Investment thesis

Cerence (NASDAQ:CRNC) is a leading provider of conversational AI solutions for the automotive segment. The company works with nearly all major OEMs globally and has a market penetration of 54%. Its products span from Voice Assistant solutions to driver monitoring systems and its revenue comes from three segments namely Licenses, Connected Services and Professional Services. Its latest product offerings have seen a significant boost in performance due to the introduction of Gen AI and the adoption of Large Language models. The company’s value proposition versus its competitors is its ability to offer a white label solution where it can plan and build customized solutions together with the respective OEM.

The share price has declined sharply since the company cut its full year guidance and withdrew its previous financial targets for the period between 2024 to 2026. The future margin profile remains uncertain as management attempts to adjust the company’s cost structure to the latest growth expectations. I have identified significant risks associated with an investment in Cerence at present. However, I also consider the shares to be attractively valued based on my estimates. Given this balanced risk-reward scenario, I am currently rating it as a Hold until I gain further clarity.

Recent developments

Q2 revenue came in at $67.8 million and was above the high end of management’s guidance. This outperformance was however due to certain unplanned items, without which revenue would have ended up near the low end of guidance. Adjusted EBITDA for the quarter was nearly breakeven, while operating cash flow was $1 million.

The reason for the negative share price reaction following the earnings release was reduction in full year guidance and the updated framework for FY25. FY24 guidance was lowered by $40 million, representing a decrease of approximately 11%. Furthermore, the company withdrew its mid-term financial targets. The main reason cited for this reduction was the lower production expectations for some of its OEM customers versus the prior forecasts. Additionally, the rollout of some of its IoT related products had been slower than anticipated due to delays and slowdowns in automotive production. Its 5-year order backlog, however, remained solid at above $1 billion.

Shortly thereafter, the company’s CFO resigned, having been hired just two months earlier. The company has managed to hire an interim CFO while they search for a permanent hire. On the Q2 earnings call, the company’s CEO outlined the company’s strategy going forward stating:

Moving forward, we are focused on transforming the company to be in a position to deliver on our Generative AI and large language model product roadmap and deliver improved financial results. We understand that our cost structure is not properly aligned with our near-term revenue outlook and we will be taking action to address this, while also making sure we have the right balance to drive the success of our NextGen AI platform currently in development.

Expectations going forward

Cost reduction efforts

The effort to balance its cost structure with the latest outlook for revenue growth remains the highest priority for the management team. The benefits from these cost reduction measures will likely be reflected in the company’s financials only in FY25. In a recent investor conference, its CEO highlighted that an external firm has been brought on to support with this initiative.

Growth drivers

A majority of the company’s revenue for the next two years is expected to come from its solid order backlog. Additionally, the company has made solid progress recently by signing six contracts for its Generative AI product offerings since showcasing them at CES. Since these solutions can be delivered through the cloud, they can be introduced to both new and existing vehicles. Connected services is a key growth driver for the company as more services can be offered on the cloud at increasingly higher pricing tiers. Management remarked that new cars using Cerence’s connected services increased 23% on a trailing 12-month basis. The contribution from connection services to the company’s revenue is expected to show up with a lag, as explained by its CEO when he said:

Because these products are cloud centric, their revenue contribution will be taken as connected services is first booked into deferred revenue and then amortized into revenue over the subscription period. This means in the short-term, any success of our new products will be insufficient to make up for the expected revenue shortfall resulting from the factors I outlined earlier in the call.

Debt concerns

The company’s balance sheet consists of $108 million in cash and $278 million in debt. According to its latest Annual report, close to $90 million of this debt is due in June next year. Despite its current cash balance being sufficient to cover the debt repayment, this situation presents a financial risk if the company burns cash in upcoming quarters due to its restructuring efforts.

Thoughts on valuation

Q2 Investor presentation

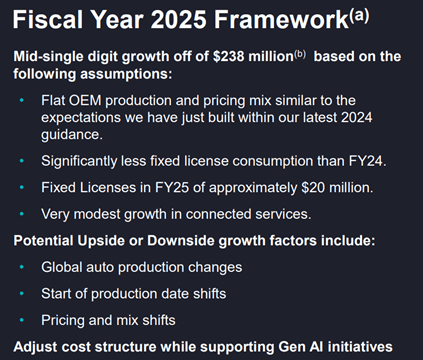

Valuing the business in its current state with a high level of uncertainty can be quite challenging. In order to arrive at a fair valuation for the company, I will refer to the recent guidance framework outlined during the Q2 earnings call and summarized in the slide above from its latest investor presentation. I will also make prudent assumptions with respect to future margins. The current revenue run-rate for the business is $238 million with mid-single digit growth expected next year as explained by the company’s previous CFO when he said:

In addition, if you assume $20 million in new fixed licenses in fiscal year 2025 and very modest growth in our run rate connected services, it would be reasonable to anticipate mid-single-digit growth off of the new estimated run rate of $238 million.

Following this guidance and in line with analyst estimates, I expect 5% revenue growth in FY25, which would result in total revenue of $250 million. After the cost reductions that the company is undertaking, I expect that it will be able to reach steady state adjusted EBITDA margins of around 15%. I believe this to be conservative, considering management’s previous guidance called for adjusted EBITDA margins between 28-32%. This would imply that adjusted EBITDA for FY25 would be approximately $37.5 million. Given the growth in deferred revenue expected from its Connected services, I expect FCF to be solid due to working capital benefits. After accounting for expected annual capex, FCF should be around $30 million without any restructuring costs included.

At today’s share price of $3 and considering the company’s net debt position of $170 million, it has an enterprise value of $300 million with 42 million shares outstanding. Based on my estimates, shares therefore currently trade at EV to adjusted EBITDA and EV to FCF multiples of 8 and 10 respectively. I believe the current valuation offers a balance risk-reward considering the attractive outlook for this market leader that will benefit from the increased adoption of AI, yet with increased risks and uncertainties in the near term.

Risks

Future profitability and debt concerns

While the business is anticipated to maintain free cash flow neutrality in FY24 despite the ongoing challenges, the future margin profile and free cash flow generation are uncertain. This risk is compounded by the upcoming 2025 convertible debt of $90 million due next year.

Competition

The company faces competition from the likes of Google (GOOG) and Amazon (AMZN) in the US and Baidu (BIDU) in China. Despite being much smaller than its rivals, Cerence has been able to maintain its market share due to its competitive advantages. Though the company has previously lost a few of its OEM customers to these rivals, it has recently even won some of them back.

Macroeconomic headwinds

The company’s revenue is heavily dependent on new vehicle sales, which can be sensitive to macroeconomic changes. This was cited as a key reason that led to the company withdrawing its earlier guidance. Further worsening of the macroeconomic environment could impact the company’s path to profitability.

Conclusion

The company’s product offerings are poised to benefit from the growing adoption of AI in the automotive industry. However, the near-term outlook carries significant uncertainties and risks for investors. Despite valuation seeming to be attractive at the current price, I chose to remain on the sidelines until I see clear signs of progress being made with regard to the rightsizing of the business.

Read the full article here