Back in April, I wrote that Chord Energy (NASDAQ:CHRD) was one of the cheapest stocks in the oil patch, and that the company has been under-earning due to a poor hedge book that will roll off in 2024. The stock has generated a nearly 17% return since then, compared to a nearly 8% gain for the S&P 500. With the company having reported Q2 results earlier this month, let’s catch up on the name.

Company Profile

As a refresher, CHRD is an energy exploration and production company that was formed through the merger of Whiting Petroleum and Oasis Petroleum just over a year ago. The E&P’s primary focus is on the Williston Basin (Bakken), where it holds the largest acreage position in the basin. Virtually all of its acreage is held by production.

At the end of 2022, it had net proved reserved of 655.6 MMBoe, of which 77% were classified as proved developed. Approximately 58% of its reserves are oil, while 21% are NGLs and the rest natural gas.

Following recent deals, it had 1,028K net acres, on which it had a 74% working interest.

Wheeling and Dealing

Following my initial write-up, CHRD acquired more Williston acreage, spending $375 million to acquire ~62,000 net acres from XTO, a subsidiary of Exxon Mobil (XOM) in late May. The acreage was ~77% undeveloped.

The assets currently had production of around 6 MBoe/d, of which ~62% was oil. The base decline rate was about 23%.

CHRD then turned around and sold acreage that included 153 producing wells across 16 fields in the Permian to BCO Resources. The acreage had 1.3 MMBOE of net PDP reserves, of which 84% was liquids. Terms of the deal were not disclosed, but on its Q2 earnings call, the company said it sold $29 million in non-core assets and $64 million year to date.

The company said the acquisition will add 3,000 barrels of oil per day in the second half, while non-core sales were approximately 500 barrels of oil per day.

On its Q2 earnings call, CEO Daniel Brown said:

“This bolt-on was an excellent supplement to our core inventory and demonstrates natural synergies from our scale position in the Bakken, which is now over 1 million acres. We added approximately 123 net locations. And importantly, we were also able to convert 6 core 2-mile DSUs [drilling space unit] into 3-mile DSUs. This further enhance the economics of the deal, which is immediately accretive to cash flow, free cash flow and our return metrics. In light of the above, we have updated our full year capital forecast to a range of $850 million to $880 million. Excluding the $11 million of reimbursed nonoperating capital, the midpoint of annual CapEx investment increased approximately $20 million, largely due to additional drilling and completions activity associated with maintaining a larger production base moving forward.”

With CHRD virtually a Bakken pure play, adding acreage to its core holdings while disposing of some non-core assets is a smart move. As the largest producer in the Bakken, the company should see synergistic benefits from additional acreage ground to its core holdings, which it is predicting it will see.

Q2 Results

For Q2, CHRD recorded revenue of $912.1 million, up 15.5% from a year ago. Oil, NGL, and gas revenue climbed 29% to $695.4 million. Crude oil revenue rose 54.7% to $647.9 million, while natural gas revenues fell from $119.7 million to $19.0 million. NGL revenues were $28.5 million versus none a year ago. Notably, all year-ago numbers only reflect legacy Oasis results, and not a combined Whiting-Oasis.

Adjusted EBITDA came in at $369.9 million, up 44.4% from $244.9 million. Adjusted EPS was $3.65 versus $7.30 a year ago.

The company saw $51 million in hedge losses in Q2, which was an improvement from the $92 million it experienced in Q1.

Total production rose 164% to 169.0 MBoe/d from 64.1 MBoe/d a year ago. That was ahead of the 163.2-168.2 MBoe/d forecast the company had given earlier. Oil volumes rose 124% to 96.4 MBo/d, compared to guidance of 93.5-96.6 MBo/d.

NGL volumes came in above expectations at 36.0 MBl/d, versus a forecast of 33.5-34.5 Mbl/d, but price realizations as a percentage of WTI were only 12% versus expectations for 23-33%. Natural gas volume was 219.3 MMcf/p versus expectations of 217-223 MMcf/d, although prices remained low.

CHRD ended the quarter with $395 million in long-term debt and $214.8 million in cash on its balance sheet. As a result, leverage is de minimus at 0.1x. It is looking to pay out a base dividend of $5.00 a share, and return 75%+ of FCF to shareholders if leverage is below 0.5x.

Overall, it was a solid quarter from CHRD, with volumes generally coming in ahead of its forecasts, as well performance was strong. The company obviously can’t control energy prices, and low NGL and nat gas prices did weigh on results some. However, its balance sheet remains strong and the company looks well positioned moving forward.

Outlook

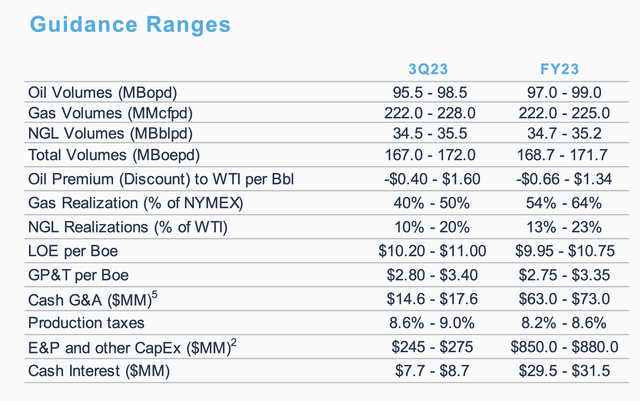

Looking forward, CHRD guided for Q3 total volumes of between 167-172 MBoe/d, with oil volumes of between 95.5-98.5 MBO/d. NGL volumes are projected to be 34.5-35.5 Mbl/d, with a net realization of WTI of 10-20%. Nat gas volumes are forecast to be 222.0-228.0 MMcf/d.

For the full year, CHRD forecast total volumes of between 168.7-171.7 MBoe/d verus prior guidance of 164.0-168.5 MBoe/d. Oil volumes are now expected to be between 95.5-98.5 MBO/d compared to a prior forecast of 95.0-98.0 MBO/d. NGL volumes are projected to be 34.7-35.2 Mbl/d, with a net realization of WTI of 13-23%. That compares to prior guidance of 33.0-34.0 Mbl/d, with a net realization of WTI of 23-33%. Nat gas volumes are forecast to be 222.0-225.0 MMcf/d versus 216.0-220.5 MMcf/d previously.

Company Presentation

Discussing its development of its earnings call, Brown said:

“As most of those on the call know, 3-mile laterals are an important part of our program in 2023 and beyond. … We have materially reduced drilling times for 3-mile wells over the past year and are now running a little ahead of schedule. On the cleanout side, we’ve also made steady improvements and have generally been able to stimulate and access the vast majority of the third model. As a reminder, for 3-mile wells, we are assuming a 40% EUR uplift for 50% longer lateral and about 20% more drilling and completion costs. Said another way, we’re assuming the third mile is only 80% as productive as the first 2 miles. In practice, what we’re seeing is a volume response proportional to the percentage of the third mile that’s cleaned out. So a 50% longer well that was cleaned out all the way to the toe is generally delivering an approximate 50% uplift in EUR. In some instances, we’ve been unable to clean out a small portion of the toe and that can lead to a reduction in productivity for the last mile. But once again, we’ve anticipated this with our 80% production assumption I just discussed. … The 3-mile wells are clearly outperforming 2-mile wells in the same area. … Given the large number of potential 3-mile laterals CHRD has and the improved capital efficiency opportunity, these laterals represent, the results we are seeing are exciting and [show] that our execution performance has been improving.”

The company expects to generate $1.7 billion in EBITDA in 2023 and $735 million in FCF. If hit, it would look to return around $13 per share back to shareholders through dividends and buybacks.

CHRD’s wells are performing better than expected, which, in combination with its recent bolt-on acquisition, bodes well for further production gains going forward. If energy prices co-operate, the company is in good shape for 2024, especially as unfavorable oil hedges roll-off.

Valuation

CHRD trades at 4.0x EBITDA based on 2023 analyst estimates of $1.67 billion. Based on the 2024 consensus of $2.1 billion, the stock trades at a 3.2x multiple. Of course, the price of oil, NGLs, and natural gas can change the actual results immensely.

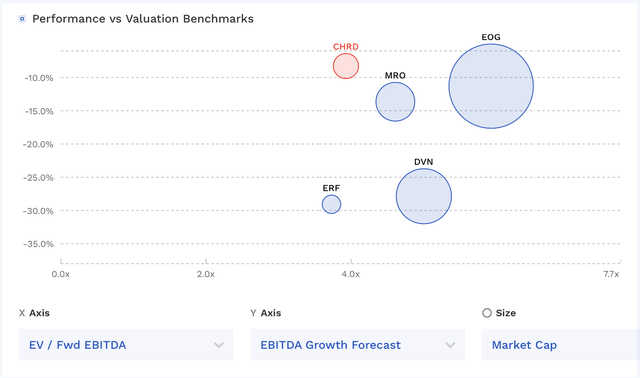

CHRD is valued in the low-end of the pack compared to other independent E&Ps, despite it being nearly debt free and under-earning because of its hedge book. Being tied solely to the Bakken could play a role, as Bakken E&P Enerplus (ERF) also trades at a discount.

CHRD Valuation Vs Peers (FinBox)

Conclusion

While not as inexpensive as when I first looked at it, CHRD remains a bargain in the oil space in my view. While the Bakken doesn’t get the love of the Permian, the core acreage there has very attractive return profiles, and with the largest position in the basin, CHRD is able to take advantage of its scale there.

I like its recent moves to make its position even stronger, taking advantage of its strong balance sheet to add core acreage. With the financially stronger Energy Transfer (ET) taking over Crestwood (CEQP), it will be interesting to see if this will ultimately benefit CHRD, which was CEQP’s biggest customer in the Bakken.

Overall, I still remain productive on oil, as OPEC+ has become more proactive and U.S. producers are no longer chasing prices and much more disciplined. China hasn’t been as strong as expected, but there is still some more time for this to play out. Meanwhile, the U.S. economy has been more resilient than I expected earlier this year.

With solid assets, a strong balance sheet, inexpensive valuation, and unfavorable hedges continuing to roll off, I continue to rate CHRD a “Buy.”

Read the full article here