Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund (“CEF”) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the third week of December. Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

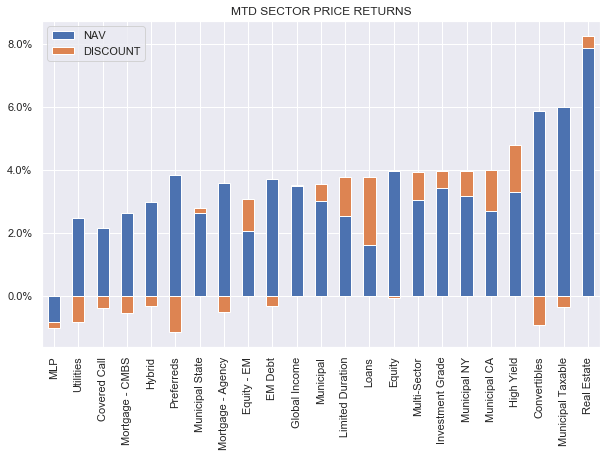

CEFs had a strong week with a total return above 2%. Month-to-date, all sectors but MLPs are in the green with total returns between 2-8%.

Systematic Income

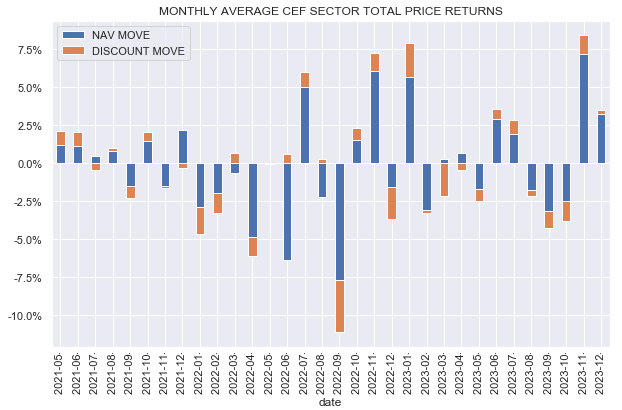

The December Santa Claus rally looks pretty good and follows a stellar November.

Systematic Income

CEFs are at their peak total return for the year of around 8%.

Systematic Income

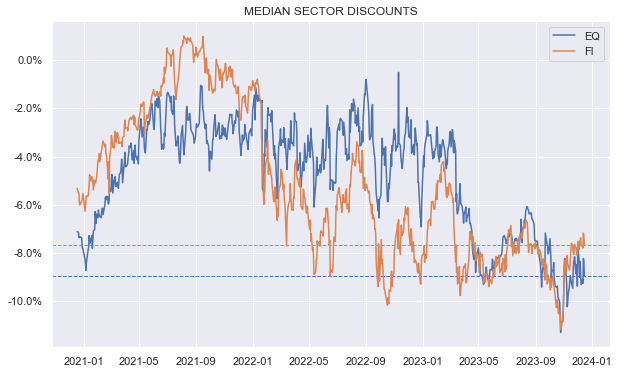

While fixed-income CEF sector discounts have tightened nicely, equity CEF sector discounts remain depressed.

Systematic Income

Market Themes

We are occasionally asked on the service whether covered call CEFs are just more or less equities at a discount. The appeal of covered call CEFs is very obvious – you get to own a portfolio of stocks that you could buy in the market directly but with two main advantages. One, the covered call CEF gives you a much higher distribution rate than the portfolio of individual stocks, and two, the stocks within the CEF are offered at a discount (because, typically, the CEF trades at a discount) whereas the stocks bought directly in the market have no discount. Both of these beliefs are incorrect – we take a look at them individually in this section.

First, although covered call CEFs hold equities they are not really equities funds – they are covered call funds. This is because, while covered call funds do hold stocks (individual or via ETFs), they also sell calls on their holdings.

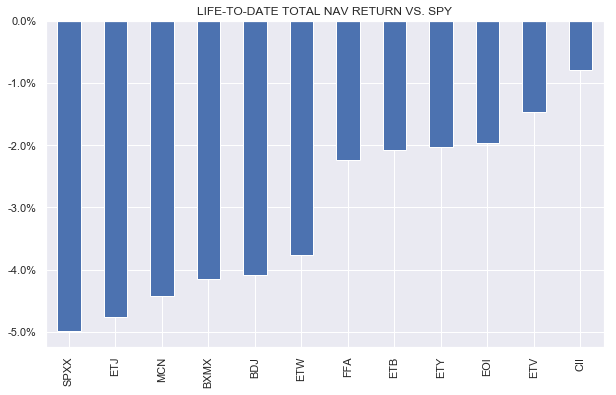

Apart from that important structural element, another reason why covered call CEFs are not “equities” is because they underperform equities. For example, all the SPX-benchmarked covered call CEFs have underperformed the S&P 500 since their inception, ranging from around 1% to 5% per annum.

Systematic Income

Some of that underperformance is due to fees and probably negative alpha, however, another is due to the dynamic of covered call funds. Intuitively it might seem like selling calls on stocks guarantees that a covered call fund will underperform the underlying equity index as a covered call fund gives away the upside in an environment of rising stock prices (which the market has enjoyed since the inception of all the funds above). However, that’s only true if the compensation the covered call funds receive for the calls is less than what the market actually delivers.

This is why it’s important for investors in covered call funds to have a sense of whether today’s market environment favors call selling i.e. whether the volatility risk premium is attractive. This volatility risk premium is, roughly, the difference between implied and realized stock market volatility. The higher the implied volatility is relative to realized volatility, the higher is the volatility risk premium that call selling enjoys.

Covered call funds have tended to significantly underperform their stock benchmarks because the volatility premium has not been high enough. And, arguably, it has not been high enough because of the very popularity of covered call funds. The more sellers of call options there are, the lower is the volatility risk premium. This results in covered call holders not being sufficiently compensated for the strategy.

Another important point is that, intuitively it might seem like in a period of flat stock returns, covered call funds should outperform as they get the additional return from call premiums. However, this is also not necessarily true for 2 reasons. Fund fees, again. And the fact that a flat return period is not one where the stocks are precisely flat each day, rather it’s a period when stocks move up and down and return to roughly the same point. This zig-zagging of returns is generally not good for covered call funds.

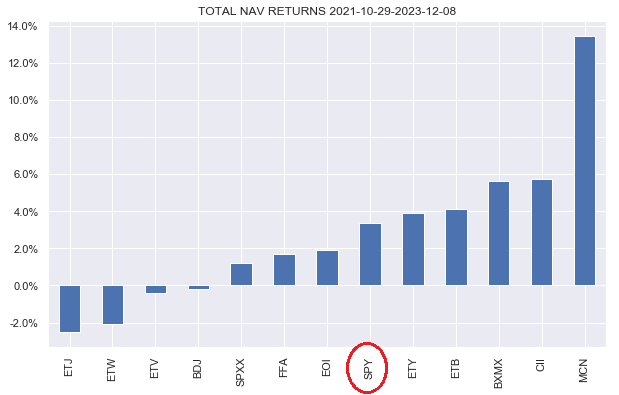

For example, for the return period of 29-Oct-21 to 8-Dec-23, a period over which SPY was flat (in price terms), which should be an absolute lay-up for covered call funds, the majority of SPX-benchmarked covered call CEFs underperformed SPY as the following chart shows.

Systematic Income

In short, covered call CEFs are not “equities” for the simple reason that, apart from the short call position, they have tended to significantly underperform their underlying equity benchmarks over the longer term. This is not to say that individual covered call funds can’t outperform their equity benchmarks or that covered call funds won’t outperform in a down market, but a market environment similar to what we have seen in the past does not favor these funds. This may change in the future but it would require the volatility risk premium to reset higher from historic levels.

Turning to the discount element of the “covered call funds are equities at a discount”, this is incorrect as well. A covered call CEF owns a basket of stocks, however, unlike the basket of stocks, the fund charges investors a sizable fee which can be avoided through direct stock ownership or a cheap fund tracker. The discount that most covered call CEFs (and, in fact, most CEFs) have is not a coincidence – it is a reflection that there is a fee levied on the portfolio of assets which can often be acquired at lower cost directly.

Overall, investors have to be careful in thinking of covered call funds as “equities at a discount” for the basic reason that they don’t deliver equity-like performance and that the discount is there for fair-value reasons.

Market Commentary

CLO Equity CEF, Carlyle Credit Income Fund (CCIF) NAV came in at $8.04 in November, a drop of around 2% from the previous month. This is unexpected given the strength in broader credit markets. That said, other CLO Equity fund NAV changes were mixed – OXLC NAV was up while ECC NAV was down. CLO Equity moves don’t always align with broader credit markets as they are more akin to a trading strategy than a static credit portfolio.

CCIF continues to build out its portfolio so there could have been some trading slippage costs as well as a potential cost to unwind its last legacy position. We should get a better sense of its NAV trajectory and performance relative to other CLO Equity funds over the next year. The discount based on this NAV is 3.5% which is wider than the 3-5% premiums of OXLC, ECC, and EIC, making it an attractive option in its niche sector.

Stance And Takeaways

The loan CEF Apollo Tactical Income Fund (AIF) rose around 9% over the last week, making it fairly expensive overall as well as relative to its sister CEF AFT. The two funds’ discounts have tended to trade in lockstep with each other but have diverged most recently. For this reason, we moved a part of our allocation to its sister fund AFT which remains at an attractive discount.

Systematic Income CEF Tool

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here