Overview

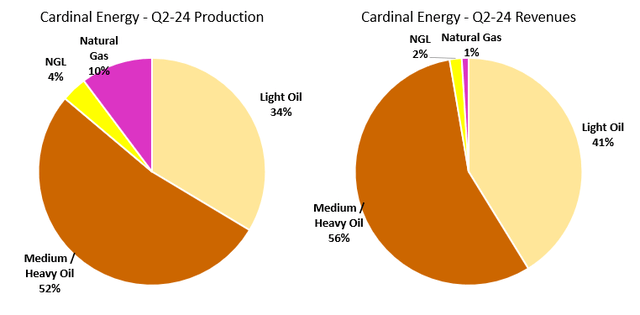

Cardinal Energy (TSX:CJ:CA) is a smaller Canadian oil & natural gas producer, with a production of around 22,000 boe/d. The company has most of its production coming from liquids, where it is split between medium/heavy oil and light oil, as illustrated in the charts below. There are typically few hedges in place, which means Cardinal Energy has substantial exposure to the oil price.

Figure 1 – Source: Cardinal Energy Q2 2024 MDA

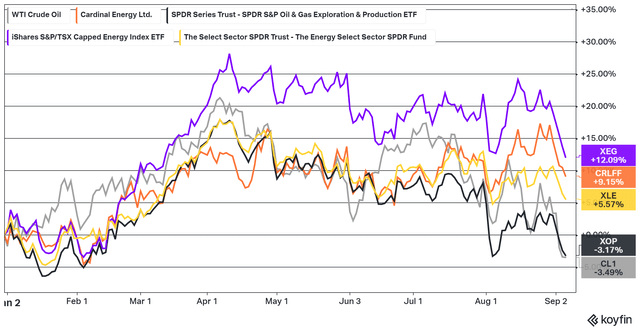

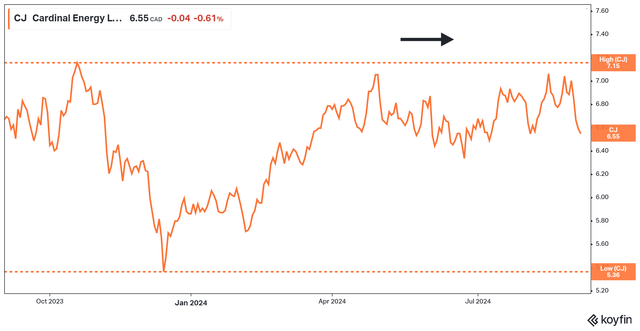

The total return for Cardinal Energy has been +9% in 2024, which is roughly in line with Canadian energy companies, and marginally better than many U.S. peers.

Figure 2 – Source: Koyfin

The WTI oil price is down slightly in 2024, which looks like a minor headwind for the company. However, the oil price has spent much of the year above the current level, which has allowed Cardinal Energy to generate substantial amounts of cash flows.

It is also worth remembering that the Canadian Dollar has weakened slightly against the U.S. Dollar in 2024. So, the WTI price has been marginally better than what the chart above indicates. Another important factor is that the commissioning of the TMX pipeline during Q2 2024 has led to a lower discount for heavy Canadian oil, so Western Canadian Select (WCS) is up 8% in USD terms during 2024 and 10% in CAD. These have been nice tailwinds for Cardinal Energy lately.

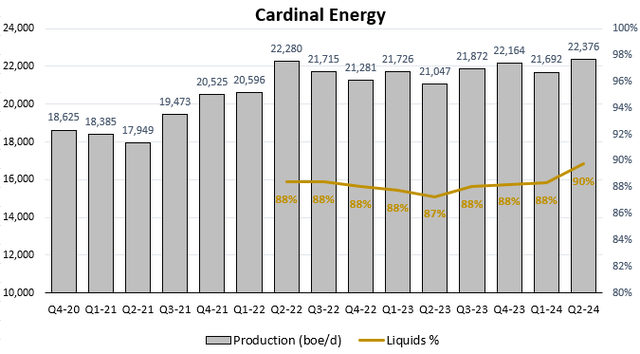

Q2 2024 Result

Cardinal Energy reported a production volume of 22,376 boe/d in Q2, in line with the annual guidance, and up 3% compared to Q1. The good production volume was despite the company curtailing some minor amounts of natural gas production during the last quarter due to low prices. As much as 90% of production and 99% of revenues did in Q2 come from liquids.

Figure 3 – Source: Cardinal Energy Quarterly Reports

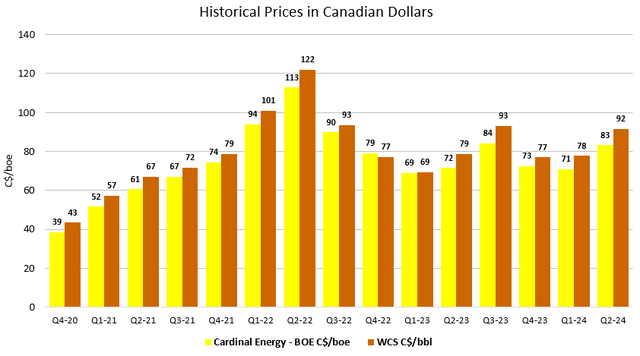

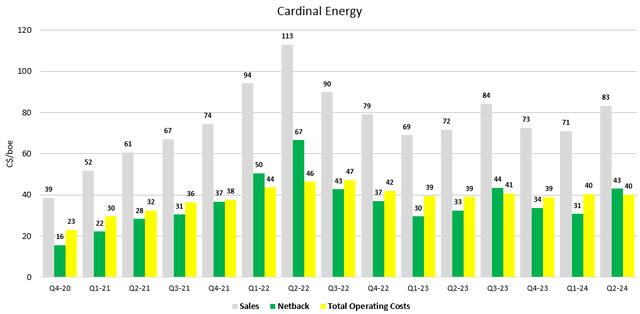

Cardinal Energy has quite a lot of medium/heavy oil production, but also some light oil production. The company normally has a realized sales price slightly below WCS, somewhat dependent on light oil and natural gas prices. In Q2 2024, Cardinal Energy has a realized sales price of C$83/boe, which is one of the better quarterly figures we have seen lately.

Figure 4 – Source: Cardinal Energy Quarterly Reports

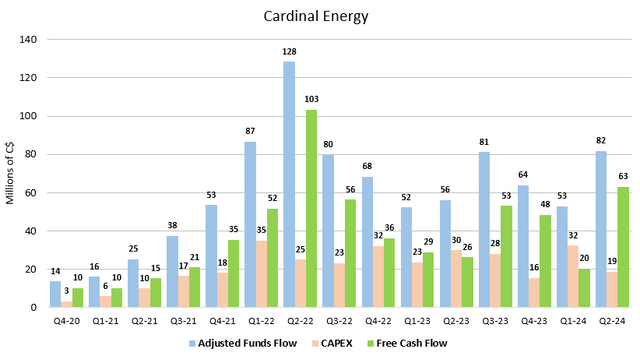

The company reported C$169M in revenues, C$82M in adjusted funds flow, and C$63M in free cash flow during Q2, which was up materially compared to Q1. The higher oil price, weaker Canadian Dollar, and a smaller WCS-WTI differential were tailwinds during the quarter, and the increased production also had an impact.

Figure 5 – Source: Cardinal Energy Quarterly Reports

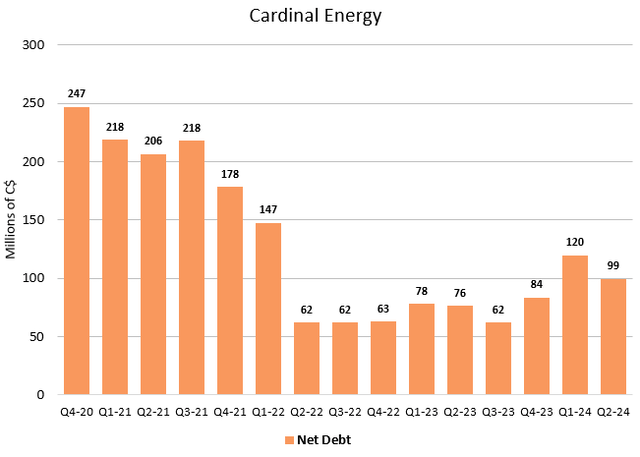

Capital expenditures were relatively low during Q2, both for the regular assets and the Reford thermal project. So, the strong free cash flow caused the net debt to decrease by as much as C$21M during the quarter.

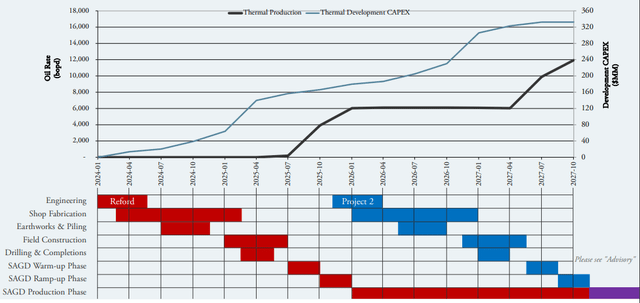

The Reford thermal project continues to progress on time and on budget, with production scheduled to begin around mid-2025. The company has a total debt facility of C$200M, but only C$78M utilized in Q2, so there is a relatively large liquidity position if we were to see weaker energy prices going forward. The good liquidity situation and the fact that the Reford thermal project is so far running on budget, means the oil price would need to persist at current levels or lower for some time for the very attractive dividend yield of 11.0% to be at risk.

Figure 6 – Source: Cardinal Energy Quarterly Reports

During the quarter, Cardinal Energy acquired C$10M worth of exploration & evaluation assets and paid with 1.36M shares, valued at C$7.35 per share. I am normally not a fan of share-based acquisitions by cash flowing companies, but when they are made above the current share price or following a strong stock price performance, it is much less of a concern. The impact was relatively minimal as well, the increase in the share count was less than 1%.

Figure 7 – Source: Koyfin

Netback

Cardinal Energy isn’t the lowest cost operator in the industry, but in the most recent quarter, it had a realized sales price of C$83/boe, which translated to a very respectable netback of C$43/boe.

Figure 8 – Source: Cardinal Energy Quarterly Reports

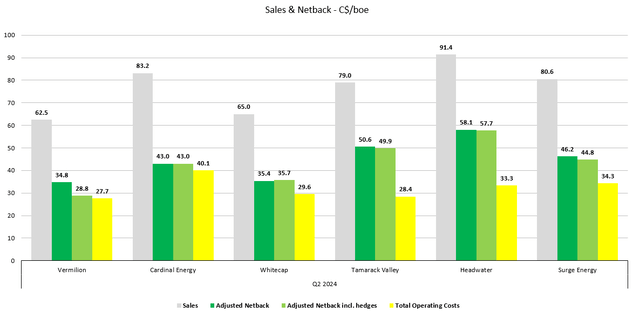

In the chart below we can see that a netback of C$43/boe in Q2 was still quite a bit better than Whitecap Resources (WCP:CA) for example, which is often considered a low-cost operator, even if the number doesn’t come close to the lower cost and liquids rich producers Headwater Exploration (HWX:CA) at C$58/boe.

Figure 9 – Source: Quarterly Reports

Conclusion & Risks

Cardinal Energy is a liquids rich oil producer, with almost all of its production unhedged. So, the company will have substantial upside and downside participation to the oil price.

Today, the company pays one of the most attractive monthly dividends in the industry, with an annual dividend yield of 11.0%. Many industry participants have been critical about the company paying a large dividend while also investing for growth.

In my view, there is little difference between using the credit line to fund the internal Reford thermal project compared to making a debt-financed acquisition. If the oil price gets very weak and stays weak until mid-2025, I do think the company will struggle to maintain the current dividend while also getting the thermal project across the finishing line.

However, if we are talking about more minor weakness for a quarter or two, Cardinal Energy also has some levers to pull, which would reduce capital commitments of the existing assets until we see more cash flow in the back half of 2025, not to mention there is still a lot of room on the credit line.

Figure 10 – Source: Cardinal Energy Corporate Presentation

With that said, there will, of course, be some execution risk of getting the thermal project up and running, which will boost production by +25% in the back half of 2025. If we see any substantial delays or cost overruns, the dividend and share price would be at risk as well.

Cardinal Energy has a free cash flow yield of around 10%, using a WTI price of $70/bbl, provided we don’t include the thermal project, which I expect to be debt financed. At a WTI price of $80/bbl, we are instead looking at a free cash flow yield around 18%.

Keep in mind that this is before any growth from the thermal project, which is expected to boost production and cash flow in the back half of 2025 and also lower costs slightly. So, I consider Cardinal Energy a good buy here, even if there is more execution risk than some of its peers.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here