Introduction

I like commercial REITs that have a very strong relationship with their tenants. Choice Properties (TSX:CHP.UN:CA) (OTC:PPRQF) has Loblaws as its main tenant and has a historic relationship with the superstore chain. Choice Properties was spun out of Loblaws and still has the same majority shareholder. I doubt Loblaws will stop leasing assets from a related party and I consider the strong ties to be a clear positive for Choice Properties. This article is meant as an update to previous articles. You can read the older articles on Choice Properties here.

The AFFO continues to increase

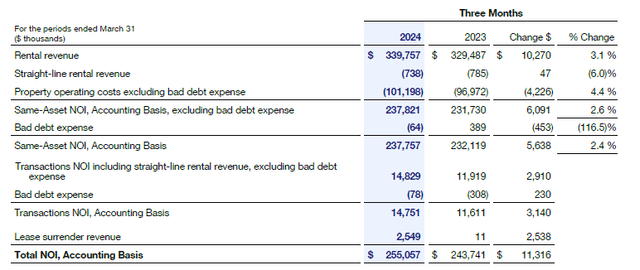

When looking at a REIT, I’m mainly interested in its FFO and AFFO performance, as those metrics provide a better look under the hood than for instance a net profit result. Another important element and starting point is the net operating income, and as you can see below, Choice Properties saw its same-asset NOI increase by approximately 2.6% compared to the first quarter of 2023, while the addition of new assets further boosted the NOI to C$255M, an increase of almost 5% compared to the C$244M in Q1 2023.

Choice Properties Investor Relations

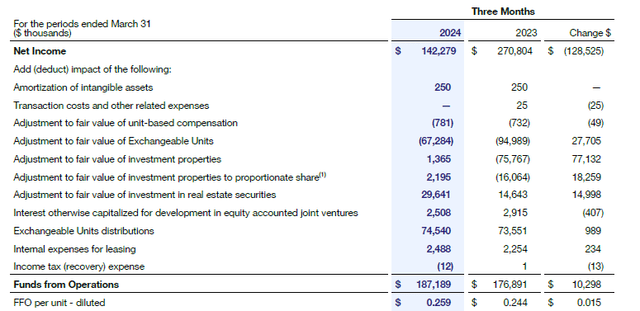

As Choice Properties has a good grip on its financing situation (I will discuss that later in this article), I was keen on seeing if the NOI increase also translated into a FFO and AFFO increase. Fortunately that was indeed the case and as you can see below, the total FFO increased by approximately C$10.3M to C$187.2M. This means the FFO per share was approximately C$0.259, and as you can see on the image, despite a small dividend increase, the payout ratio actually decreased to the low-70% range.

Choice Properties Investor Relations

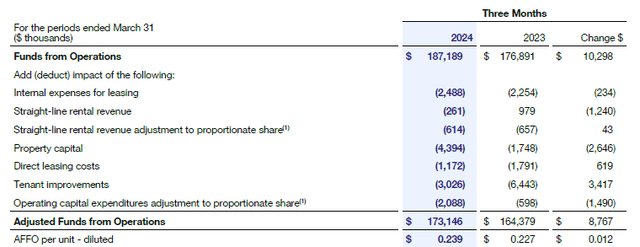

While the FFO is important, I give more weight to the AFFO calculation as it includes certain capital expenditures including tenant improvements. The image below shows the breakdown, and although the REIT spent about C$7.4M on capex and tenant improvements (which is roughly in line with its spending in Q1 2023), the AFFO still showed a nice C$8.8M increase to C$173.1M. Divided over the almost 724 million shares outstanding, the AFFO per share was C$0.239.

Choice Properties Investor Relations

As the REIT is currently paying a dividend of C$0.76 per year, payable in twelve equal monthly tranches of C$0.0633, the distribution is well covered as the payout ratio has dropped to less than 80%.

Should I be worried about the balance sheet?

As REITs had to deal with the increasing interest rates on the financial markets, I’m obviously very interested in seeing what the potential impact could be going forward. I think the worst is behind us, and although the REIT obviously will still have to deal with increasing interest rates, I think the impact could be relatively moderate.

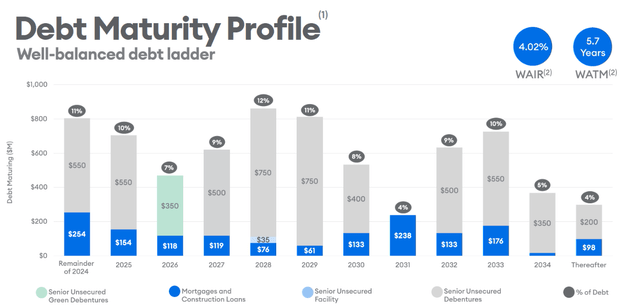

As you can see below, Choice Properties’ maturity profile is nicely spread out in time which means the higher cost of debt will be very palatable.

Choice Properties Investor Relations

Choice Properties recently issued a seven-year bond with a 5.03% coupon. This means we can reasonably expect the average cost of debt to increase toward that 5% level (although decreasing benchmark interest rates may make future refinancings cheaper than that). With just under C$6.5B in debt on the balance sheet, this means the maximum impact of seeing an increase of the cost of debt to 5% would be around C$65M or C$0.09 per share.

As mentioned above, this won’t happen overnight and will be a multi-year process. Meanwhile, Choice Properties should be able to hike its rents at a low single digit percentage per year. And considering the annualized NOI is approximately C$1B per year, increasing the NOI by 1% per year over the next six years would take care of the entire impact of higher interest rates on its debt.

And the retained cash flow (thanks to the sub-80% payout ratio this year) will help to fund the development portfolio. The REIT is currently actively developing C$62M of retail assets with an anticipated stabilized yield of approximately 6.5% and C$348M in industrial assets with an anticipated stabilized yield of 7.25%. This could boost the FFO by approximately C$29M. Approximately C$290M of the C$348M capex still has to be spent.

Investment thesis

Choice Properties REIT is not cheap based on its current earnings multiple. As we can expect a full-year AFFO of C$0.93-0.94 per share (increasing to C$0.95-0.96 next year), Choice is currently trading at a multiple of around 13 times its AFFO. That’s not cheap, but I also think a certain premium is warranted given the strong ties with main tenant Loblaws which reduces the leasing risk. I doubt Loblaws will stop leasing assets from a related party, and so far I haven’t seen any clear corporate governance issues (like CHP giving Loblaws a good deal on its rent). So I currently consider the strong ties with Loblaws and the family behind Loblaws to be a positive.

Meanwhile, after the recent share price decrease, the dividend yield has increased to 6%. And considering the AFFO performance remains robust, I wouldn’t be surprised to see more dividend hikes in the future, although Choice has been conservative and hiked its distribution by just C$0.01 per share per year.

I have a long position in Choice Properties, and I’m adding to that position at the current share price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here