Chubb Limited (NYSE:CB) provides insurance services to businesses and individuals, highly present in property & casualty insurance. I believe the stock is priced quite modestly compared to the company’s very defensive earnings nature, constituting a buy-rating.

The Company

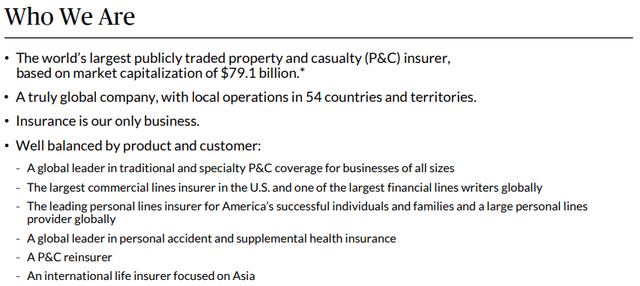

Chubb condenses the business well in the company’s Q2 earnings presentation:

Chubb Q2 Earnings Presentation

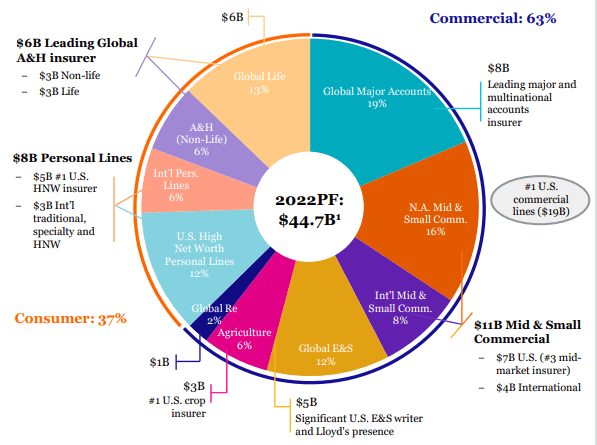

Further, the company is present on multiple segments, as the company provides a diversified offering of insurance products:

Chubb 2022 Investor Presentation

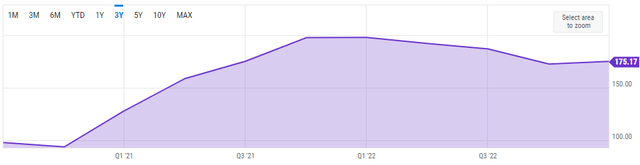

As Chubb is segmentally and geographically diversified company, I believe the company’s risk profile on a single vertical is quite low – geographically, the company operates subsidiaries in 54 countries, and around 58% of the company’s revenues come from the United States. The low risk profile is further demonstrated by a quite stable long-term growth in the stock’s price, as the stock has appreciated at a CAGR of around 10.6%:

Chubb’s 30-year Chart (Seeking Alpha)

On top of the appreciation, Chubb does pay out a small quarterly dividend, with a current estimated annual yield of 1.68%.

Financials

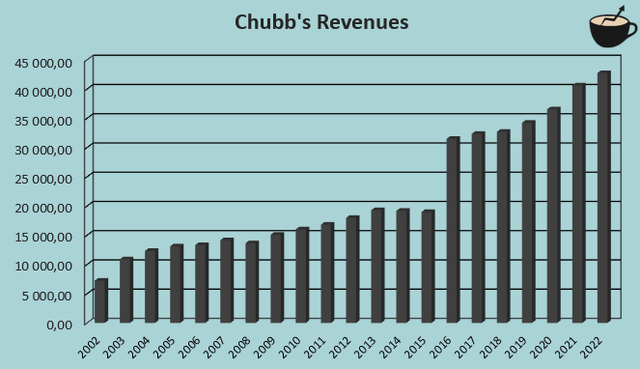

Chubb has had a reasonably good revenue history, as the company’s compounded annual rate has been 9.3% from 2002 to 2022:

Author’s Calculation Using TIKR Data

A good amount of the growth has been organic, but not entirely – for example, the jump from 2015 to 2016 is related to ACE Limited’s acquisition of Chubb for around $29.5 billion in total. Related to the acquisition, the formed company changed its name to the current name of Chubb Limited from ACE Limited.

The growth doesn’t seem to have stopped yet – although the growth is mostly non-organic as in 2022 Chubb acquired Asian insurance businesses for around $5.4 billion, the company’s growth still seemed good at 24.9%. The growth doesn’t seem to be altered by a challenging economy – Chubb’s Q2 earnings call seemed to have a positive tone with CEO Evan Greenberg communicating further momentum into the second half along with a double-digit EPS growth.

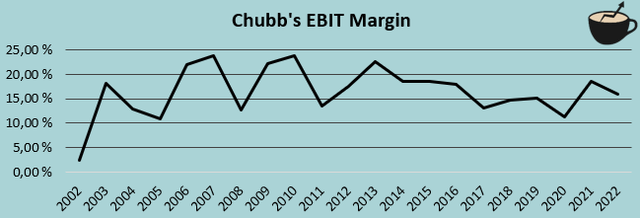

Chubb has kept a good EBIT margin in the company’s history, with an average of 16.5% from 2002 to 2022:

Author’s Calculation Using TIKR Data

The current trailing figure of 16.7% falls in line with the company’s history – Chubb seems to be able to keep a stable margin through accurate pricing.

Chubb leverages some debt in the company’s balance sheet – the company has around $14.5 billion of long-term debt, of which $0.7 billion is to be paid off within a year. Compared to the company’s market capitalization of $84 billion, the amount seems very reasonable when also considering the company’s quite stable cash flows. The company also has a cash balance of around $2.3 billion.

A Current Safehaven

As interest rates keep climbing higher, the economy is at a risky state. With the inflation still at 3.2% in July despite rising interest rates and a GDP showing basically stable figures, the risks of a recession are still high. The insurance industry should be relatively a safehaven if an economic downturn should come; insurance premiums should still come in despite a worse economy. Although the commercial segment representing 63% of revenues should be somewhat riskier than the consumer segment, I think Chubb should be quite safe.

S&P 500’s trailing EPS as of Q1/2023 is around 11.5% below the figure of Q1/2022:

S&P 500 EPS (YCharts)

In the meanwhile, Chubb has already proven a good financial performance in the turbulent economy, as the company continued to improve earnings in Q2 of 2023. I believe that Chubb should be a relatively safe pick for investors, rising attractiveness in the current situation.

Valuation

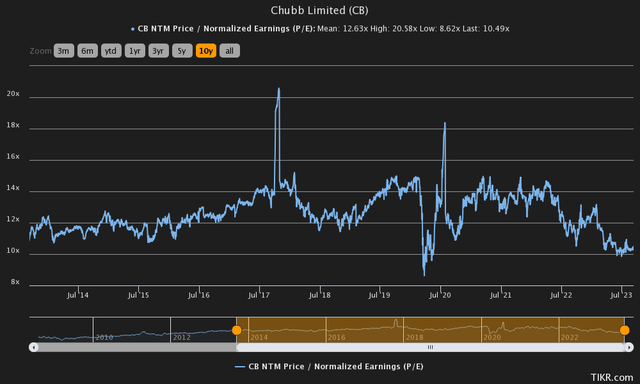

Although the company seems to have a good financial history and a low risk profile, the company seems to be quite cheap compared to the S&P 500’s P/E of around 24.5 – Chubb is currently trading at a forward price-to-earnings ratio of 10.5, below the company’s ten-year average:

Chubb’s Forward P/E History (TIKR)

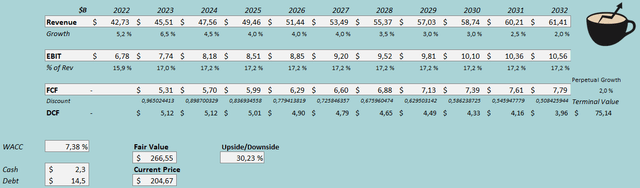

To further analyse the valuation, I constructed a discounted cash flow model of Chubb. In the model, I estimate the insurance provider to have a growth of 6.5% for 2023, signifying slight decreases in the second half – I believe this is quite conservative compared to the CEO’s comments of continued momentum, but I like to stay on the conservative side. Going further, I estimate a growth of 4% for a few years that eventually slows down into a perpetual growth of 2% in steps. The growth estimate is significantly below the company’s historical average of 9.3%, but as the DCF model doesn’t account for acquisitions, I believe the estimates are fair.

As for the EBIT margin, I estimate Chubb to have a quite stable future – I estimate a margin of 17.0% for 2023, with an increase to 17.2% in 2024 that stays as the margin into perpetuity. These estimates along with weighed average cost of capital of 7.38% craft the following DCF model scenario with an estimated fair value of $266.55, around 30% above the current price:

DCF Model (Author’s Calculation)

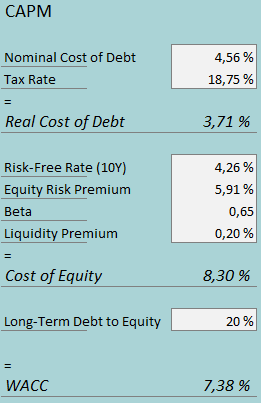

The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q2 of 2023, Chubb had $165 million in interest expenses. With the company’s long-term debt balance of around $14.5 billion, Chubb’s interest rate around 4.56%, used in the model. As the company is incorporated in Switzerland, Chubb seems to pay quite a low tax rate, and guides for a tax rate between 18.5% and 19% for the current year. As Chubb has historically had a reasonable amount of debt, I expect the debt-to-equity ratio to stay quite stable at a ratio of 20%.

For the risk-free rate, I use the United States’ 10-year bond yield of 4.26%. The equity risk premium of 5.91% is Professor Aswath Damodaran’s estimate for the US, made in July. Tikr estimates Chubb’s beta to be 0.65. Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity of 8.30% and a WACC of 7.38%, used in the DCF model.

Takeaway

At the current price, Chubb seems like a safe pick. Although the stock shouldn’t have a very large growth, the current valuation seems to reflect a higher risk profile than I believe the stock has – Chubb has a P/E ratio that’s around 40% lower than the S&P 500 in total, even though Chubb’s systemic risk should be lower than the indexes. For this reason, I have a buy-rating for the stock.

Read the full article here