One of the most interesting exploration and production companies in the energy space has got to be Chesapeake Energy Corporation (NASDAQ:CHK). As a business that produces essentially nothing now but natural gas, the enterprise is a way for investors to focus entirely on that commodity. What’s more, management has been working on transforming the firm with the hopes of creating additional shareholder value. To be perfectly truthful with you, the work done by management has not always been successful. I say this because, in June 2020, the company filed for bankruptcy protection. It ultimately emerged from bankruptcy in February 2021.

For my part, I saw problems regarding the business well in advance. I originally proclaimed, in August 2019, that the business was in trouble. The article that I made that claim in saw me rate the firm a “sell.” I ultimately downgraded it further to a ‘strong sell’ in November of that year, even making the claim that ‘the end is fast approaching.’ Even though I have been bullish about many companies in the oil and gas space recently, this was one business that, because of leverage, production declines, and massive capital expenditure requirements, I was wary of.

Unlike many investors who refuse to give a company that has exited bankruptcy a second chance, I am much more open-minded on that front. In January of this year, for instance, I talked about Chesapeake Energy’s decision to merge with Southwestern Energy (SWN) in a deal that amounted to a big bet on what could be potentially big savings. That deal has yet to close. However, I felt it appropriate, at this time, to look at Chesapeake Energy once again from a standalone perspective. What I found was that, while the company is certainly not at risk of bankruptcy like it was previously, it’s far from being a strong prospect for those looking for attractive upside. Because of this, I do still think that the ‘hold’ rating I assigned it earlier this year makes the most sense.

Nothing special

As I dive into this analysis, I would like to reiterate that the purpose of this article is not to talk more about the pending merger that the business has with Southwestern Energy. I did that in detail in my article about the transaction earlier this year. Rather, my goal is to simply understand how healthy, or unhealthy, Chesapeake Energy is on its own. This is in part to inform investors of whether Chesapeake Energy makes sense to buy into, and to understand what the picture will look like should the deal ultimately fail to close. I don’t know the probability of the transaction falling apart. But I do know that regulators are currently looking at it. Given the larger transactions that have gone on in the energy market over the past year or so, I think that a failure for this transaction to close is very unlikely.

Operationally speaking, Chesapeake Energy is a company that is focused on two major natural gas producing regions. The first of these is the Marcellus Shale, where approximately 56.5% of the company’s output comes from. All combined, the company has 758,000 gross acres and 489,000 net acres in that region. The other major region for the business is the Haynesville, which consists of 454,000 gross acres or 381,000 net acres. To be clear, this is not the only acreage that Chesapeake Energy has control over. In fact, the company has another 1.66 million gross acres or 1.57 million net acres split between other areas. This includes 1.2 million net acres that the company retained when, in 2016, it sold off its Devonian Shale assets. The business used to have some other acreage, including a decent amount of exposure that was oil-centric that was located in the Eagle Ford. But in three separate transactions between January 2023 and August 2023, management sold off those assets for $3.53 billion.

Author – EIA Data

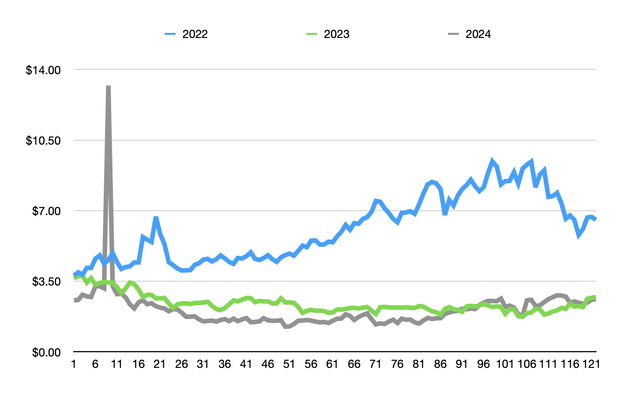

Today, this leaves a company that is basically a pure play in the natural gas space. For those who are bullish on this commodity, this can be a good thing. But in my opinion, this emphasis is not the best idea. The fact of the matter is that natural gas prices have been quite low for quite some time. From the start of this year through June 25th when the most recent data was available, the average price of natural gas has been $2.10 per Mcf. This happens to be $0.30 per Mcf lower than what it was for the same window of time last year. It’s also well below the $6.12 per Mcf that we saw as an average during the same window of time throughout 2022.

Author

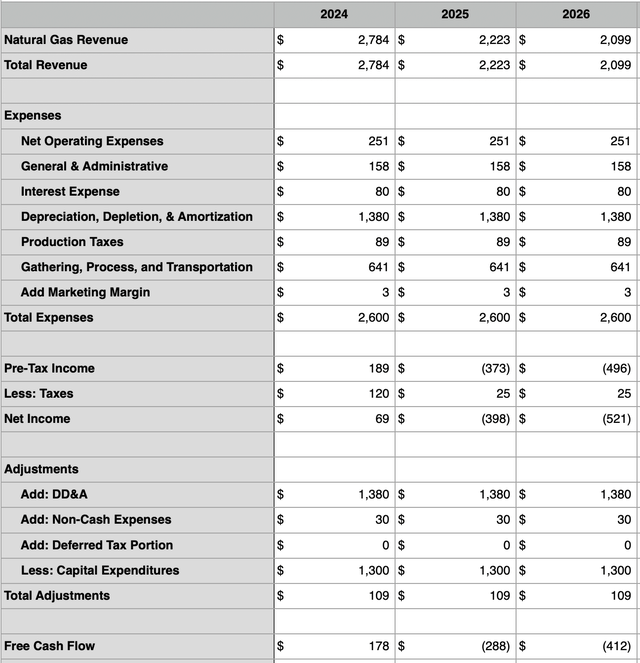

This is not to imply that we are dealing with a company that is likely to collapse. In the table above, you can see a cash flow model that I made for the business for the 2024 through 2026 fiscal years. This model assumes that production remains flat in perpetuity. This year, we are looking at free cash flow of $178 million. Now, to be clear, we do see this turn negative to the tune of $288 million next year before becoming negative to the tune of $412 million the year after. The reason for this decline stems from differences in the company’s hedge book. At some point, management needs to get this to at least being free cash flow neutral. But the hope is that the aforementioned merger will solve some of these problems.

Author

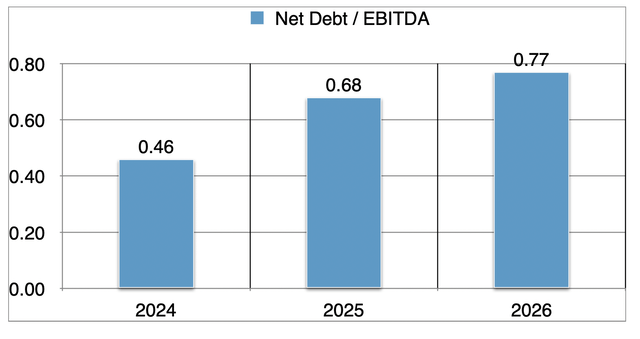

In the next table above, you can see two other profitability metrics set beside free cash flow. These would be operating cash flow and EBITDA. As the table illustrates, the overall trend for both of these should be negative as well. The good news for shareholders is that, at present, the debt situation for the business is under control. As illustrated by the chart below, for 2024, the net leverage ratio for the business is only 0.46. Even with the expected decline in profits next year and the year after, this is unlikely to get higher than 0.77. Generally speaking, investors in this space consider a net leverage ratio of 2 or lower to be desirable.

Author

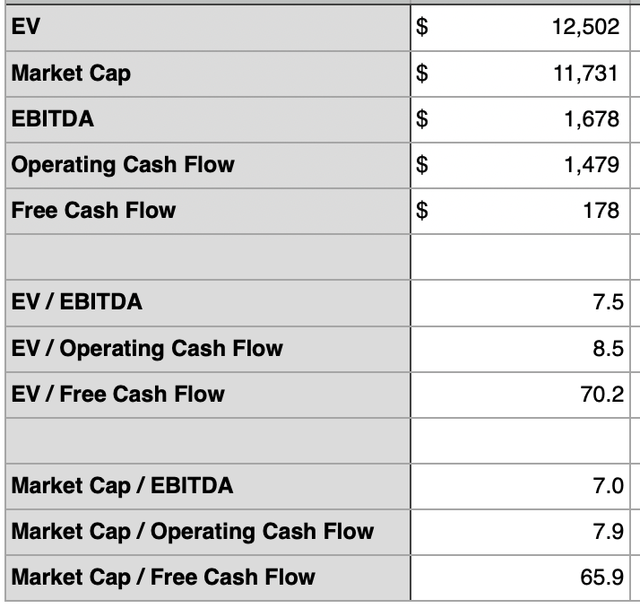

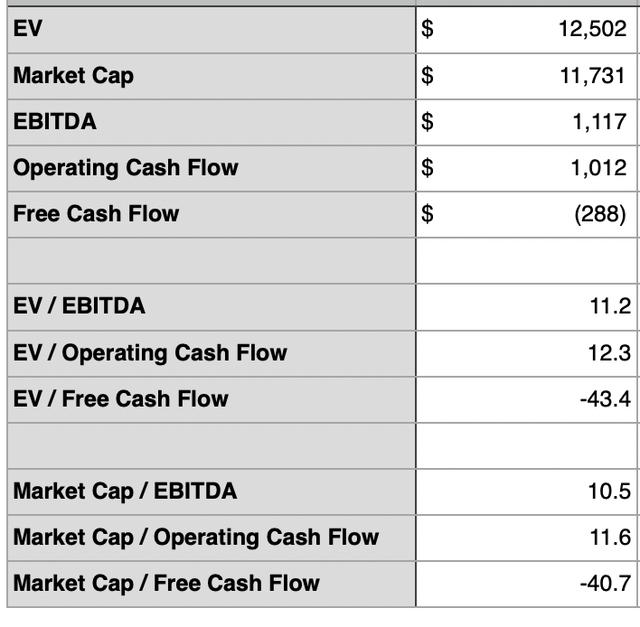

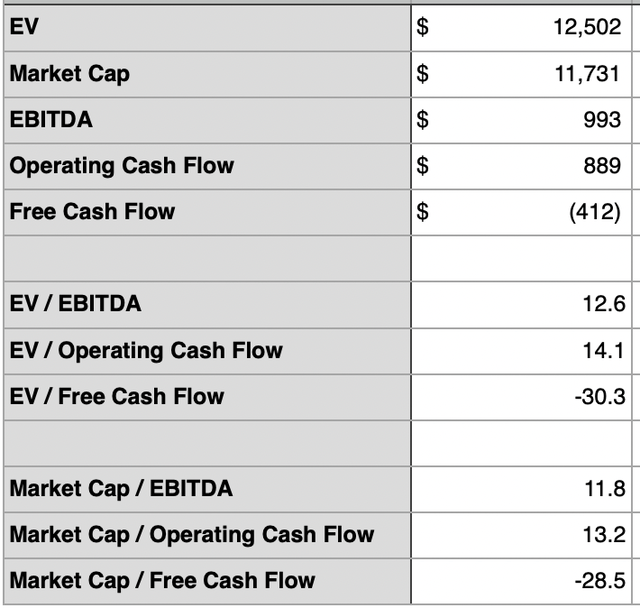

In terms of valuation, it does appear to me as though Chesapeake Energy Is on the lofty side of things. In the first table below, you can see how shares are priced on an EV to EBITDA basis and on a price to operating cash flow basis. This is specifically for the 2024 fiscal year. In the subsequent table, you can see the same analysis repeated for 2025. And in the table below that, you can see the same thing again for 2026. Naturally, the decline in cash flows does make the stock more expensive. Many of the oil and gas exploration and production companies that I have looked at recently are trading at EV to EBITDA multiples of between 4 and 6. So to see something quite a bit higher than this is disconcerting.

Author Author Author

There is some hope that the company might be able to make some profit and cash flow from its LNG deals. This includes an agreement that the firm entered into in February of this year for 0.5 million tons of LNG per annum that it will buy from another firm and then sell to a different party. The netback projected from these activities could be between $4 and $6 per MMbtu, but the contracted start date for that is far out into 2028. The company is also working with another business to produce a new pipeline with an initial capacity of 1.7 Bcf per day that is part of a natural gas gathering pipeline and carbon capture and sequestration project. But with the pipeline not expected to be in service until at least next year, it remains to be seen whether this will be a fruitful enough endeavor to justify the premium that shares are trading for.

Author

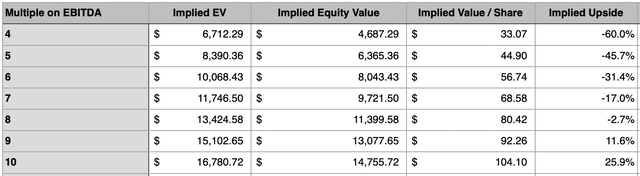

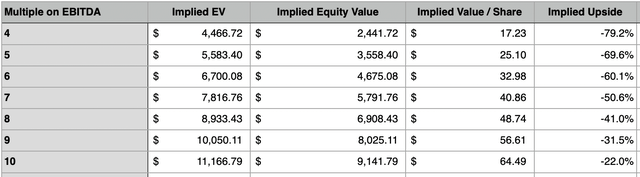

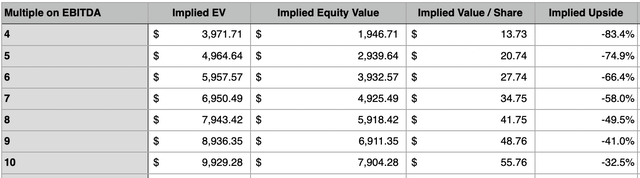

As things stand at this time, the upside for the company looks limited at best. It might, in fact, be nonexistent. In the table above, you can see a hypothetical range for the EV to EBITDA multiple, starting at 4 and ending at 10. In this table, you can see the implied share price of the company and the implied upside that shareholders would experience if the firm were to trade at that multiple. It really would take the business trading near the higher end of the scale to warrant any upside. In the next two tables below, you can see the same type of analysis, with the first of these focused on 2025 and the second focused on 2026. In these cases, the picture looks even worse given the reduction in cash flow that’s anticipated.

Author Author

Takeaway

As much as I would love to say that Chesapeake Energy makes for a compelling opportunity, I honestly don’t believe that is the case. Even though leverage is under control and there appears to be no real risk of bankruptcy and the foreseeable future, Chesapeake Energy Corporation’s cash flow picture is problematic. As a standalone enterprise, this is the kind of firm that I would seriously consider rating a “sell.” But the only thing stopping me from doing that is the potential associated with the aforementioned merger.

Read the full article here