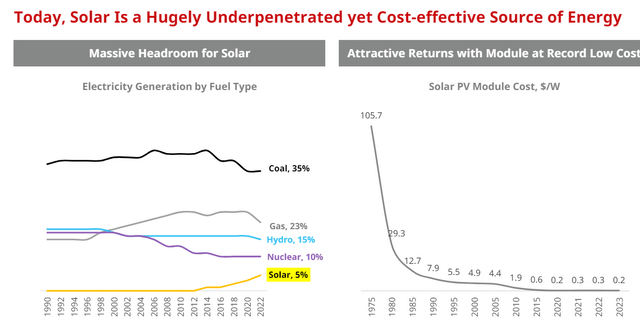

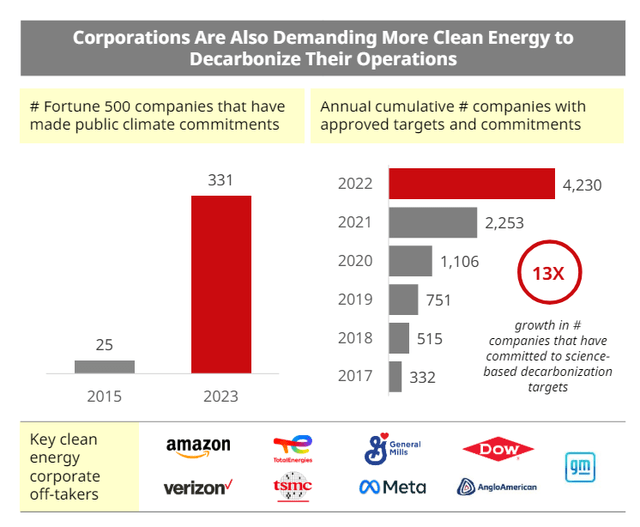

- AI demand will increase energy consumption requirements. Even if AI claims to reduce energy consumption, here at the Lab, we expect a higher electricity demand. According to S&P Global Insights, “global power demand will increase by a third in the next ten years,” specifically a surge in data center energy demand. Our team believes the data center will use renewable energy (Fig 1 -2), favoring Canadian Solar, which meets wafer, cell, and module manufacturing capacity combined with storage product solutions.

- Reassuring investor confidence with better-than-expected results. The company delivered Q1 results ahead of Wall Street expectations. In numbers, the company reported a Q1 EPS of $0.19, supported by top-line sales of$1.33 billion. Looking at the average sell side, we see the Street with an EPS of minus $0.09 with a turnover of $1.29 billion. These better performances were due to higher module shipments of 6.3 GW, slightly ahead of the consensus estimate of 6.1 GW. Canadian Solar’s gross margin reached 19% (the high end of the company’s guidance, previously set at the 17-19% range). This also was above consensus estimates (17.4%). We positively note that this beat was due to lower manufacturing costs as there are transitions to TOPcon. On a negative note, the solar backlog was down by 9% on a quarterly basis, marking the third quarter of sequential decline. However, the company anticipates delivering 7.5-8.0 GW of modules in Q2. This implied a volume growth of 19% on a sequential basis. Regarding the Recurrent Energy segment, the company expects to ship 1.4-1.6GWh of energy storage solution in Q2. This segment has an impressive backlog of almost 56 GWh to develop.

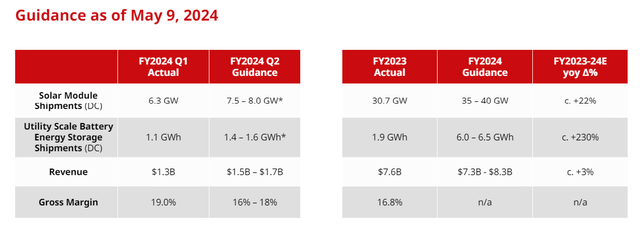

- Prioritizing value over volume. The company lowered its Fiscal Year 2024 guidance (Fig 3). In detail, CSIQ decided to decrease its revenue and shipment outlook as it strategically manages module volume to protect its core operating profit margin in a significantly oversupplied and highly competitive environment. That said, after having listed the Q1 2024 analyst call, top management remains hopeful of improving demand and economies in H2, supported by further reductions to manufacturing costs and price normalization. In number, the module shipment guidance moved from a previous outlook of 42-47 GW to 35-40 GW. These equals lower top-line sales from $8.5-9.5 billion to $7.3-8.3 billion. However, the energy storage shipment guidance remained unchanged at 6-6.5 GWh. This implied a 240% year-on-year growth.

Electricity Generation Split

Fig 1

Electricity Demand from Corporations

Fig 2

Canadian Solar FY 2024 new outlook

Fig 3

Earnings Changes and Valuation

Our previous estimates forecasted an EBITDA of $1.1 billion in 2024. After the Q1 results, we updated our estimates to reflect the company’s performance and revised the Fiscal Year 2024 outlook. Given the lower shipment volumes, we revised our 2024 sales and EBITDA estimates to $7.7 billion and $931 million, respectively. This reflects a reduction in the company’s operating leverage. Canadian Solar market cap is equal to $1 billion. Considering the company’s technical guidance and including the minorities, we estimated a tax rate of 25%.

In addition, to support the project evolution, we slightly increased the company’s interest rate payment. BlackRock recently financed Canadian Solar for a total amount of $500 million. Our interest rate payment is set for $120 million in 2024. Still, in our valuation, we consider CSI Solar Co’s 62% equity stake, which is currently valued at approximately $3.2 billion. Therefore, CSI Solar is presently valued at $0 in the company’s sum of the parts. Here at the Lab, we applied a holding discount of 40%, and we value CSI Solar at $1.2 billion. This is equal to $18.15 per share in our valuation. In addition, we should consider Canadian Solar as a standalone business. In our estimates, we arrived at a 2024 net earnings of $202 million, with an EPS of $2.52. The company currently trades at a P/E of 5.7x or 2.5x our FY24 EPS forecast, adjusting for CSI Solar segment non-controlling interests. This valuation is hard to justify. Even applying a P/E of 4x on the Canadian Solar standalone business, we derive a target price of $10.08 per share. If we add our $18.15 per share CSI Solar Co-investment (with the discount applied), our valuation comes to $28.23 per share. Therefore, we reiterate our buy recommendation.

Risks

Downside risks in our target price include 1) higher production capacity from Chinese competitors supported by subsidies, 2) volatile commodity prices such as polysilicon, which might dramatically impact Canadian Solar’s profitability, 3) a prolonged higher-for-longer interest rate environment that combines with higher solar modules price might impact consumers demand.

In addition, any changes in IRA support could reduce the company’s sales and diluted future earnings. Regulation changes also impact the company; in detail, the AD/CVD petition presents a short-term risk. This is because Canadian Solar needs to change its US shipment strategy. Regarding a company’s specific risk, we also value CSIQ based on SOTP and CSI Solar Co. Ltd.’s current market cap. CSI Solar Co. stock price evolution might significantly impact Canadian Solar valuation.

Conclusion

The renewable energy sector is an underappreciated beneficiary of data center-driven electricity demand growth. Canadian Solar has leverage to benefit from the AI technology wave and wait for residential solar demand to pick up, which is currently offset by higher project financing costs. Here at the Lab, we are encouraged by Canadian Solar’s focus on profitability, and we believe this stock remains a high-risk reward investment.

Read the full article here