Energy company Chevron (NYSE:CVX) presents a big investment opportunity for investors after the company recently missed earnings estimates for the second-quarter. Chevron reported mixed Q2’24 earnings and experienced a headwind related to a delayed arbitration meeting regarding its planned merger with Hess. However, Chevron is projecting strong production and free cash flow growth in the short term and the company has done an excellent job in returning more cash to shareholders in the last couple of years. Further, Chevron has outperformed its U.S. rivals in terms of dividend growth which makes CVX an especially attractive investment for income investors. In my opinion, investors should consider buying the drop as the risk profile remains skewed to the upside and the energy company is set to grow its dividend going forward.

Previous rating

I rated Chevron a strong buy in April as the energy company benefited from high petroleum prices in the $80s price range and OPEC+ announced that it would cut back on production in order to support petroleum prices. I believe Chevron remains a very attractive investment, especially from a capital return point of view, and I see a growing dividend as well as growing production volumes as good reasons to invest.

Growing production volumes and free cash flows

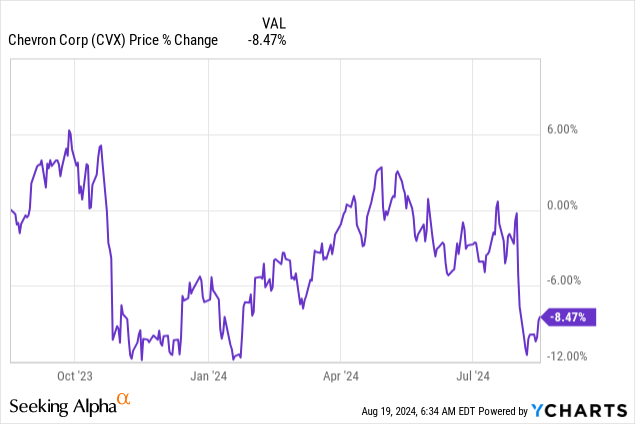

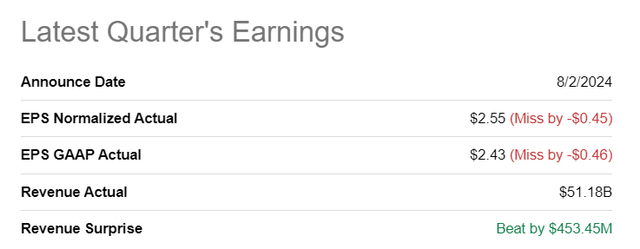

Chevron’s shares went into free-fall after the company’s mixed second-quarter earnings scorecard that showed a sizable earnings miss, but also a top line beat. Chevron earned $2.55 per-share in Q2’24, $0.45 per-share less than expected, while the company beat the consensus top line expectation by nearly half a billion dollars.

Seeking Alpha

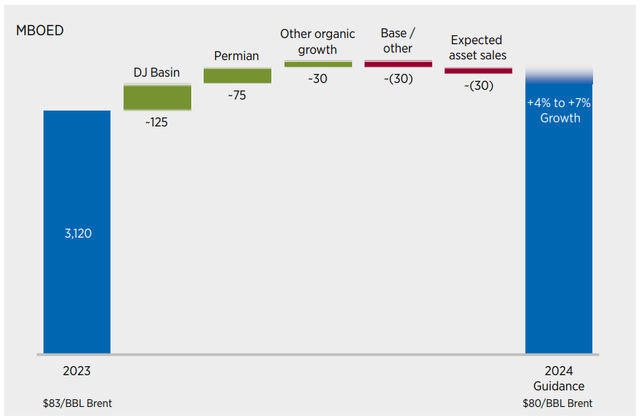

Chevron is seeing strong growth in its production, however. Chevron’s upstream liquids production surged 24% year-over-year to 1,132 MBD in the second-quarter and this growth comes chiefly from the company’s PDC Energy’s assets, which Chevron acquired last year for $7.6B. Chevron has also guided for its Permian assets to generate approximately 10% year-over-year production growth which is set to contribute to the company’s overall estimated production growth rate of 4-7%.

Chevron

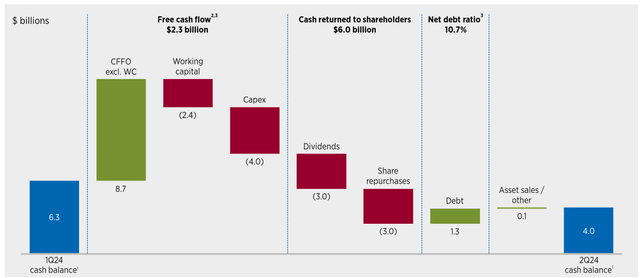

The company is benefiting from high average petroleum prices and Chevron therefore has a ton of potential to grow its capital returns. In the second-quarter, Chevron generated $2.3B in free cash flow (after working capital and long term capital needs were met), and the energy company returned a total of $6.0B to shareholders… with capital returns about evenly split between dividends and stock buybacks. In the previous quarter, Chevron’s operations generated $2.7B in free cash flow. As a result, Chevron returned all of its free cash flow to investors in the second-quarter.

Chevron

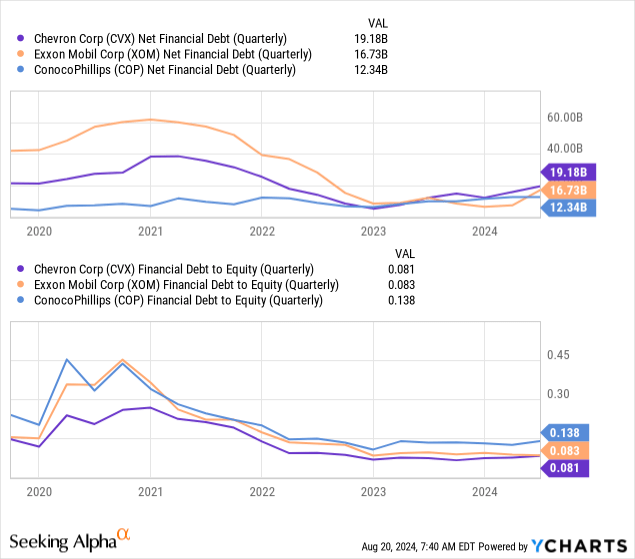

Chevron has the cash on its balance sheet to ensure the payment of continual dividends and stock buybacks. It also has a lot of net financial debt ($19.2B as of the end of the June quarter), as do most energy companies, but the leverage ratio is actually the lowest in its industry group at 8.1%.

Chevron’s valuation

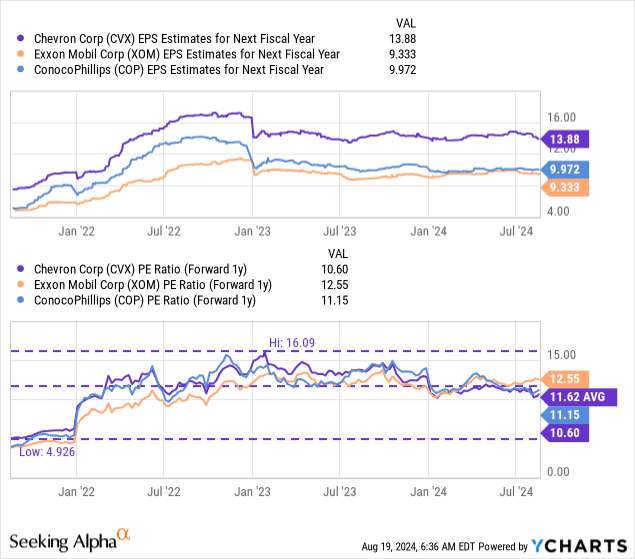

Chevron is currently valued at a price-to-earnings ratio of 10.6X which compares against a longer term, 3-year P/E ratio of 11.6X (implying a discount of ~9%). Chevron is also trading at a cheaper valuation factor than ExxonMobil (XOM) whose earnings potential costs investors about 12.6X FY 2025 earnings. ExxonMobil is also projecting strong growth related to its Permian assets and has submitted a strong capital return outlook as well. ConocoPhillips (COP), which is much less diversified given its sole upstream focus, is trading at 11.2X forward earnings, but I see more risks here given that the company’s earnings should prove to be much more volatile in a down-market.

Chevron’s shares sold off at the beginning of the month after it was reported that an arbitration hearing in the Chevron-Hess merger was delayed, creating negative sentiment for the energy company and its investors. ExxonMobil and CNOOC have made competing claims relating to some of Hess’ Guyana assets which has led to a delay in the merger between the two companies. Chevron now expects the arbitration hearing to take place in May 2025, as opposed to Q4’24.

Given that Chevron is growing its production and generating strong free cash flow, I believe this negative sentiment is undeserved. Shares have also become significantly cheaper on the drop, creating an engagement opportunity for investors. Like ExxonMobil, I believe Chevron could trade at 13-14X FY 2025 earnings which implies a fair value range of $181 to $195 (based off of a FY 2025 consensus estimate of $13.89 per-share).

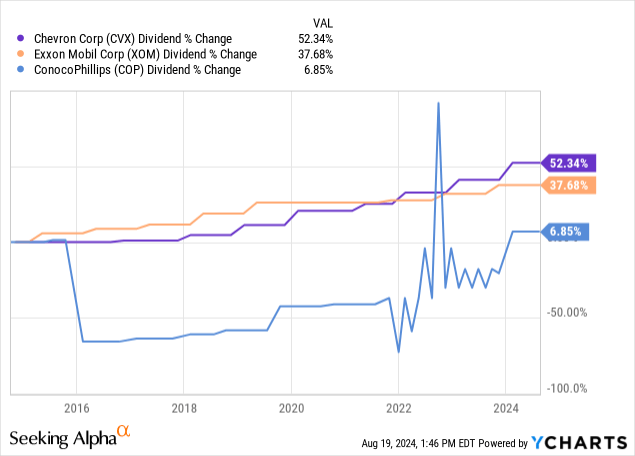

Given that petroleum prices still are quite high, I believe earnings and free cash flow prospects are still very much attractive for investors that seek a high-quality income play in the energy sector. This is especially true for Chevron which has out-performed ExxonMobil and ConocoPhillips in the last ten years in terms of dividend growth. Based off of a current quarterly dividend payout of $1.63 per-share, COP currently enriches income investors to the tune of 4.5% annually.

Risks with Chevron

The biggest commercial risk for Chevron, as I see it, is a potential down-turn in the economy which would most likely lead to a contraction in petroleum prices and lower free cash flow and capital return potential for cyclically-positioned energy companies. What would also change my mind about Chevron is if the Permian-based growth strategy were to falter or if the company were to see declines in its net production volume.

Chevron just settled with the City of Richmond for $550M in exchange for the city withdrawing a refinery oil tax proposal. The $550M will be paid over a 10-year period which means the settlement is not financially significant for Chevron. While there is a risk to similar settlements in the refinery business, I don’t believe the $550M payment fundamentally impacts the investment case for Chevron.

Final thoughts

Chevron reported second quarter results that were really not that bad, but the market has been on a weak footing and the delayed arbitration hearing has weighed on investor sentiment as well. The market has garnered new strength lately and Chevron’s shares appear to be in the early stages of a rebound. This creates a favorable backdrop for investors that are cashed up and are looking to buy a stable, growing energy firm that is set to grow its capital returns and free cash flows going forward. With shares of Chevron trading at only 10.6X FY 2025 earnings, implying an earnings yield of more than 9%, I believe the risk profile here is widely skewed to the upside. Further, Chevron has outperformed ExxonMobil in the last ten years in terms of dividend growth which makes CVX the preferred energy investment from a dividend growth perspective as well!

Read the full article here