Introduction

The US-based broadband and cable operator Charter Communications (NASDAQ:CHTR) which operates the Spectrum brand, has recently been in the news due to its ongoing carriage tussle with The Walt Disney Company (DIS). In this article, we’ll explore the ramifications of this development, after which we’ll seek to ascertain if it would be a good time to buy the CHTR stock.

Charter vs. Disney – The Implications

At the start of this month, Charter Communications put out a notice providing further clarity on why Disney had prevented access to video channels for Charter’s video customers since the end of last month. The former also highlighted their endeavors to get Walt Disney to consider a more value-conscious short-term contract, which was shot down by the latter, who, in turn, prefers pricier long-term deals, with limited packaging flexibility.

CHTR believes that programmers such as DIS are shooting themselves in the feet by following a myopic strategy of being selective in putting out their best content on DTC (Direct to Consumer) platforms, which in turn erodes the competitive positioning of content available on the traditional cable networks, leading to the attrition of subscribers. To ameliorate the ongoing loss of subscribers, programmers, particularly in the high-cost sports avenue, lift affiliate fees, which in turn are passed on, even to non-sports viewers, who feel cheated for having to pay top dollar for content they are not even remotely interested in, which eventually leads to even further customer dissatisfaction and loss. Basically, this is not a very healthy ecosystem to be involved in, and CHTR made certain proposals to DIS that could help dampen the slowdown of its traditional video business and improve package flexibility for its customers.

Disney’s unwillingness to consider CHTR’s proposed hybrid model is certainly not ideal, but what investors should also bear in mind, is that, in the grand scheme of things, the market is unlikely to be too perturbed by the developments linked to this carriage tussle. In fact, after an initial -10% drop in the CHTR stock price, there has already been some recovery around lower levels, with the overall price drop currently standing at just -4% since the announcement on the 1st of Sep.

Rather, we’d like to think that investor focus will continue to be primarily centered around CHTR’s successful execution of its network evolution plan (which involves spectrum expansion to 1.8Ghz and the transition to DOCIS 4.0 technology, amongst others), particularly as delays here could have a more unsavory impact on the overall free cash flow profile of the firm. In contrast, management believes that its video portfolio is “ultimately cash flow neutral” with cash flows from videos already on a declining trend, long before this tussle came to light. All in all, we believe that stakeholder interest will continue to be oriented more toward the broadband and wireless portfolios of CHTR’s overall business.

Admittedly, in the short-term, this disagreement with DIS could be inimical to the smooth operations of CHTR’s business, and could necessitate some compensatory expenditure in the form of one-off consumer credits or rebates (estimated at $3.7bn of revenue or 6.7% of group revenue), not to mention the incidence of unwelcome legal events, it’s worth pondering if the latter would be better served by cutting ties.

We say this because currently, only 25% of Charter’s video subscribers regularly engage with Disney content, yet the overall cadence of annual programming costs that the former pays to the latter, are massive, at $2.2bn! So even if CHTR ends up losing billions in revenues, it would also be cutting the chord with what is, innately, a low gross margin business, which is anyway only facilitating unremarkable dollar drop through to the bottom line.

Closing Thoughts – Is The CHTR Stock A Good Buy Now?

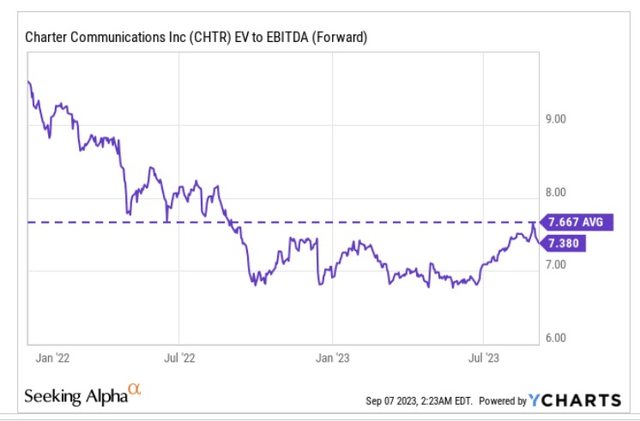

We last covered CHTR in May-23, and back then, the stock could have been picked up at a double-digit discount to its long-term forward EV/EBITDA average multiple. Given CHTR’s positive momentum in the following months, the attractive valuation differential is no longer quite in play. As things stand, CHTR is priced at 7.38x on a forward EV/EBITDA basis, hardly a breath away from its long-term average of 7.66x.

YCharts

Then, those who read our previous article on CHTR would also likely be aware that whilst we expressed some misgivings over the underlying fundamentals of this business, we also did think there were some pretty promising charting developments, that could have been exploited. Nearly four months on, and with a ~23% upside in the share price, it’s fair to say that the reward-to-risk equation is less tantalizing now.

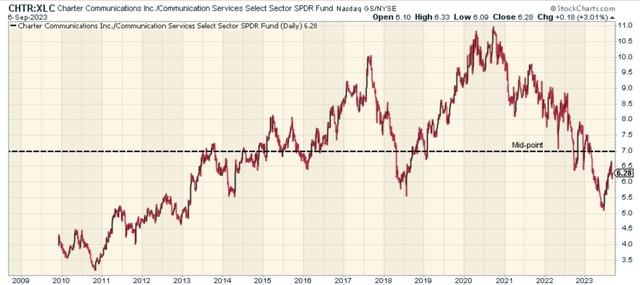

The chart below highlights how Charter Communications is positioned relative to its major communication service peers from the S&P500. CHTR is unlikely to attract too much of rotational interest as its current relative strength ratio is almost on par with its long-term average (this was not the case back in May)

Stockcharts

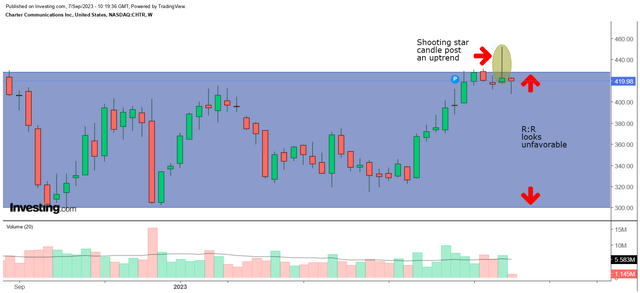

Then, if we switch over to CHTR’s weekly price imprints over the past year, we can see that it has chopped around within an approximate range of $300-$415/420; as things stand, the price is now closer to the upper boundary of this range, which dampens the allure of a long position (you ideally want to be getting in when the price is trading somewhere towards the lower half of its range). What compounds the issue is that last week, one also witnessed the dreaded shooting star reversal candlestick pattern which typically reflects a fatigue in buying pressure.

Investing

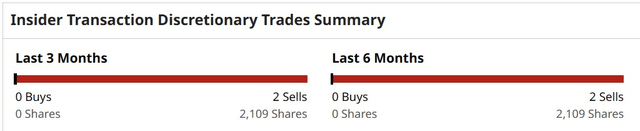

Some caution may also be felt by the fact that a few insiders started selling the CHTR stock last month, after months of dormant insider activity.

Barcharts

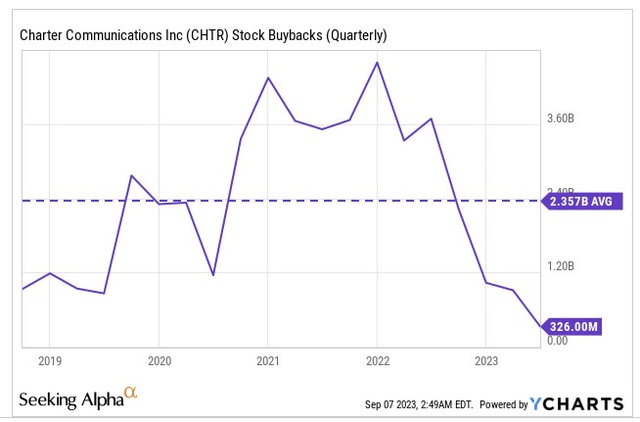

The share price is also unlikely to receive too much of support from buyback initiatives. As the chart below shows, this was a business that was previously deploying over $2.36bn in buyback spend per quarter, but as things stand it is at 5-year lows of just $0.3bn.

YCharts

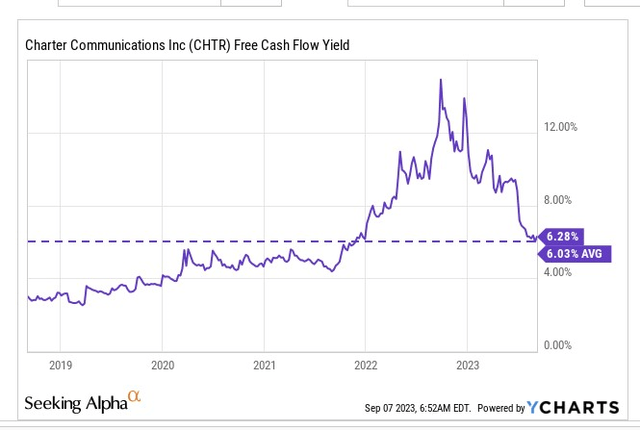

Subdued buyback initiatives are primarily driven by the fact that the company’s free cash flow dynamics have come off in a big way (down by 60% YoY in Q2-23), driven largely by higher CAPEX and higher cash taxes as the company has become a full federal cash taxpayer this year. Note that if you stage an entry in the stock at this stage, there won’t be any great edge, as the current FCF yield is on par with the long-term average. It’s difficult to envisage a drastic improvement in FCF dynamics as CAPEX intensity will likely stay elevated at least till the end of FY25.

All things considered, we don’t believe the CHTR stock would make a good BUY at this stage.

YCharts

Read the full article here