Editor’s note: Seeking Alpha is proud to welcome Mahesh Chaganti as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

Investment Thesis Overview

Cencora, Inc. (NYSE:COR), formerly known as AmerisourceBergen, presents a complex investment puzzle for even the savviest of investors. My discounted cash flow (DCF) suggests significant undervaluation and untapped potential, promising future growth opportunities. However, my comparable companies (comps) analysis indicates that COR may be overvalued in relation to industry peers. It seems possible that Cencora’s current stock price is merely driven by optimistic market sentiments rather than accurately reflecting its intrinsic worth, indicating a risk that its price is at its peak and may eventually decline to reflect its true value once market sentiments cool. And to complicate matters further, in February 2024, Cencora experienced a significant cyberattack that exposed sensitive patient data, including names, addresses, health diagnoses, medications, and prescriptions. This breach affected over 540,000 individuals and involved major pharmaceutical companies like Bayer, GlaxoSmithKline, and Novartis. Despite the severity of the breach, news of it has had a negligible impact on the stock’s price so far. Nevertheless, given the mixed signals from my analyses and the risk of future negative consequences due to the data breach, I believe that a rating of “HOLD” or “SELL” appears more appropriate than “BUY” at the moment.

Company Overview

Based in Conshohocken, Pennsylvania, Cencora is a prominent global provider of pharmaceutical services. It plays a vital role in the healthcare supply chain by offering comprehensive solutions in pharmaceutical distribution, logistics and data analysis. Cencora operates through two main segments: U.S. Healthcare Solutions and International Healthcare Solutions. The former delivers a wide range of products including pharmaceuticals, over-the-counter healthcare items, home healthcare supplies and equipment to various clients such as hospitals, health systems, pharmacies (both retail and mail-order), medical clinics and long-term care facilities. Moreover, it provides pharmacy management services, staffing solutions, consulting services, supply management software, packaging solutions, clinical trial support services, and sales force services for manufacturers. On the other hand, the International Healthcare Solutions segment focuses on offering pharmaceutical wholesale services and global commercialization support to pharmacies, doctors, health centers, and hospitals primarily in Europe. This segment also specializes in transportation and logistics services for the biopharmaceutical industry. Cencora reported revenue of $262 billion during fiscal year 2023 and has around 46,000 employees globally.

Industry Overview & Competitive Analysis

The pharmaceutical distribution sector is fiercely competitive and tightly regulated, marked by significant entry barriers, complex logistical networks and strict regulatory standards. The industry is experiencing significant changes due to various key trends, notably the progress of digital and analytical tools that enhance operational efficiency and supply chain robustness. The increasing adoption of digital technologies like AI and automation is expected to continue driving operational optimization and cost reduction. Moreover, the emergence of novel treatment methods such as mRNA vaccines, gene therapies and antibody drug conjugates is reshaping the pharmaceutical landscape by demanding sophisticated distribution and logistics capabilities to meet their unique storage and transportation requirements.

Cencora faces stiff competition from major players like Cardinal Health, McKesson Corporation, Henry Schein, Patterson Companies and Owen & Minors. The industry is heavily consolidated, with just three companies, McKesson, Cencora and Cardinal Health, holding U.S. market shares of around 34-36%, 31-33% and 25-26%, respectively, collectively controlling around 90-95% of the market. McKesson, as the largest player in this arena, has made substantial investments in AI and automation to enhance logistics management efficiency. Noteworthy collaborations include partnering with Accuweather for 24/7 meteorological services, a testament to their dedication to ensuring supply chain resilience. Cardinal Health is known for being proactive in adopting innovative technologies and forming strategic partnerships. They have collaborated with Zipline for drone delivery, Ember Technologies for cold-chain solutions, and companies like FourKites for AI and machine learning. Owens & Minor uses its specialized knowledge and agility to stay competitive, focusing on specific therapeutic areas to offer tailored solutions with lower overhead costs than larger rivals. In the midst of this tough competition, Cencora has made a mark by significantly expanding its global footprint through acquisitions, most notably acquiring Alliance Healthcare from Walgreens. Overall, I would say that the pharmaceutical distribution industry is characterized by high market concentration, strict regulatory standards, the growing importance of investing in cutting-edge technologies, and the constant need to adapt to meet the demands of a dynamic global market.

Financials

In my assessment of Cencora’s financials, I am concerned about the valuation metrics, particularly the price-to-earnings (P/E) and price-to-book (P/B) ratios, which I believe indicate the stock might be overvalued. Currently, Cencora’s P/E ratio stands at 25.4, well above its five-year quarterly average of 15.6. This elevated P/E ratio could suggest that the stock is priced too high relative to its earnings, making it less attractive for investors who follow a value-oriented investment strategy. Likewise, the P/B ratio stands at 42.8, which is also too high for investors seeking undervalued stocks. Cencora has shown impressive revenue growth, from $213.99 billion in 2021 to $276.54 billion in 2024. However, the rise in the company’s stock price and market valuation has outpaced these fundamentals by a substantial margin. From the perspective of investors aiming to “buy low and sell high” such as myself, it seems that Cencora’s current stock pricing may be more influenced by optimistic sentiments towards the market at-large rather than reflecting Cencora’s intrinsic value accurately, presenting a potential risk of entering at a peak. Moreover, the significant increases in market cap and revenue over the years have not been accompanied by proportional increases in fundamental financial health metrics such as EBITDA, which has grown at a modest average rate of 7% annually since 2021. The high leverage, indicated by a debt-to-equity ratio of 4.85, suggests that a substantial portion of the equity value is leveraged, potentially inflating metrics like ROE, which is currently at an exceptionally high 213.15%. In summary, while Cencora is growing and maintaining a strong industry presence, I believe that the current stock valuation is too steep for value investors. The high P/E and P/B ratios, in my view, are red flags for those seeking undervalued opportunities.

Valuation

Despite all of the potential negatives I mentioned before, one significant positive for Cencora is that, even under the most pessimistic assumptions, it still appears at least moderately undervalued according to DCF analysis. In fact, I believe that one of Cencora’s strongest financial selling points is its consistently large and positive free cash flow. In 2023, the company generated over $3.4 billion in free cash flow, up from $2.2 billion in 2022. The following table shows Cencora’s annual FCF each year since 2009:

|

Year |

Free Cash Flow (FCF) (in USD millions) |

|

2023 |

$3,452.98 |

|

2022 |

$2,206.77 |

|

2021 |

$2,228.37 |

|

2020 |

$1,873.73 |

|

2019 |

$2,035.10 |

|

2018 |

$1,083.08 |

|

2017 |

$1,037.74 |

|

2016 |

$2,713.88 |

|

2015 |

$3,690.64 |

|

2014 |

$1,200.20 |

|

2013 |

$585.68 |

|

2012 |

$1,172.16 |

|

2011 |

$1,012.67 |

|

2010 |

$932.42 |

|

2009 |

$638.03 |

Source: Macrotrends

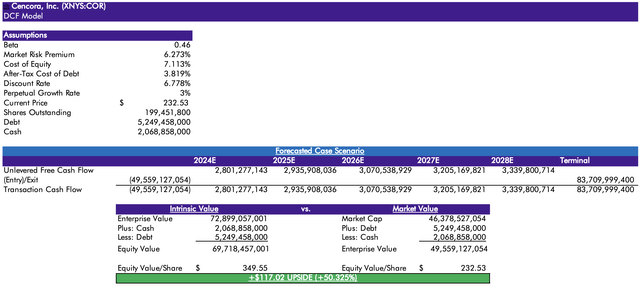

I forecasted Cencora’s free cash flow for the next 5 years using its historical FCF data and linear regression. My model assumes a market risk premium of 6.273%, which is slightly higher than usual but apt for a cautious investor like myself, and a perpetual growth rate of 3%. The model indicated an intrinsic value per share of $349.55, suggesting a potential upside of $117.02 (+50.325%):

Author’s Calculations

However, please keep in mind that this DCF model is highly sensitive to the beta used in calculating the cost of equity, and I have found conflicting information regarding Cencora’s beta. According to Refinitiv’s database in Excel, Cencora’s beta is 0.46, Yahoo Finance lists it as 0.48, and Alpha Spread reports it as 0.88. I used Refinitiv’s beta of 0.46 in the model above. If I used a beta of 0.48 in the model, COR’s intrinsic value per share would drop to $338.03, indicating a $105.5 upside (+45.372%), and with a beta of 0.88, it would drop further to $209.45, indicating a -$23.08 downside (-9.927%). Additionally, when using a beta of 0.46, the WACC comes out to 6.778%, which seems lower than other estimates. GuruFocus calculates a WACC of 8.26%, and Finbox estimates it at 8.00%. If I used a WACC of 8.00% in the model, the intrinsic value per share would drop to $260.94, indicating a $28.41 upside (+12.219%), and with a WACC of 8.26%, it would drop further to $247.39, indicating a $14.86 upside (+6.392%). Overall, while the DCF analysis suggests that COR is undervalued, it is highly sensitive to the WACC used. The varying information regarding COR’s WACC means that even minor changes can significantly affect the potential upside. Therefore, please take this DCF analysis with a grain of salt.

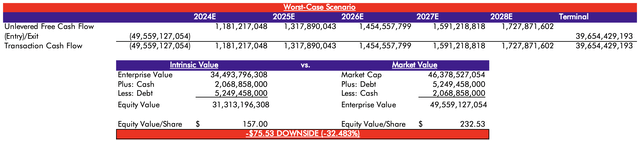

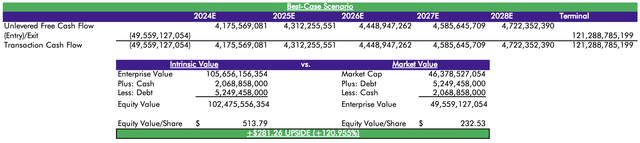

Furthermore, my worst-case scenario and best-case scenario DCF models indicate a downside of -$75.53 (-32.483%) and an upside of $281.26 (+120.955%), respectively:

Author’s Calculations

Author’s Calculations

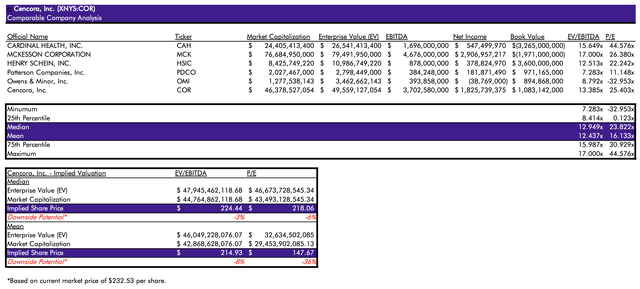

However, my comps analysis for Cencora paints a far darker picture. When using the median Enterprise Value-to-Earnings Before Interest, Taxes, Depreciation, and Amortization (EV/EBITDA) ratio of COR and its peers, the implied share price is $224.44, indicating a -3% downside. Using the average EV/EBITDA ratio, the implied share price is $214.93, indicating a -8% downside. When using the median P/E ratio, the implied share price is $218.06, indicating a -6% downside. Finally, when using the average P/E ratio, the implied share price is $147.67, indicating a -36% downside. In all cases, COR is moderately overvalued compared to its current price of $232.53.

Author’s Calculations

In case you are concerned about OMI’s outlier P/E ratio of -32.953x unfairly skewing the overall results against COR, excluding OMI gives COR an implied share price of $232.53 using the median P/E, indicating no upside (0.00%), and $237.54 using the average P/E, indicating a mere 2% upside. In either case, the comps analysis suggests that COR is moderately overvalued or, at best, fairly valued, with very little potential upside. Furthermore, if you consider excluding this outlier, it would be fair to also exclude all outliers, including CAH’s unusually high 44.576x P/E ratio, and removing this would make COR even more overvalued.

Overall, the valuations are ambiguous. While the DCF analysis suggests solid upside potential under certain assumptions, the comps analysis indicates that COR may be overvalued or, at best, fairly valued.

Mispricing

In summary, despite my DCF model indicating undervaluation, considering my comps analysis and COR’s abnormally high P/E, P/B, and EV/EBITDA ratios, I believe that COR is either fairly valued or overvalued. I believe that the main reason for this overvaluation seems to be that Cencora’s current stock price is driven by optimistic market sentiments rather than accurately reflecting its intrinsic worth. The broader market’s upward trend has naturally boosted COR’s stock, but I see a significant risk that COR’s price is at its peak and may eventually decline to reflect its true intrinsic value once the market sentiment cools. I acknowledge that I could very well be wrong and that there are many signs in COR’s favor, but given that there are so many other stocks out there that are clearly and unambiguously undervalued by virtually all metrics, I don’t believe that investing in COR would be prudent at the moment.

Risks

Investing in Cencora comes with several potential risks that I believe investors should consider. One significant issue is the data breach the company experienced in February 2024. This incident resulted in unauthorized parties gaining access to Cencora’s information systems and stealing personal data, including names, addresses, health diagnoses, medications, and prescriptions of hundreds of thousands of individuals from at least 27 pharmaceutical and biotechnology companies. While Cencora has not detected any public disclosure or misuse of the stolen data, it has offered affected individuals two years of free identity protection and credit monitoring services and has strengthened its cybersecurity defenses to prevent future breaches. Despite the severity of the breach, news of it has had a negligible impact on the stock’s price so far. However, I am concerned that the small impact on the stock price so far does not rule out potential future fallout, including legal challenges, regulatory scrutiny, financial penalties, and loss of client trust. Such a serious security lapse, which compromised sensitive patient data, adds a layer of risk that could have long-term repercussions on Cencora’s market position.

Additionally, Cencora is entangled in numerous lawsuits related to its alleged role in the opioid crisis. The company, along with other major drug distributors, reached a comprehensive settlement agreement in 2022 to address the majority of opioid-related lawsuits filed by state and local governments. This settlement involves a payout of up to $6.1 billion by Cencora over 18 years, aiming to provide relief to communities affected by the opioid epidemic. However, ongoing litigation and the potential for future legal challenges continue to pose significant risks.

Beyond these specific issues, the pharmaceutical distribution industry is highly competitive, requiring constant adaptation to changing market conditions, regulatory requirements, and advancements in technology. Economic factors such as inflation, interest rate changes, and global economic instability could also affect Cencora’s financial performance. Additionally, as I mentioned before, Cencora’s high P/E, EV/EBITDA, and P/B ratios should be cause for concern, indicating the stock may be overvalued and potentially at its peak. Overall, I believe Cencora faces a variety of cybersecurity, regulatory, legal, industry, economic, and financial risks that investors should be cautious of.

Conclusion

In conclusion, while Cencora offers promising growth opportunities, its current valuation raises concerns. The mixed results from my DCF and comps analysis suggest ambiguity, with potential undervaluation on one hand and possible overvaluation on the other. The data breach adds another layer of risk, highlighting potential future legal and regulatory challenges. Given these factors, along with the competitive and economic pressures in the pharmaceutical distribution industry, I believe that there are more clearly undervalued investment opportunities available. Thus, adopting a cautious stance on Cencora appears prudent at this time.

Read the full article here