Cenovus Energy Inc. (NYSE:CVE) has a strategy that remains largely intact. What changed in the latest quarter was the Toledo Refinery and the Superior Refinery are now heading in a cash flow positive direction after a shut-down. That means that the company has more capacity to upgrade the thermal production in the future while the two refineries are no longer cash flow drains. There will, therefore, be more cash available in the future to repay debt and distribute to shareholders.

Underlying the growth strategy has been a little noticed strategy to get rid of dysfunctional partnerships. When I first began coverage of the company, the company was nearly all partnerships. Clearly, that is not the case now. The remaining partnerships appear to work. That was also not the case back in the beginning of the journey.

Cash flow has increased tremendously from back then, and it is less cyclical thanks to the additional refining and upgrading capacity.

Major Immediate Issues

The Superior refinery issues during construction were largely covered by insurance. But it was still an idle asset that was not earning a return until the startup process was complete. The story may have been similar with Toledo as well. Insurance though, never covers everything (it would seem) though it is a big help.

In addition to this, management now completely controls the Sunrise thermal area and is working to get costs in this area down. When this is successful, there is likely to be still more cash flow on the way.

The growth of the past few years is likely to slow in the future. But well-run thermal companies generally produce a lot of cash because the upstream production of thermal oil often requires large upfront cash investments. Therefore, these companies generate decent cash flow even if they lose money from the depreciation of those initial costs.

As a result, an integrated thermal producer like Cenovus can meet the market demand for some dividends while still growing the company. Growth here will likely come from a combination of organic growth, an opportunistic acquisition or two, and optimization of the operations already acquired for (likely) years to come.

Cenovus is a newly integrated company. Therefore, management will have to show that the whole company can produce the planned profits along with the benefits of integration. That will take some time. It should also result in a wider price-earnings ratio over time.

Significant Changes

One of the biggest changes was the decline of purchased product.

This should be expected, as the original Cenovus sold product from upstream production to customers. The issue was that thermal is a discounted product and that discount did widen from time to time (usually during times of pricing weakness).

The refining capacity that the company now has allows the company to upgrade the thermal product to more valuable products while avoiding the risk of selling the upstream production to a large extent. Now refining gets the benefit of cheaper thermal rather than a customer when the discount hurts the price of thermal oil.

(Note: This Company reports in Canadian dollars unless otherwise noted.)

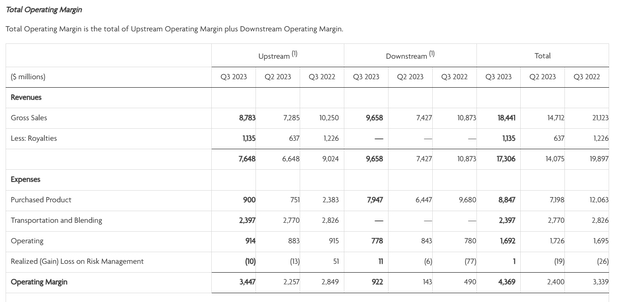

Cenovus Energy Summary Of Operations (Cenovus Energy Third Quarter 2023, Earnings Conference Call Press Release)

Obviously, the plan from the start was to reduce the exposure of the thermal production to the marketplace. The thermal market has been particularly volatile in a generally volatile industry. Sometimes this volatility caused some noticeable losses. Profits can really get hurt when the discount widens. All of this made the previous considerations first stated, particularly urgent because all the worries were happening with an exclamation point.

Clearly, this issue has been reduced with the acquisition of more refineries and the restart of the refineries that were shut in. The result is shown above in a dramatic operating margin increase.

In the future, profits will still largely depend upon the volatility of posted oil prices. However, there will be a large avoidance of the thermal oil situation that was not the case in the past. The refined products due relate to the price of oil. But it is a very different margin “ballgame” than was the case with just an upstream operation. That should lead to a valuation similar to the more established Canadian integrated majors in the future. That is clearly not the case right now. Companies like Suncor (SU) and Imperial (IMO) have a far better valuation and a longer integrated operating history.

However, Cenovus is beginning to show margin improvement over a very tough third quarter comparison that few companies in the industry can match.

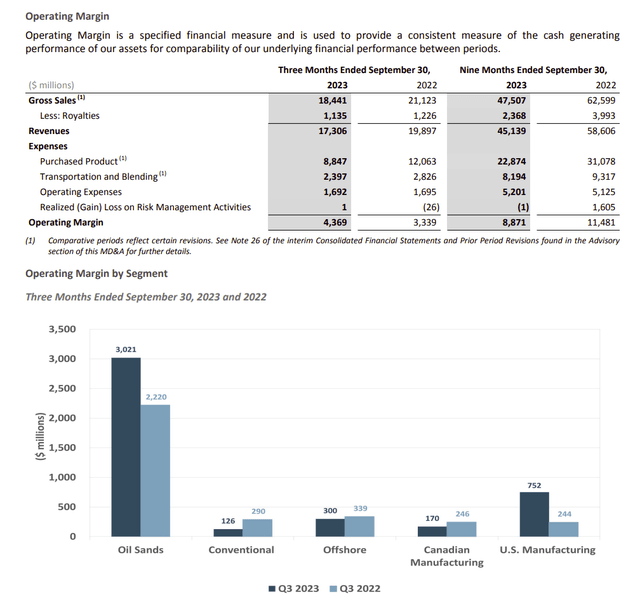

Cenovus Energy Operations Summary Details (Cenovus Energy Third Quarter 2023 Management Discussion And Analysis)

Management attributes most of the improvement to refining during the discussion about the third quarter. This gives the market a “heads up” that things will be different (and better) going forward. At least some of that improvement is permanent from the idea that the thermal oil production is now mostly not sold to third parties but instead goes to the refineries owned by the company. Therefore, the discount that used to be realized is now part of the refining profits.

As the market price for thermal changes, that upgrade process to more valuable products will show the additional profit either in the thermal area when pricing is strong or in the refining area when the pricing is weak. The key is the company is now reporting that profit in different areas of the company rather than having some of that profit go to third parties that used to upgrade the product.

The true value of integration can be disputed in that some will argue where the profit is. But the overall picture is the company has a profit it did not have before the acquisition of the refineries and that profit includes an “upgrade” in addition to what many think of as refining margins. This is a big reason why thermal producers often do not survive as independents. For thermal producers, integration is essential to get that “product upgrade value” because it is often significantly more than the refining process that uses exclusively light oil.

Going Forward

The process of optimizing some rather large acquisitions since the company purchased the ConocoPhillips (COP) partnership interest will likely take years. All the acquisitions were relatively large compared to what the company was years ago as mainly an upstream company with a small downstream interest.

Therefore, it is quite possible that cash flow and earnings growth will exceed revenue growth for some time to come. The third quarter results give a hint that some material improvements are on the way (still).

Some things like midstream agreements take years to unravel or rearrange to suit new circumstances.

This is likewise probably true not only for refinery feedstock but also optimizing the refinery itself for the feedstock that the company has available for the refining system.

Another huge cost savings is that the company recovers more condensate than it did when it sold the oil and had to purchase the condensate used to make the oil flow in pipelines to third parties. Now company owned refineries recover that condensate so that it is available to the upstream part of the company to reuse. Condensate alone used to lower the sales price roughly 25%. So, the increase in recycling is probably a huge cost savings to a newly integrated company like this one.

While the company remains a strong buy. The immediate benefits shift to margin expansion even though there will be slow organic growth and an occasional opportunistic acquisition.

There should be a material increase in profitability that would allow for superior valuation of the earnings in the future. Typically, the market wants proof. But Cenovus Energy Inc. management will not have to do anything spectacular to provide that proof.

Read the full article here