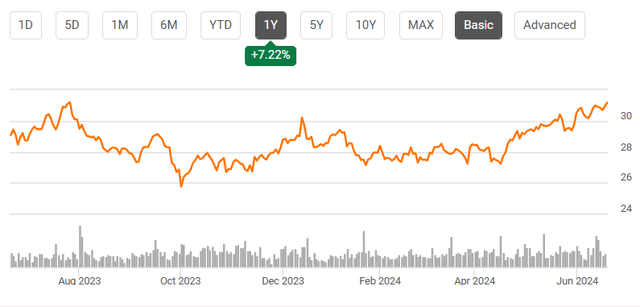

Shares of CenterPoint Energy (NYSE:CNP) have been a modest performer over the past year, rising just 7%, and lagging the broader market as elevated interest rates have weighed on utility valuations. However, shares have been rising steadily since reporting solid Q1 earnings and sit near a 52-week high. I last covered CenterPoint in March, rating shares a “buy,” and since that recommendation, CNP has returned 12%, ahead of the market’s 6% rally. I remain bullish

Seeking Alpha

In the company’s first quarter reported on April 30th, CenterPoint earned $0.55 in adjusted EPS, beating consensus by $0.02. This came despite a 5% decline in revenue to $2.62 billion. Earnings rose 10% from last year, with $0.08 of higher rates and a $0.02 weather benefit offsetting a $0.04 interest expense headwind. While weather was better than last year, it has still been a milder than average winter. Given climate change, that may be a persistent trend.

In the first quarter, revenue fell by $159 million, which may at first be surprising given more favorable weather and the fact it continues to grow its Houston customer base 1-2%. This decline was entirely driven by lower commodity prices. CNP’s energy costs fell by $291 million given weaker natural gas. CNP itself does not take commodity risk, instead passing price changes on to customers. As such, revenue was lower, but this has no P&L or cash flow impact. Ex-energy, revenue rose by over $130 million, consistent with its upper single digit rate base growth.

During the quarter, it achieved about a $5 million revenue increase from its Texas Gas rate case, earning a 9.8% return on equity, with the rate increase effective on December 1. This is notable because this 9.8% return is above its average 9.64% allocated equity return, speaking to the friendly regulatory environment as Texas incentivizes utilities to invest in improving the resiliency of the grid after challenges in recent years.

CenterPoint has also developed a strong relationship with regulators thanks to its strong cost control. Its average monthly bill in Houston has been flat for 10 years at $49, and this rate increase will raise bills by less than 0.1% while supporting $500 million of incremental capital. Regulators and politicians both like low utility costs, and it is easier for a utility to recover costs when customer bills are not rising.

As discussed in my prior article, CNP continue to be a beneficiary of a growing population in its key Texas market as it now has 2.8 million customers in the Greater Houston area. Texas is enjoying positive population dynamics, given net migration from other states, and I expect this trend to continue. Its growing customer base allows it to spread its rate base across more customers, mitigating the per-customer impact of its capital spending. On top of this, CNP continues to be disciplined in its expense management. I expect operating & maintenance spending to rise by no more than 2% this year.

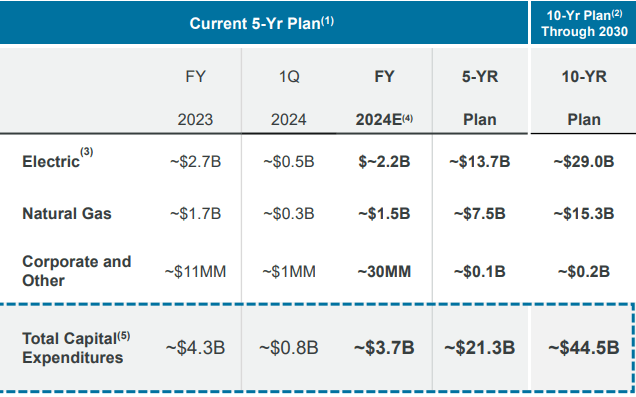

For a utility to grow, it needs to continue to expand its rate base—the value on which it earns regulatory returns. Alongside results, management reaffirmed guidance of 8% EPS growth this year and then 6-8% growth through 2030. Dividend growth should track EPS growth. This implies $1.61-$1.63 in 2024 EPS. Underpinning this growth is a targeted 8-10% annual increase in the rate base due to a $44.5 billion 10-year cap-ex plan.

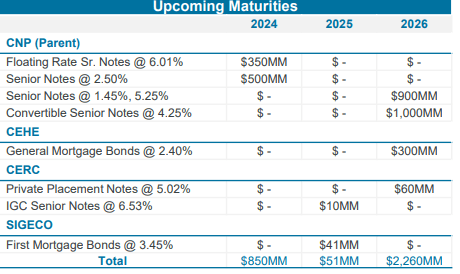

Now, in the near term, I view its 2024 EPS estimate as highly credible. We have passed through the most volatile weather quarter, and its rate case profile for 2024 is largely set. This should create significant visibility to near-term earnings. Now, as you can see below, it does have some near-term maturities on its $18.1 billion debt load. However, it has hedged interest rate risk on near-term maturities it will be refinancing, again reducing volatility for this year’s earnings. I would also highlight its current 14.6% FFO/Debt ratio is consistent with its 14-15% target. Additionally, about 90% of its existing debt is fixed-rate or hedged, further reducing near-term rate sensitivity.

CenterPoint Energy

Now, in the longer term, growing its rate base in an accretive fashion is necessary to achieve targets. As you can see below, it has a $44.5 billion 10-year plan, including $3.7 billion this year. There was $800 million of Q1 cap-ex spending, and this should ramp towards $1 billion/quarter over the course of the year. Because of this large capital program, it will also be a perennial equity issuer. That is why its 8-10% rate base growth is expected to translate to 6-8% annual EPS and dividend growth.

CenterPoint Energy

This year, it aims to do $250 million of equity issuance, and it has already completed over 75% of this total, reducing near-term needs and market risk. Much of this capital program is focused on expanding capacity in Houston to meet demand, as well as improve the reliability of its system. In fact, it has filed a three-year plan to spend $2.2 billion to $2.7 billion over 2025-2027 on improved resilience.

At the high end of this plan, its capital program would grow to $45 billion rather than $44.5 billion. Given the growth in Texas and legislative support to improve grid resiliency, I do not see the primary risk being able to achieve its capital spending target; the risk is more on financing it in an accretive fashion. Importantly, if it does pursue this incremental $500 million of spending, it is seeking $100 million of grants as well as DOE loans, which can reduce funding costs by over 1%. Absent these measures, it would likely require some incremental equity issuance.

Importantly, beyond raising equity, CenterPoint has made progress repositioning its equity base in more favorable ways. Most notably, expects to close the sale of its Louisiana and Mississippi operations by Q1 2025. As discussed in March, this sale was for $1.2 billion or 32x earnings and 1.55x their rate base, just a 5% discount to all of CNP. It will net $1 billion of proceeds, which it can use to fund growth in Houston, where it earns a higher regulatory rate of return and has better growth prospects.

Additionally, it is important to note that 80% of its capital spending leads to interim recovery, rather than being tied to multiyear rate case. This increases my confidence that shareholders will see benefit from the capital spending. Its electricity demand growth has also largely been tied to a rising residential population and associated industrial activity, leaving CNP less dependent on lower margin data center usage to power demand growth than other utilities.

CNP continues to execute well and is benefitting from its favorable geographic position. Additionally, its front-loaded equity issuance and well-priced acquisition support the financing for its capital spending. Now, with a 2.6% yield, and a 6-8% long-term growth profile, CNP can deliver an 8.6-10.6% capital return. However with interest rates likely near a peak, and the potential to expand its capital budget while taking advantage of government incentives, I am increasingly confident CNP can deliver at the top-end of guidance, if not slightly higher.

This leads me believing CNP is still positioned to deliver 10-11% long-term returns even after its recent rally. I view that as attractive for dividend growth-oriented investors, and as such I continue to view CNP as a buy. Its favorable growth profile will support rising dividends and EPS, and I remain a buyer.

Read the full article here